NSF OIG Audit Update NORTHEAST CONFERENCE ON COLLEGE COST ACCOUNTING

|

|

|

- Avis Underwood

- 6 years ago

- Views:

Transcription

1 NSF OIG Audit Update 1 NORTHEAST CONFERENCE ON COLLEGE COST ACCOUNTING S e p t e m b e r 2 3,

2 Overview 2 Overview of NSF OIG Office of Audit Overview of Federal financial assistance in the U.S. Framework for Grant Oversight Grant Reform Purchase Card Oversight

3 NSF OIG Who We Are 3 Inspector General Office of Audit Counsel to the IG Office of Investigations Financial Statement and IT Audit Compliance Analytics External Audit Performance Audit Administrative Staff Expertise in areas of research, grant, and contract administration Admin. Investigations (Investigative Scientists) Civil/Criminal Investigations (Special Agents) Investigative Legal / Outreach (Investigative Attorneys) Investigations Specialists and Support Staff

4 Office of Audit Promote economy and efficiency in NSF s financial, administrative, and program operations Internal Audits Performance audits of NSF program management Oversee annual audit of NSF s financial statement Information technology and security External Audits Audit NSF-funded grants, contracts, and cooperative agreements Determine whether claimed costs are allowable, reasonable, and allocated properly Outreach 4 OIG Semiannual Report:

5 Work Required by Law: Audit Planning Agency Financial Statement Audit (CFO Act) Federal Information Security Management Act (FISMA) Improper Payment Elimination and Recovery Act (IPERA) Other: OIG Risk-based Assessments Referrals from Investigations NSF Management Challenges National Science Board and NSF Suggestions Congressional Requests 5

6 U.S. Financial Assistance Overview $600 billion in awards 88,000 awardees and 26 Federal grant making agencies Project and research, block, and formula Outcomes are designed to promote public good Challenges Limited visibility of how Federal funds are spent by awardees Support for funding requests much less than for contracts American Recovery and Reinvestment Act (2009) $840 billion of assistance to stimulate the economy ARRA spending still being tested in audit work Greater accountability and transparency over spending than ever 6

7 Grants Differ From Contracts GRANTS Promote services for the Public Good Merit review (competitive) Multiple awardees Award budget No government ownership Grant payments Summary drawdowns No invoices for claims Expenditures not easily visible Salary percentages 7 CONTRACTS Specified deliverables (Goods and Services) Competitive process One awardee Contract Price Government ownership Contract payments Itemized payment requests Invoices to support claims Detailed costs Salary hourly rates

8 Grant Audit Focus Areas Award Administration NSF administration (controls) Awardee administration (controls) Cost Compliance Allowable Within award scope Documented

9 Award Administration Grant Recipient Responsibilities We Look At Financial management system and expenditures Accuracy and timelines of reporting, notifications Participant support, sub-award monitoring Effort reporting Common Findings No approvals, no procedures for determining allowable costs Effort reporting not timely, not approved by correct official Budget not compared to actual expenditures Participant support reallocated without prior NSF approval Inadequate sub-award monitoring

10 Cost Compliance Costs must be allowable, reasonable, allocable, documented, and consistent in treatment We Look At All costs, including cost share expenditures, claimed on NSF awards. We use data analytics tools to identify risk areas. Common Findings Unsupported expenditures Reimbursements not documented (invoices, etc.) Time and effort not timely, not signed/certified Unallowable expenditures Direct charges for costs in the indirect pool Excess faculty/senior personnel salaries (unless NSF-approved) Meals, non-related travel, alcohol Unapproved changes in participant support

11 Framework for Grant Oversight Data analytics-driven, risk-based methodology to improve oversight Identify institutions that may not use Federal funds properly Techniques to surface questionable expenditures Life cycle approach to oversight Mapping of end-to-end process to identify controls 100% review of key financial and program information Focus attention to award and expenditure anomalies Complements traditional oversight approaches Techniques to review process and transactions are similar Transactions of questionable activities are targeted 11

12 Automated Oversight More efficient use of resources 100% transaction review Still use traditional audit techniques to test transactions Opportunities to enhance oversight with less resources Improved risk identification Business rules based on risks Focus review on higher risks Recipients and Agency Officials can use data analytics Monitor grant spending Identify anomalies early

13 Data Analytics Help. Determine reliability data fields Shape of the data (statistics) Completeness of transactions and fields Show anomalies Within a database Between databases Changes in behavior over time Develop risk profiles and scores for comparisons Awardee profiles Award-type profiles Program profiles Transaction level data is key

14 Data Analytics: Myths and Realities 14 MYTHS REALITIES Data only, no fieldwork Numbers exercise Process changes data Findings unsupported Not auditing Focuses fieldwork Still test support with traditional techniques Source data not changed Findings have stronger support Yellow Book Compliant

15 End to End Process for Grant Oversight 615 PRE-AWARD RISKS Funding Over Time Conflict of Interest False Statements False Certifications Duplicate Funding Inflated Budgets Candidate Suspended/Debarred ACTIVE AWARD RISKS Unallowable, Unallocable, Unreasonable Costs Inadequate Documentation General Ledger Differs from Draw Amount Burn Rate No /Late/Inadequate Reports Sub-awards, Consultants, Contracts Duplicate Payments Excess Cash on Hand/Cost transfers Unreported Program Income AWARD END RISKS No /Late Final Reports Cost Transfers Spend-out Financial Adjustments Unmet Cost Share Dr. Brett M. Baker, 2010

16 Risk Assessment and Identification of Questionable Transactions Phase I Identify High Risk Institutions Phase II Identify Questionable Expenditures Agency Award Data Project reporting Cash draw downs Agency Award Data Project reporting Cash draw downs Awardee Data General ledger Subaward data Data Analytics Continuous monitoring of grant awards Data Analytics Apply risk indicators to GL. Compare to Agency data Review Questionable Transactions External Data Single Audits SAM (CCR, EPLS) External Data Single Audits SAM (CCR, EPLS) Dr. Brett Baker (2012)

17 Identification of Higher Risk Institutions and Transactions 17 Dr. Brett Baker AIGA. NSF-OIG

18 Anomalous Drawdown Patterns 18 $$ Start up costs Drawdown Spike Extinguishing Remaining Grant funds (before expiration) Extinguishing Remaining Grant funds (after expiration) Normal drawdown pattern Grant Award Grant Expiration 18 Dr. Brett Baker AIGA. NSF-OIG

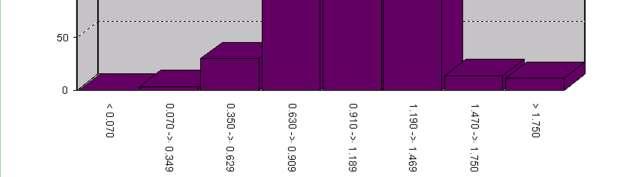

19 Burn Rate Actual vs Expected Actual 19 Expected Award Amount ($K) Expended ($K) % Expend Award Days Days Active % Total Days Delta 1 10,000 9,000 90% % ,000 4,000 80% % ,000 1,500 75% % , % % ,000 12,000 60% % ,000 5,000 50% % 0.57 Awardee Totals 48,000 32,495 68% 7,302 3,997 55% would be normal

20 Award Burn Rate Profile Comparison 20

21 Example: Equipment Charges Incurred Immediately Before Grant Expiration Date 21 GRANT EXPIRATION TRANSACTION LEDGER FINANCIAL GRANT ID OBJECT DESCRIPTION DATE DATE POST DATE AMOUNT XXXXX42 CONSTRUCTION AND ACQUISITION 09/30/ /30/ /06/ , Same day as expiration GRANT EXPIRATION TRANSACTION LEDGER FINANCIAL GRANT ID OBJECT DESCRIPTION DATE DATE POST DATE AMOUNT XXXXX27 INVENTORIAL EQUIPMENT 07/31/ /04/ /11/ , days before expiration GRANT EXPIRATION TRANSACTION LEDGER FINANCIAL GRANT ID OBJECT DESCRIPTION DATE DATE POST DATE AMOUNT XXXXX77 INVENTORIAL EQUIPMENT 08/31/ /16/ /10/ , days before expiration TOTAL 106,636.53

22 Travel Related to Award? 22 Just before award expiration NSF_OIG_Transaction Expiration Date Transaction Date Expense Type Amount GL Trans /25/ /31/2007 TRAVEL-IN-STATE 73,519 GL Trans /11/ /01/2010 TRAVEL - FOREIGN 41,474 GL Trans /02/ /31/2010 TRAVEL - OUT-OF-STATE 37,516 GL Trans /09/ /01/2010 TRAVEL-IN-STATE 28,905 GL Trans /11/ /15/2010 TRAVEL - FOREIGN 27,262 GL Trans /19/ /30/2010 TRAVEL-IN-STATE 20,975 Just after award expiration

23 OMB Grant Reform OMB effort to streamline financial assistance circulars Cost compliance and administrative principles Audit monitoring and follow-up Presidential Memorandum (February 2011) Administrative Flexibility, Lower Costs, and Better Results for State, Local, and Tribal Governments. Federal Register Notices and Final Rules Two postings: April 2012 and June 2013 Uniform Guidance finalized December 2013 Focus areas by OIG community Single Audit threshold and testing Effort reporting Cost Accounting Standards and Disclosure Statements Must vs Should language in final rules 23

24 Grant Reform Working Group OIG community Grant Reform Working Group 20 OIGs from 26 grant agencies Allison Lerner, NSF IG, is Chair Established in January 2012 to address proposed rule changes Opportunity to streamline makes sense, but need to maintain accountability Collaboration and Communication Process Regular meetings with stakeholders to share insight on concerns OMB (Danny Werfel, Norm Dong, Mark Reger, Victoria Collin, Gil Tran) Coordination with stakeholders: Council on Financial Assistance Reform (COFAR) 12 grant-making CFOs Council on Governmental Relations (COGR) over 180 research schools Federal Demonstration Partnership (FDP) Fed Govt/Schools streamline Financial Fraud Enforcement Task Force (DoJ) Not-for-profit community -AICPA, States, Schools, Tribal government 2013 OMB Webinar 24

25 OIG Community Focus Areas Single Audit threshold and testing Increasing threshold to $750,000, lose coverage of awardees Reduce compliance testing from 14 areas to 7 (cost testing still required) Responsibilities for OIGs (audit quality) and Agencies (program management) Annual time and effort reporting Streamline effort reporting and keep accountability Dropping semi-annual certification by a knowledgeable person Suitable means of verification need to show work performed NSF and HHS OIGs performing audits of 4 effort reporting pilots Cost accounting standards and Disclosure Statement (DS-2) DS-2 shows awardee can manage federal funds (systems, accounting) DS-2 filings required only for changes and new entities (1-2 a year) Helps differentiate between direct and indirect costs Must versus Should language in Uniform Guidance 25

26 Purchase Card Oversight Using Data Analytics Government Purchase Card Overview Simplified acquisition High risk for abuse without strong oversight DoD Joint Purchase Card Review Current work at NSF 26

27 Review objective DoD Joint Purchase Card Review 27 Develop automated oversight capability to identify anomalies in purchase card data that may indicate fraud or abuse Improve field research, reporting, process for audit and investigation Universe reviewed 15 million purchase card transactions ($9 billion) 200,000 cardholders (CH) and 40,000 authorizing officials (AO) Subject Matter Expert Conferences Structured brainstorming : 35 auditors, investigators, GSA officials Developed 115 indicators of potential fraud 46 codable Build targeted business rules to run against data

28 Top Performing Indicator Combinations 97% Entertainment Internet sites, Weekend/Holidays 28 67% Purchases from 1 vendor, Card Holder=AO 57% Internet transactions, 3rd party billing 53% Interesting vendors, many transactions 43% Even dollars, near limit, same vendor, vendor business w/few CHs

29 Joint Purchase Card Review Results Review Results 6.5 million transactions had at least 1 indicator 13,000 transactions (with combinations of indicators) 2000 cardholders and 1600 approving officials in 750 locations 8000 transactions (researched by base-level auditors ) 1300 questioned/investigated transactions (some level of misuse) Outcomes 275 cases with adverse action or prosecution $100 million in improper and fraudulent purchases Improved Defense agency oversight, policies and procedures Example: AO span of control < 7 CHs, closer oversight by APC Capability to embed risk indicators in credit card company systems Government purchase card abuse personal credit card abuse

30 Current NSF Purchase Card Work Approach similar to DoD joint purchase card review 30 Transaction universe 3 years of purchase card activity 230 card holders 34,000 transactions $17 million Risk-based approach to testing Worked closely with Investigations Developed risk indicators (previous and new)

31 Risk Factor Flags Approving official has a span of control of 5 or more card holders (Risk value = 1) MCC codes Transactions with Suspect MCC codes (Risk value = 2) Blocked MCC codes (Risk value = 3) One-to-One Transactions in which the merchant did business only with that particular NSF card holder (Risk value = 2) Weekend and holiday purchases Transactions on Saturday, Sunday, Holidays (Risk value = 3) 31

32 Risk Factor Flags- continued Suspect Level 3 Data Flags transactions with Level 3 data deemed suspect based on manual review. For example, possible personal purchase, possible split transaction, questionable legitimate business need. (Risk value = 3) 32 Possible Split Purchase Card holder has multiple purchases from the same merchant totaling more than $3,000 on the same day or within a few days. (Risk value = 3)

33 Example of Level 3 Data 33

34 Questions? 34 Dr. Brett M. Baker Assistant Inspector General for Audit National Science Foundation Office of Inspector General Phone:

A S S O C I A T I O N O F C O L L E G E A N D U N I V E R S I T Y A U D I T O R S A N N U A L C O N F E R E N C E S

National Science Foundation Office of Inspector General Audit Overview 1 ASSOCIATION OF COLLEGE AND UNIVERSITY AUDITORS ANNUAL CONFERENCE September 2012 Outline 2 Federal Offices of Inspector General National

National Science Foundation Office of Inspector General Audit Overview 1 ASSOCIATION OF COLLEGE AND UNIVERSITY AUDITORS ANNUAL CONFERENCE September 2012 Outline 2 Federal Offices of Inspector General National

NCURA Region II. Hot Topics in Research Administration 1. Denise Clark Associate Vice-President for Research, University of Maryland College Park

Hot Topics in Research Administration Denise Clark Associate Vice-President for Research, University of Maryland College Park Ann Holmes Assistant Dean of Finance & Administration, College of Behavioral

Hot Topics in Research Administration Denise Clark Associate Vice-President for Research, University of Maryland College Park Ann Holmes Assistant Dean of Finance & Administration, College of Behavioral

Here Come the Feds! What a Sponsor Audit is Looking for and How to Prepare Your Institution

Here Come the Feds! What a Sponsor Audit is Looking for and How to Prepare Your Institution Presented by: Richard Cordova, University of Washington Kevin Robinson, Auburn University Kim Ginn, Baker Tilly

Here Come the Feds! What a Sponsor Audit is Looking for and How to Prepare Your Institution Presented by: Richard Cordova, University of Washington Kevin Robinson, Auburn University Kim Ginn, Baker Tilly

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

University of Pittsburgh SPONSORED PROJECT FINANCIAL GUIDELINE Subject: SUBRECIPIENT MONITORING

I. Scope Subrecipient monitoring is the process by which the University selects, monitors, controls, and accounts for University subcontractors or subrecipients utilized on sponsored projects in accordance

I. Scope Subrecipient monitoring is the process by which the University selects, monitors, controls, and accounts for University subcontractors or subrecipients utilized on sponsored projects in accordance

Navigating the New Uniform Grant Guidance. Jack Reagan, Audit Partner Grant Thornton LLP. Grant Thornton. All rights reserved.

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

FOR OFFICIAL USE ONLY. Naval Audit Service. Audit Report. Government Commercial Purchase

FOR OFFICIAL USE ONLY Naval Audit Service Audit Report Government Commercial Purchase Card This report Transactions contains information exempt from at release Naval under the District Freedom of Information

FOR OFFICIAL USE ONLY Naval Audit Service Audit Report Government Commercial Purchase Card This report Transactions contains information exempt from at release Naval under the District Freedom of Information

Delayed Federal Grant Closeout: Issues and Impact

Delayed Federal Grant Closeout: Issues and Impact Natalie Keegan Analyst in American Federalism and Emergency Management Policy September 12, 2014 Congressional Research Service 7-5700 www.crs.gov R43726

Delayed Federal Grant Closeout: Issues and Impact Natalie Keegan Analyst in American Federalism and Emergency Management Policy September 12, 2014 Congressional Research Service 7-5700 www.crs.gov R43726

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS. National Historical Publications and Records Commission

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida

Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida") Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

Uniform Guidance Subpart D Administrative Requirements. Why This Session Is Needed. Lesson Overview & Module Objectives

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

Federal Rules for Sponsored Programs. Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

New Uniform Consolidated Grants Guidance

New Uniform Consolidated Grants Guidance From Accountability for Compliance to Accountability for Results The Honorable Jim Taylor and Robert Shea December 2014 Agenda Background Former circulars Consolidated

New Uniform Consolidated Grants Guidance From Accountability for Compliance to Accountability for Results The Honorable Jim Taylor and Robert Shea December 2014 Agenda Background Former circulars Consolidated

Something for Everyone: Adjusting to the OMB s Super Circular May 25, :30 10:10 am 2 CPE

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN

TO 2 CFR 200 (UNIFORM ADMIN") Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Understanding and Complying with Government Grants

Presents... Understanding and Complying with Objectives Obtain information to determine if applying for governmental grants is appropriate for your organization Obtain understanding of internal controls

Presents... Understanding and Complying with Objectives Obtain information to determine if applying for governmental grants is appropriate for your organization Obtain understanding of internal controls

Uniform Guidance Subpart D Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

2012 OMB Circular A-133 Compliance Supplement

2012 OMB Circular A-133 Compliance Supplement An Interactive Webinar July 24, 2012 Presented by Presented by: Stephen W. Blann, CPA, CGFM Director of Governmental Audit Quality Principal, Government/Nonprofit

2012 OMB Circular A-133 Compliance Supplement An Interactive Webinar July 24, 2012 Presented by Presented by: Stephen W. Blann, CPA, CGFM Director of Governmental Audit Quality Principal, Government/Nonprofit

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA NORTH CAROLINA DEPARTMENT OF COMMERCE STATEWIDE FEDERAL COMPLIANCE AUDIT PROCEDURES FOR THE YEAR ENDED JUNE 30, 2012 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR

STATE OF NORTH CAROLINA NORTH CAROLINA DEPARTMENT OF COMMERCE STATEWIDE FEDERAL COMPLIANCE AUDIT PROCEDURES FOR THE YEAR ENDED JUNE 30, 2012 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR

The OmniCircular - 2 CFR 200

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

PERALTA COMMUNITY COLLEGE DISTRICT SINGLE AUDIT REPORT JUNE 30, 2010

PERALTA COMMUNITY COLLEGE DISTRICT SINGLE AUDIT REPORT JUNE 30, 2010 TABLE OF CONTENTS JUNE 30, 2010 Independent Auditors' Report on Internal Control Over Financial Reporting and on Compliance and Other

PERALTA COMMUNITY COLLEGE DISTRICT SINGLE AUDIT REPORT JUNE 30, 2010 TABLE OF CONTENTS JUNE 30, 2010 Independent Auditors' Report on Internal Control Over Financial Reporting and on Compliance and Other

Circular A-133 Audits for Non-Profits Receiving Grants Preparing for Audits and Protecting Grant Eligibility Given Current Government Priorities

Presenting a live 110-minute teleconference with interactive Q&A Circular A-133 Audits for Non-Profits Receiving Grants Preparing for Audits and Protecting Grant Eligibility Given Current Government Priorities

Presenting a live 110-minute teleconference with interactive Q&A Circular A-133 Audits for Non-Profits Receiving Grants Preparing for Audits and Protecting Grant Eligibility Given Current Government Priorities

TRUCKEE MEADOWS COMMUNITY COLLEGE GRANTS AND CONTRACTS Internal Audit Report July 1, 2013 through June 30, 2014

TRUCKEE MEADOWS COMMUNITY COLLEGE GRANTS AND CONTRACTS Internal Audit Report July 1, 2013 through June 30, 2014 GENERAL OVERVIEW During the audit period, Truckee Meadows Community College (TMCC) had 44

TRUCKEE MEADOWS COMMUNITY COLLEGE GRANTS AND CONTRACTS Internal Audit Report July 1, 2013 through June 30, 2014 GENERAL OVERVIEW During the audit period, Truckee Meadows Community College (TMCC) had 44

Uniform Guidance Sponsored Projects Services

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Dollars & Sense: Federal Grant Financial

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

Insurance & Federal Claims Services (IFCS)

") Insurance & Federal Claims Services (IFCS) Why? s (IFCS) practice is a group of professionals dedicated to assisting governmental, nonprofit and corporate entities to expedite financial recovery and mitigation

Insurance & Federal Claims Services (IFCS) Why? s (IFCS) practice is a group of professionals dedicated to assisting governmental, nonprofit and corporate entities to expedite financial recovery and mitigation

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance)

") Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Seminar on Financial Management. VOCA s National Conference

Seminar on Financial Management VOCA s National Conference Financial Management Systems In summary, a Financial Management System must be able to: Record and report on the -- Receipt; Obligation; and Expenditure

Seminar on Financial Management VOCA s National Conference Financial Management Systems In summary, a Financial Management System must be able to: Record and report on the -- Receipt; Obligation; and Expenditure

Federal Grant Guidance Compliance

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

Financial Research Compliance. April 2013

Financial Research Compliance April 2013 Overview I. What is a Sponsored Award? II. Sponsored Awards at WFU III. Compliance IV. Hot Topics V. Audits VI. WFU Updates VII. Questions VIII. Contacts What is

Financial Research Compliance April 2013 Overview I. What is a Sponsored Award? II. Sponsored Awards at WFU III. Compliance IV. Hot Topics V. Audits VI. WFU Updates VII. Questions VIII. Contacts What is

PART 3 COMPLIANCE REQUIREMENTS

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION Overview The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribes, institutions of higher

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION Overview The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribes, institutions of higher

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

Grant Award and Contract Accounting

1 Grant Award and Contract Accounting 2 Overview on Grants State Agencies are responsible for tracking both State and Federal Grants for audit and reporting purposes Agencies can utilize a 5 digit grant

1 Grant Award and Contract Accounting 2 Overview on Grants State Agencies are responsible for tracking both State and Federal Grants for audit and reporting purposes Agencies can utilize a 5 digit grant

Federal Grants-in-Aid Administration: A Primer

Federal Grants-in-Aid Administration: A Primer Natalie Keegan Analyst in American Federalism and Emergency Management Policy October 3, 2012 CRS Report for Congress Prepared for Members and Committees

Federal Grants-in-Aid Administration: A Primer Natalie Keegan Analyst in American Federalism and Emergency Management Policy October 3, 2012 CRS Report for Congress Prepared for Members and Committees

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Federal Grants and Financial Assistance 2017 Training Catalog

1 P a g e Who are we? Meet Colleague Consulting Colleague Consulting LLC is a 19-year-old small business specializing in training, human resource development, and organizational development services for

1 P a g e Who are we? Meet Colleague Consulting Colleague Consulting LLC is a 19-year-old small business specializing in training, human resource development, and organizational development services for

Grant Closeout Process

Grant Closeout Process Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients administrative and their subrecipients

Grant Closeout Process Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients administrative and their subrecipients

AUDITS & REVIEWS OF SCHOOL BASED SERVICES T I M K U B U K A B E E R S I N G H

AUDITS & REVIEWS OF SCHOOL BASED SERVICES T I M K U B U K A B E E R S I N G H INTRODUCTIONS Tim Kubu, Manager MDHHS Bureau of Audit, Audit Division, Audit & Review Section 13 Years with State of MI Kabeer

AUDITS & REVIEWS OF SCHOOL BASED SERVICES T I M K U B U K A B E E R S I N G H INTRODUCTIONS Tim Kubu, Manager MDHHS Bureau of Audit, Audit Division, Audit & Review Section 13 Years with State of MI Kabeer

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT)

") GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

Are You Ready for This? The New Uniform Guidance 2 CFR 200

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

Nonprofit Single Audit and Major Program Determination Worksheet

40 HUD 8/14 : Nonprofit Single Audit and Major Program Determination Worksheet Entity: Completed by: Statement of Financial Position Date: Date: IMPORTANT INFORMATION ABOUT CHANGES TO THE SINGLE AUDIT

40 HUD 8/14 : Nonprofit Single Audit and Major Program Determination Worksheet Entity: Completed by: Statement of Financial Position Date: Date: IMPORTANT INFORMATION ABOUT CHANGES TO THE SINGLE AUDIT

Report No. DODIG May 31, Defense Departmental Reporting System-Budgetary Was Not Effectively Implemented for the Army General Fund

Report No. DODIG-2012-096 May 31, 2012 Defense Departmental Reporting System-Budgetary Was Not Effectively Implemented for the Army General Fund Additional Copies To obtain additional copies of this report,

Report No. DODIG-2012-096 May 31, 2012 Defense Departmental Reporting System-Budgetary Was Not Effectively Implemented for the Army General Fund Additional Copies To obtain additional copies of this report,

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. AUSPAN Martha Taylor

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Ohio Enterprise Grants & Common Grants Compliance Issues

Ohio Enterprise Grants & Common Grants Compliance Issues Stacie Massey Ohio Office of Budget and Management June 12, 2018 The Growing Grants Business The State of Ohio manages $28 billion in federal grant

Ohio Enterprise Grants & Common Grants Compliance Issues Stacie Massey Ohio Office of Budget and Management June 12, 2018 The Growing Grants Business The State of Ohio manages $28 billion in federal grant

GATA GRANT ACCOUNTABILITY AND TRANSPARENCY ACT OVERVIEW T.H.E. CONFERENCE

GATA GRANT ACCOUNTABILITY AND TRANSPARENCY ACT OVERVIEW T.H.E. CONFERENCE 2.28.17 Topics of Discussion GATA Myths Applicability of GATA GATA Overview What s New Roles and Responsibilities Consequences

GATA GRANT ACCOUNTABILITY AND TRANSPARENCY ACT OVERVIEW T.H.E. CONFERENCE 2.28.17 Topics of Discussion GATA Myths Applicability of GATA GATA Overview What s New Roles and Responsibilities Consequences

OMB Uniform Guidance ( UG ) Briefing. ASRSP & OSR Brown Bag Tuesday, January 27 th

Briefing. ASRSP & OSR Brown Bag Tuesday, January 27 th") OMB Uniform Guidance ( UG ) Briefing ASRSP & OSR Brown Bag Tuesday, January 27 th Background The UG is the single biggest regulatory change in the last fifty years in research administration Interesting

OMB Uniform Guidance ( UG ) Briefing ASRSP & OSR Brown Bag Tuesday, January 27 th Background The UG is the single biggest regulatory change in the last fifty years in research administration Interesting

Question and Answer Transcript Follow-up to the December 7, 2011 webinar on: Proper Management of Federal Grants - Support of Salaries and Wages

Question and Answer Transcript Follow-up to the December 7, 2011 webinar on: Proper Management of Federal Grants - Support of Salaries and Wages Acronyms used in the Questions and Answers (alphabetical

Question and Answer Transcript Follow-up to the December 7, 2011 webinar on: Proper Management of Federal Grants - Support of Salaries and Wages Acronyms used in the Questions and Answers (alphabetical

Roadmap to the Uniform Grant Guidance for School Districts

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

2009 American Recovery and Reinvestment Act (ARRA)

") 2009 American Recovery and Reinvestment Act (ARRA) Understanding Compliance and Reporting Requirements Associated with ARRA Stimulus Funds November 19, 2009 2009 American Recovery & Reinvestment Act Today

2009 American Recovery and Reinvestment Act (ARRA) Understanding Compliance and Reporting Requirements Associated with ARRA Stimulus Funds November 19, 2009 2009 American Recovery & Reinvestment Act Today

AUDIT OF THE OFFICE OF COMMUNITY ORIENTED POLICING SERVICES AND OFFICE OF JUSTICE PROGRAMS GRANTS AWARDED TO THE CITY OF BOSTON, MASSACHUSETTS

AUDIT OF THE OFFICE OF COMMUNITY ORIENTED POLICING SERVICES AND OFFICE OF JUSTICE PROGRAMS GRANTS AWARDED TO THE CITY OF BOSTON, MASSACHUSETTS EXECUTIVE SUMMARY The Department of Justice Office of the

AUDIT OF THE OFFICE OF COMMUNITY ORIENTED POLICING SERVICES AND OFFICE OF JUSTICE PROGRAMS GRANTS AWARDED TO THE CITY OF BOSTON, MASSACHUSETTS EXECUTIVE SUMMARY The Department of Justice Office of the

Department of Contracts, Grants and Financial Administration, Texas Education Agency 1/26/18

Federal Grant Procurement Rules and Regulations and Federal Fiscal Monitoring Requirements Cory Green, Associate Commissioner Department of Contracts, Grants and Financial Administration Texas January

Federal Grant Procurement Rules and Regulations and Federal Fiscal Monitoring Requirements Cory Green, Associate Commissioner Department of Contracts, Grants and Financial Administration Texas January

CURRENT COGR PRIORITIES - BY COMMITTEE (7/10/17)

") CURRENT COGR PRIORITIES - BY COMMITTEE (7/10/17) No. 1 Student Financial Aid and "Securing Student Information" and Compliance Supplement New single audit requirement. Delayed until 2018. MEDIUM Pending

CURRENT COGR PRIORITIES - BY COMMITTEE (7/10/17) No. 1 Student Financial Aid and "Securing Student Information" and Compliance Supplement New single audit requirement. Delayed until 2018. MEDIUM Pending

Wake Forest University Financial Services: Grants Accounting and Compliance

Wake Forest University Financial Services: Grants Accounting and Compliance 1 WFU Policies and Procedures a Policies b Fiscal Administration i Award Notification 1 The Office of Research and Sponsored

Wake Forest University Financial Services: Grants Accounting and Compliance 1 WFU Policies and Procedures a Policies b Fiscal Administration i Award Notification 1 The Office of Research and Sponsored

Welcome. Please help yourself to breakfast.

Welcome Please help yourself to breakfast. 1 Agenda 8:00-8:45am Registration and Breakfast 8:45-8:55am Welcome 8:55-9:25am Rhea Hubbard, OMB Office of Federal Financial Management 9:25-9:55am Q&A and Discussion

Welcome Please help yourself to breakfast. 1 Agenda 8:00-8:45am Registration and Breakfast 8:45-8:55am Welcome 8:55-9:25am Rhea Hubbard, OMB Office of Federal Financial Management 9:25-9:55am Q&A and Discussion

Jason Galloway, Associate Controller HSC Contract and Grant Accounting

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

To the Board of Overseers of Harvard College:

Independent Auditor s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing

Independent Auditor s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing

Felipe Lopez, Vavrinek, Trine, Day & Co., LLP

San Luis Obispo County Community College District & San Luis Obispo County Office of Education 2012 F d l C li T i i 2012 Federal Compliance Training Felipe Lopez, Vavrinek, Trine, Day & Co., LLP Objectives

San Luis Obispo County Community College District & San Luis Obispo County Office of Education 2012 F d l C li T i i 2012 Federal Compliance Training Felipe Lopez, Vavrinek, Trine, Day & Co., LLP Objectives

Topics 6/28/2017. U.S. Department of Transportation Office of Inspector General (OIG) OIG Audits Impact DOT Oversight. Heads Up on Future Issues

OIG Audits Impact DOT Oversight. Heads Up on Future Issues") U.S. Department of Transportation (OIG) What s New with the OIG? Recent Activity and Future Audit Plans Impacting the AASHTO Community AASHTO Internal/External Audit Meeting Missoula, Montana July 11,

U.S. Department of Transportation (OIG) What s New with the OIG? Recent Activity and Future Audit Plans Impacting the AASHTO Community AASHTO Internal/External Audit Meeting Missoula, Montana July 11,

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist 1 Learning Objectives Participants will gain an understanding of the elements of preaward and how to think through required

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist 1 Learning Objectives Participants will gain an understanding of the elements of preaward and how to think through required

Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs

3/15/14 Draft Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs Prepared for the Council of Chief State School Officers Federal

3/15/14 Draft Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs Prepared for the Council of Chief State School Officers Federal

The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

Subrecipient Monitoring Procedures

Subrecipient Monitoring Procedures This procedure describes the proper management of subrecipient activity under Purdue sponsored program awards. Definitions Award: An award is a binding agreement between

Subrecipient Monitoring Procedures This procedure describes the proper management of subrecipient activity under Purdue sponsored program awards. Definitions Award: An award is a binding agreement between

ort ich-(vc~ Office of the Inspector General Department of Defense USE OF THE INTERNATIONAL MERCHANT PURCHASE AUTHORIZATION CARD

ort USE OF THE INTERNATIONAL MERCHANT PURCHASE AUTHORIZATION CARD Report Number 99-129 April 12, 1999 Office of the Inspector General Department of Defense ich-(vc~ INTERNET DOCUMENT INFORMATION FORM A.

ort USE OF THE INTERNATIONAL MERCHANT PURCHASE AUTHORIZATION CARD Report Number 99-129 April 12, 1999 Office of the Inspector General Department of Defense ich-(vc~ INTERNET DOCUMENT INFORMATION FORM A.

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY. Office of Contracts and Grants December, 2014

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

2010 Mauldin & Jenkins Single Audits for for Auditees

2010 Mauldin & Jenkins Single Audits for Auditees SINGLE AUDITS FOR AUDITEES Mauldin & Jenkins July 22, 2010 Macon August 3, 2010 - Atlanta PRESENTER Hope Pendergrass Manager Macon Office hpendergrass@mjcpa.com

2010 Mauldin & Jenkins Single Audits for Auditees SINGLE AUDITS FOR AUDITEES Mauldin & Jenkins July 22, 2010 Macon August 3, 2010 - Atlanta PRESENTER Hope Pendergrass Manager Macon Office hpendergrass@mjcpa.com

Grant Administration Glossary of Commonly-Used Terms in Sponsored Programs

Page 1 of 6 Grant Administration Allowability: The determination of whether or not costs can be charged to a sponsored project as a direct or indirect cost. Allocability: A cost is allocable to a particular

Page 1 of 6 Grant Administration Allowability: The determination of whether or not costs can be charged to a sponsored project as a direct or indirect cost. Allocability: A cost is allocable to a particular

NECA Update The New Uniform Guidance 2 CFR 200

NECA Update The New Uniform Guidance 2 CFR 200 September 23, 2014 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B

NECA Update The New Uniform Guidance 2 CFR 200 September 23, 2014 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B

Agency for Health Care Administration Response to DFS Audit of Selected Agency Contracts and Grants Active 7/1/14 through 6/30/15

Contracts and Grant Agreements Each service contract and grant agreement must contain a clear scope of work, deliverables directly related to the scope of work, minimum required levels of service, criteria

Contracts and Grant Agreements Each service contract and grant agreement must contain a clear scope of work, deliverables directly related to the scope of work, minimum required levels of service, criteria

Office of Inspector General Audit Tips for FEMA Public Assistance Grant Recipients and Subrecipients

Office of Inspector General Audit Tips for FEMA Public Assistance Grant Recipients and Subrecipients Tonda L. Hadley, Director Central Regional Office-South Office of Emergency Management Oversight Texas

Office of Inspector General Audit Tips for FEMA Public Assistance Grant Recipients and Subrecipients Tonda L. Hadley, Director Central Regional Office-South Office of Emergency Management Oversight Texas

Grants Financial Procedures (Post-Award) v. 2.0

v. 2.0") Grants Financial Procedures (Post-Award) v. 2.0 1 Grants Financial Procedures (Post Award) Version Number: 2.0 Procedures Identifier: Superseded Procedure(s): BU-PR0001 N/A Date Approved: 9/1/2013 Effective

Grants Financial Procedures (Post-Award) v. 2.0 1 Grants Financial Procedures (Post Award) Version Number: 2.0 Procedures Identifier: Superseded Procedure(s): BU-PR0001 N/A Date Approved: 9/1/2013 Effective

SINGLE AUDIT REPORTS

S A F E T Y, S E R V I C E A N D F I N A N C I A L R E SPO N S I B I LIT Y SINGLE AUDIT REPORTS FOR THE FISCAL YEAR ENDED JUNE 30, 2017 Single Audit Reports issued in Accordance with Title 2 U.S. Code

S A F E T Y, S E R V I C E A N D F I N A N C I A L R E SPO N S I B I LIT Y SINGLE AUDIT REPORTS FOR THE FISCAL YEAR ENDED JUNE 30, 2017 Single Audit Reports issued in Accordance with Title 2 U.S. Code

3 rd Annual Symposium for Research Administrators

3 rd Annual Symposium for Research Administrators Cost Transfer Policy Martha Martin, CRA, Grants Administration, School of Information and Library Science Sarah Van Heusen, MHA, Director of Research Administration,

3 rd Annual Symposium for Research Administrators Cost Transfer Policy Martha Martin, CRA, Grants Administration, School of Information and Library Science Sarah Van Heusen, MHA, Director of Research Administration,

Audit Report Grant Closure Processes Follow-up Review

Audit Report Grant Closure Processes Follow-up Review GF-OIG-16-017 Geneva, Switzerland Table of Contents I. Background... 3 II. Objectives, Scope, Methodology and Rating... 5 1) Objectives... 5 2) Scope&

Audit Report Grant Closure Processes Follow-up Review GF-OIG-16-017 Geneva, Switzerland Table of Contents I. Background... 3 II. Objectives, Scope, Methodology and Rating... 5 1) Objectives... 5 2) Scope&

The Uniform Guidance (2 CFR, Part 200)

") WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

Department of Defense DIRECTIVE. SUBJECT: Under Secretary of Defense (Comptroller) (USD(C))/Chief Financial Officer (CFO), Department of Defense

(USD(C))/Chief Financial Officer (CFO), Department of Defense") Department of Defense DIRECTIVE NUMBER 5118.3 January 6, 1997 SUBJECT: Under Secretary of Defense (Comptroller) (USD(C))/Chief Financial Officer (CFO), Department of Defense DA&M References: (a) Title

Department of Defense DIRECTIVE NUMBER 5118.3 January 6, 1997 SUBJECT: Under Secretary of Defense (Comptroller) (USD(C))/Chief Financial Officer (CFO), Department of Defense DA&M References: (a) Title

Emory Research A to Z ERAZ

Emory Research A to Z ERAZ July 17, 2014 Whitehead Auditorium G01 Whitehead Building Agenda Controlled Substances Sub Award Processing RAS Updates SAM Kiosk Federal Updates OSP/OGCA Training Updates Christine

Emory Research A to Z ERAZ July 17, 2014 Whitehead Auditorium G01 Whitehead Building Agenda Controlled Substances Sub Award Processing RAS Updates SAM Kiosk Federal Updates OSP/OGCA Training Updates Christine

Office of Sponsored Programs RESEARCH ADMINISTRATORS FORUM. December 2017

Office of Sponsored Programs RESEARCH ADMINISTRATORS FORUM December 2017 Agenda Feedback on Subawards Process What is FFATA and what does it mean to the Research Administration community at NYU? University

Office of Sponsored Programs RESEARCH ADMINISTRATORS FORUM December 2017 Agenda Feedback on Subawards Process What is FFATA and what does it mean to the Research Administration community at NYU? University

Combating Medicaid Fraud & Abuse NCSL New England Fiscal Leaders Meeting February 22, 2013

Combating Medicaid Fraud & Abuse NCSL New England Fiscal Leaders Meeting February 22, 2013 Kavita Choudhry State Health Care Spending Project Pew Charitable Trusts Pressure on state and local budgets Source:

Combating Medicaid Fraud & Abuse NCSL New England Fiscal Leaders Meeting February 22, 2013 Kavita Choudhry State Health Care Spending Project Pew Charitable Trusts Pressure on state and local budgets Source:

How to Manage Externally Funded Grants PROJECTS - FUND CODE 501 or 502

How to Manage Externally Funded Grants PROJECTS - FUND CODE 501 or 502 What is a Grant? Funding that is coming from a source external to Wesleyan Project conceived by the Investigator Response to a solicitation

How to Manage Externally Funded Grants PROJECTS - FUND CODE 501 or 502 What is a Grant? Funding that is coming from a source external to Wesleyan Project conceived by the Investigator Response to a solicitation

Trinity Valley Community College. Grants Accounting Policy and Procedures 2012

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

Financial Grants Management. Session Outline. Grants Management Roles 4/19/10

Financial Grants Management Presented by: Donna Teague Grant Accounting Supervisor El Paso County Auditor s Office Small Counties Large Counties Grants Management Records Session Outline New Application

Financial Grants Management Presented by: Donna Teague Grant Accounting Supervisor El Paso County Auditor s Office Small Counties Large Counties Grants Management Records Session Outline New Application

MAXIMUS Higher Education Practice

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director, MAXIMUS Jason Guilbeault, Senior Consultant, MAXIMUS 1 MAXIMUS Higher Education Practice Headquartered in Northbrook,

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director, MAXIMUS Jason Guilbeault, Senior Consultant, MAXIMUS 1 MAXIMUS Higher Education Practice Headquartered in Northbrook,

Hello. National Grants Management Association Monthly Training November 16, Eric J. Russell, CIA, CGAP, CGMS, MPA Crowe Horwath LLP

Hello. National Grants Management Association Monthly Training November 16, 2016 Eric J. Russell, CIA, CGAP, CGMS, MPA Crowe Horwath LLP 2016 Crowe 2016 Crowe Horwath Horwath LLP LLP Agenda Third Party

Hello. National Grants Management Association Monthly Training November 16, 2016 Eric J. Russell, CIA, CGAP, CGMS, MPA Crowe Horwath LLP 2016 Crowe 2016 Crowe Horwath Horwath LLP LLP Agenda Third Party

Administrative and Indirect Costs. What s the difference?

Administrative and Indirect Costs What s the difference? Learning Objectives Define administrative costs. Describe the difference between direct and indirect costs. Describe what an indirect cost rate

Administrative and Indirect Costs What s the difference? Learning Objectives Define administrative costs. Describe the difference between direct and indirect costs. Describe what an indirect cost rate

APPENDIX VII OTHER AUDIT ADVISORIES

APPENDIX VII OTHER AUDIT ADVISORIES I. Effect of Changes to Generally Applicable Compliance Requirements in the 2015 Supplement In the 2015 Supplement, OMB has removed several of the compliance requirements

APPENDIX VII OTHER AUDIT ADVISORIES I. Effect of Changes to Generally Applicable Compliance Requirements in the 2015 Supplement In the 2015 Supplement, OMB has removed several of the compliance requirements

Department of Defense Charge Card Task Force Status Report

Department of Defense Charge Card Task Force Status Report December 2002 The implementation of charge card programs in the Department of Defense (DoD) is a cost-saving business initiative that reforms

Department of Defense Charge Card Task Force Status Report December 2002 The implementation of charge card programs in the Department of Defense (DoD) is a cost-saving business initiative that reforms

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS Agenda Uniform Guidance Summary General Federal Procurement Laws Thresholds and Implications Sole Source Vendors Cooperative Purchasing

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS Agenda Uniform Guidance Summary General Federal Procurement Laws Thresholds and Implications Sole Source Vendors Cooperative Purchasing

A-133 Single Audits: Common Audit Findings & Ways to Mitigate and Prevent Them

A-133 Single Audits: Common Audit Findings & Ways to Mitigate and Prevent Them Wayne Finley, MBA, CGMS Mayor s Office Education & Government Services City of St. Petersburg, Florida Session Objectives

A-133 Single Audits: Common Audit Findings & Ways to Mitigate and Prevent Them Wayne Finley, MBA, CGMS Mayor s Office Education & Government Services City of St. Petersburg, Florida Session Objectives

Overview of the New EDGAR (formerly the Uniform Grants Guidance)

") Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

December 26, 2014 NEW ADDITIONAL December 26, 2014 beginning December 26, /31/15, 6/30/16 Contents Reference Origin Appendix

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews Denise Dusek, MPA Federal Funding Specialist ESC 20 Image obtained from google.com Education Service Center, Region 20 May 2018 2 1 Participants

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews Denise Dusek, MPA Federal Funding Specialist ESC 20 Image obtained from google.com Education Service Center, Region 20 May 2018 2 1 Participants

EXHIBIT A SPECIAL PROVISIONS

EXHIBIT A SPECIAL PROVISIONS The following provisions supplement or modify the provisions of Items 1 through 9 of the Integrated Standard Contract, as provided herein: A-1. ENGAGEMENT, TERM AND CONTRACT

EXHIBIT A SPECIAL PROVISIONS The following provisions supplement or modify the provisions of Items 1 through 9 of the Integrated Standard Contract, as provided herein: A-1. ENGAGEMENT, TERM AND CONTRACT

HUD-US DEPT OF HOUSING & URBAN DEVELOPMENT: Financial Grant Reporting. Ladies, and gentlemen, thank you for standing by and welcome to the

Final Transcript HUD-US DEPT OF HOUSING : Financial Grant Reporting SPEAKERS Robin Booth PRESENTATION Moderator Ladies, and gentlemen, thank you for standing by and welcome to the Financial Grant Reporting

Final Transcript HUD-US DEPT OF HOUSING : Financial Grant Reporting SPEAKERS Robin Booth PRESENTATION Moderator Ladies, and gentlemen, thank you for standing by and welcome to the Financial Grant Reporting

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS. AOA Conference Sacramento, CA January 12, 2014

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS AOA Conference Sacramento, CA January 12, 2014 Agenda 1. Introduction 2. History 3. Learning Objectives 4.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS AOA Conference Sacramento, CA January 12, 2014 Agenda 1. Introduction 2. History 3. Learning Objectives 4.

PS Operations & Management The Future of Grants Management

PS Operations & Management The Future of Grants Management Delivering Public Service for the Future Grants flow through public bodies in the US in a vast, complex series of channels FEDERAL 100% Grantor

PS Operations & Management The Future of Grants Management Delivering Public Service for the Future Grants flow through public bodies in the US in a vast, complex series of channels FEDERAL 100% Grantor

Schedule of Expenditure

Schedule of Expenditure of Federal Awards (SEFA) TACA Fall Conference October 21, 2015 Federal Grants to State and Local Governments 1960 2017 2 Uniform Grant Guidance 2 CFR 200 December 2013, OMB released

Schedule of Expenditure of Federal Awards (SEFA) TACA Fall Conference October 21, 2015 Federal Grants to State and Local Governments 1960 2017 2 Uniform Grant Guidance 2 CFR 200 December 2013, OMB released

CHAPTER Senate Bill No. 400

CHAPTER 98-91 Senate Bill No. 400 An act relating to state financial accountability; creating the Florida Single Audit Act; providing intent and findings; creating s. 216.3491, F.S.; providing purposes

CHAPTER 98-91 Senate Bill No. 400 An act relating to state financial accountability; creating the Florida Single Audit Act; providing intent and findings; creating s. 216.3491, F.S.; providing purposes

University of Pittsburgh

I. Guideline Background University sponsors are increasingly relying on institutions for the development of adequate compliance programs for the financial administration of grants and contracts. An adequate

I. Guideline Background University sponsors are increasingly relying on institutions for the development of adequate compliance programs for the financial administration of grants and contracts. An adequate

MANAGER S TOOLKIT FOR A SUCCESSFUL FINANCIAL STATEMENT AUDIT

MANAGER S TOOLKIT FOR A SUCCESSFUL FINANCIAL STATEMENT AUDIT Ms. Lorin Venable, DoD OIG ASMC PDI Workshop #79 June 2, 2017 1 Agenda OIG Audit History Complexity of DoD FY 2016 Audit Opinions Status of

MANAGER S TOOLKIT FOR A SUCCESSFUL FINANCIAL STATEMENT AUDIT Ms. Lorin Venable, DoD OIG ASMC PDI Workshop #79 June 2, 2017 1 Agenda OIG Audit History Complexity of DoD FY 2016 Audit Opinions Status of

UNIFORM GUIDANCE IMPLEMENTATION

UNIFORM GUIDANCE IMPLEMENTATION Presented by Sara Judd, OSR Consultant October 2014 Uniform Guidance Implementation what we know and what we re guessing Ready, Set, Go 2014 Fred Hutchinson Cancer Research

UNIFORM GUIDANCE IMPLEMENTATION Presented by Sara Judd, OSR Consultant October 2014 Uniform Guidance Implementation what we know and what we re guessing Ready, Set, Go 2014 Fred Hutchinson Cancer Research