Here Come the Feds! What a Sponsor Audit is Looking for and How to Prepare Your Institution

|

|

|

- Nathaniel Norton

- 6 years ago

- Views:

Transcription

1 Here Come the Feds! What a Sponsor Audit is Looking for and How to Prepare Your Institution Presented by: Richard Cordova, University of Washington Kevin Robinson, Auburn University Kim Ginn, Baker Tilly

2 Introductions Richard Cordova Executive Director, Internal Audit University of Washington (206) Kevin Robinson Executive Director, Internal Audit Auburn University (334) Kim Ginn Principal Baker Tilly (703)

3 Session Objectives 1. Determine areas on which federal auditors are most likely to focus, and common findings from the field 2. Apply best practices for surviving a sponsor audit 3. Identify how internal audit can provide assurance and assess effectiveness of research administration processes to foster a stronger research environment

4 Agenda Types of Audits Conducted Who is involved in Audits The FY 2015 Audit Plans for the Major Research Agencies Common Audit Findings Recent Settlements and Audit Findings OIG Audits Recent Settlements and Audit Findings False Claims Act Settlements Practical Advice to Ease the Pain of an Audit How Internal Audit can Help References and Resources

5 Types of Audits

6 Types of Audits Conducted Government Reduce and Eliminate Fraud, Waste, and Abuse Internal Audit Improve processes and controls Reduce the number of surprises from a government audit

7 Sponsor/Office of Inspector General (OIG) Audits Sponsoring agencies and/or their OIG may conduct audits of recipients. Audits may be focused on a specific program/project, general research administration operations, or the larger research portfolio. Sponsor audits may be prior to the receipt of an award, during the award s life, or at its completion.

8 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards OMB has streamlined and consolidated its guidance for grant recipients in a single document. The guidance raises the minimum audit (formerly detailed in Circular A-133) threshold from $500,000 to $750,000. Guidance is effective for awards (or funding increments) issued after December 26, Single Audit requirements are effective for fiscal years beginning on or after December 26, 2014.

9 Increased Focus on Internal Controls While grant recipients have always been required to establish and maintain effective internal controls to manage federal awards, the current guidance does not specify how to determine if internal controls are effective. The new guidance states that internal controls should be in compliance with the internal control requirements issued by: Government Accountability Office (GAO) Standards for Internal Control in the Federal Government (Green Book) AND/OR Committee of Sponsoring Organizations of the Treadway Commissions (COSO) Internal Control Integrated Framework OMB believes explicitly requiring compliance with the GAO Green Book and COSO framework will help mitigate the risks of waste, fraud and abuse on federal awards.

10 Internal Audit? Internal Audit s major responsibilities include: Reporting on internal controls Conducting internal audits of various offices and programs within a department Conducting internal investigations AND MAY INCLUDE: Coordinating audits and resolving audit findings by external auditors

11 Who is Involved in Federal Audits

12 OIG Audit Conducted by the OIG of a federal sponsoring agency (e.g., National Institutes of Health (NIH), National Science Foundation (NSF)). OIG audits specific awards and awardee institutions to determine whether costs charged to the award were allowable, reasonable, and properly allocated. Audits aim to identify uneconomical practices that may be altered to better use taxpayer funds and support the mission of the agency.

13 Federal Agencies Federal Bureau of Investigations (FBI) Homeland Security Federal Attorneys Office (Department of Justice) Federal Civil Attorneys Office Office of Human Research Protection (OHRP) Office of Research Integrity (ORI) Agency Finance Officers

14 Institutional Resources Involved in Audits Research Compliance Officer Grants Administration Director Institutional Review Board Internal Audit Grants Accounting Office Office of Sponsored Programs General Counsel President

15 FY 2015 Audit Work Plans

16 NIH FY 2015 OIG Audit Work Plans Superfund Financial Activities for FY 2014 Colleges and Universities Compliance with Cost Principles Oversight of Grants Management Policy Implementation Use of Appropriated Funds for Contracting Review of the National Institute of Environmental Health Sciences Funding for Bisphenol A Safety Research Added as part of the mid-year work plan update

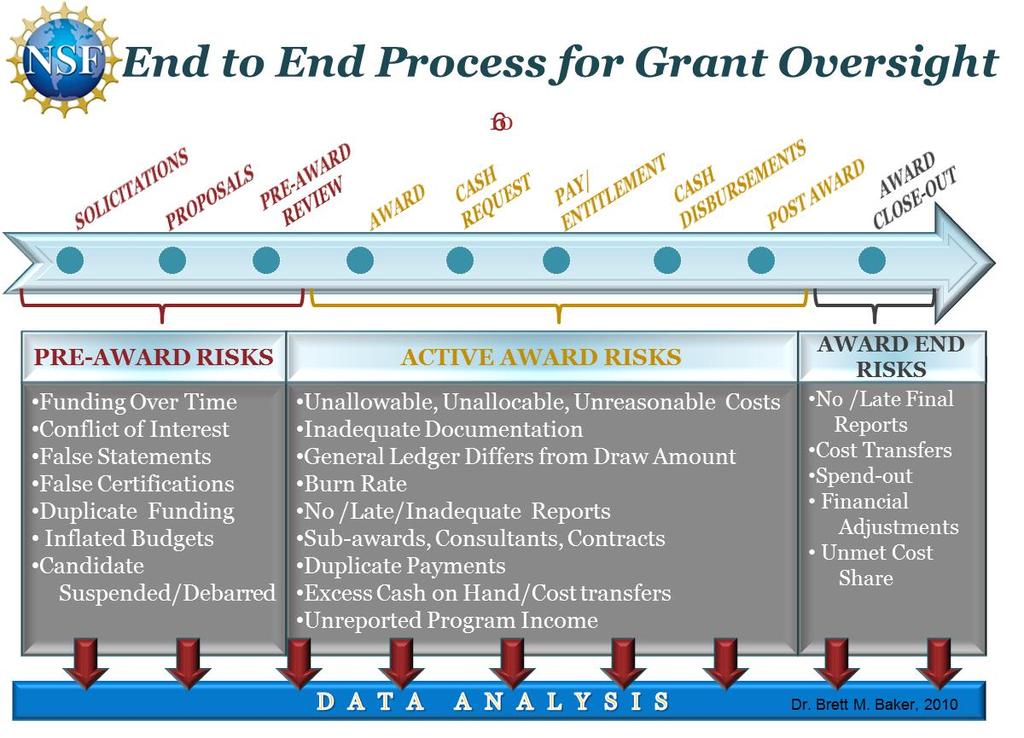

17 NSF FY 2015 OIG Audit Workplan Internal Focus: Relocation of NSF Headquarters Health and Safety in the U.S. Antarctic Program (USAP) FY 2014 and 2015 Financial Statement Audits FY 2014 and 2015 FISMA Evaluations NSF s Compliance with Improper Payments Elimination and Recovery Act (IPERA) Management Fees Inspection Travel Cards Conference Spending Cloud Computing Inspection External Focus: Awardees Management of American Recovery and Reinvestment Act (ARRA) Funds R/V Sikuliaq Incurred Costs or Accounting System Audits of 16 Institutions with ARRA Funds Assessment of Payroll Certification Pilots Audits of Various Universities, Non-Profits, and For-Profit Entities Review of Quality of Single Audits

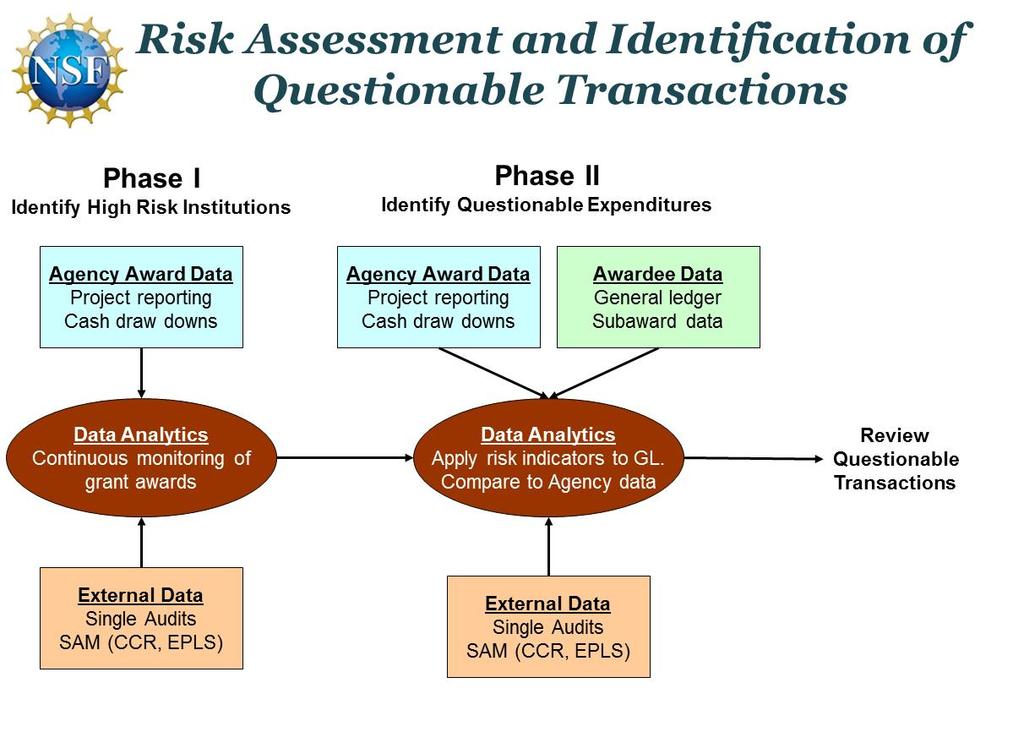

18 NSF Data Analytics Approach Data analytics-driven, risk-based methodology to improve oversight Identify institutions that may not use federal funds properly Techniques to surface questionable expenditures Life cycle approach to oversight Mapping of end-to-end process to identify controls 100% review of key financial and program information Focus attention to award and expenditure anomalies Complements traditional oversight approaches Techniques to review process and transactions are similar Transactions of questionable activities are targeted Recipients and Agency Officials can use data analytics Identify high risk activities through continuous monitoring

19

20

21 Common Audit Finding Areas

22 Consistent Audit Finding Areas The low hanging fruit Though each sponsoring agency s OIG develops an annual work plan, universities across the country have consistently received audit findings in a number of key areas over the past several years: Consistent treatment of direct and indirect costs Cost allowability Cost transfers Payroll distribution/effort reporting Subrecipient monitoring Tracking and reporting of cost sharing

23 Emerging Audit Finding Areas The changing landscape of federal regulations In addition to the standard audit findings that have been a focus of OIGs in the past, a number of other audit areas have emerged recently due to changing federal priorities and/ or regulations, including: Adequacy of internal controls Data management and security Direct charging of administrative costs Quality control reviews of A-133 audits

24 Case Study: University of Washington NSF Data Analytics Audit

25 Practical Advice to Ease the Pain of an Audit

26 How to Prepare Your Institution for an Audit General Tips 1. Identify the agency involved Review that agency s audit plan and any recently published audit reports (all information from federal sponsors is public information, and can typically be found online) Identify who will be conducting the review (many agencies are now outsourcing their audits)

27 How to Prepare Your Institution for an Audit General Tips (cont.) 2. Understand the focus area of the audit Carefully read the audit notification and any related requests for information Prepare as much documentation as possible in advance, and try to anticipate what materials the auditors may need Be sure to discuss any questions regarding requested information when needed You don t want to provide more information than needed, but also want to make sure the information requested and/or provided is what the auditors actually need

28 How to Prepare Your Institution for an Audit General Tips (cont.) 3. Assign an individual to be the audit liaison This will help make the audit process as painless and efficient as possible, both for your institution and the auditors Having one individual responsible for coordinating all audit requests will allow for greater understanding of the information needed and received by the auditors

29 How to Prepare Your Institution for an Audit General Tips (cont.) 4. Schedule the audit at a convenient time (if possible) Audits should be conducted when the organization is able to focus on the requests It s okay to tell an auditor that you want your accounting department to be heavily involved, but they need to get through a particular reporting period, etc. Remember, auditors are people, too!

30 How Internal Audit Can Help

31 Federal Recommendations Examine operations and programs to identify fraud vulnerabilities Establish an adequate and effective system of accounting, internal controls, records control and records retention Financial management systems Procurement systems Time and effort reporting systems Monitoring activities Adherence to terms and conditions of awards

32 Federal Recommendations (cont.) Implement an internal compliance and ethics program 2005: Draft OIG Compliance Program Guidance for Recipients of PHS Research Awards Standard elements (as outlined in the Federal Sentencing Guidelines) Implementing written policies and procedures Conducting internal monitoring and auditing Enforcing standards through well publicized disciplinary guidelines Responding promptly to detected problems and undertaking corrective action Defining roles and responsibilities and assigning oversight responsibility Designating a compliance officer and compliance committee Conducting effective training and education General training on ethical standards and human subject research Training on federal cost principles and grant administration regulations and policies Developing effective lines of communication

33 Using Internal Audit to Reinforce Compliance Across the Institution Internal Audit departments can assist institutions in building a culture of compliance related to sponsored research. Particular focus should be given to: Accounting system capabilities and utilization Administrative controls for monitoring cost charging Focus on allowability, allocability, and consistency of costs Cost transfers Payroll distribution/effort reporting Training programs provided to Principal Investigators and research personnel

34 References and Resources

35 References Grant Fraud: A Message from the National Procurement Fraud Task Force National Institutes of Health, Division of Grants Compliance and Oversight Common Compliance Pitfalls and Strategies for Success A Federal Perspective on Compliance National Procurement Fraud Task Force, A Guide to Grant Oversight and Best Practices for Combating Fraud, February

36 Additional Resources Baker Tilly Council on Governmental Relations National Council of University Research Administrators

844-4389 robinmk@auburn.")

37 Thank You! Richard Cordova Executive Director, Internal Audit University of Washington (206) Kevin Robinson Executive Director, Internal Audit Auburn University (334) Kim Ginn Principal Baker Tilly (703)

38 Required disclosure and Circular 230 Prominent Disclosure The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party. Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International Baker Tilly Virchow Krause, LLP.

NSF OIG Audit Update NORTHEAST CONFERENCE ON COLLEGE COST ACCOUNTING

NSF OIG Audit Update 1 NORTHEAST CONFERENCE ON COLLEGE COST ACCOUNTING S e p t e m b e r 2 3, 2 0 1 4 Overview 2 Overview of NSF OIG Office of Audit Overview of Federal financial assistance in the U.S.

NSF OIG Audit Update 1 NORTHEAST CONFERENCE ON COLLEGE COST ACCOUNTING S e p t e m b e r 2 3, 2 0 1 4 Overview 2 Overview of NSF OIG Office of Audit Overview of Federal financial assistance in the U.S.

Uniform Guidance Sponsored Projects Services

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Uniform Guidance Subpart D Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs

3/15/14 Draft Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs Prepared for the Council of Chief State School Officers Federal

3/15/14 Draft Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs Prepared for the Council of Chief State School Officers Federal

Navigating the New Uniform Grant Guidance. Jack Reagan, Audit Partner Grant Thornton LLP. Grant Thornton. All rights reserved.

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance)

") Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

New Uniform Consolidated Grants Guidance

New Uniform Consolidated Grants Guidance From Accountability for Compliance to Accountability for Results The Honorable Jim Taylor and Robert Shea December 2014 Agenda Background Former circulars Consolidated

New Uniform Consolidated Grants Guidance From Accountability for Compliance to Accountability for Results The Honorable Jim Taylor and Robert Shea December 2014 Agenda Background Former circulars Consolidated

OMB Uniform Guidance ( UG ) Briefing. ASRSP & OSR Brown Bag Tuesday, January 27 th

Briefing. ASRSP & OSR Brown Bag Tuesday, January 27 th") OMB Uniform Guidance ( UG ) Briefing ASRSP & OSR Brown Bag Tuesday, January 27 th Background The UG is the single biggest regulatory change in the last fifty years in research administration Interesting

OMB Uniform Guidance ( UG ) Briefing ASRSP & OSR Brown Bag Tuesday, January 27 th Background The UG is the single biggest regulatory change in the last fifty years in research administration Interesting

A S S O C I A T I O N O F C O L L E G E A N D U N I V E R S I T Y A U D I T O R S A N N U A L C O N F E R E N C E S

National Science Foundation Office of Inspector General Audit Overview 1 ASSOCIATION OF COLLEGE AND UNIVERSITY AUDITORS ANNUAL CONFERENCE September 2012 Outline 2 Federal Offices of Inspector General National

National Science Foundation Office of Inspector General Audit Overview 1 ASSOCIATION OF COLLEGE AND UNIVERSITY AUDITORS ANNUAL CONFERENCE September 2012 Outline 2 Federal Offices of Inspector General National

Single Audit Entrance Conference Uniform Guidance Refresher

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

DISA INSTRUCTION March 2006 Last Certified: 11 April 2008 ORGANIZATION. Inspector General of the Defense Information Systems Agency

DEFENSE INFORMATION SYSTEMS AGENCY P. O. Box 4502 ARLINGTON, VIRGINIA 22204-4502 DISA INSTRUCTION 100-45-1 17 March 2006 Last Certified: 11 April 2008 ORGANIZATION Inspector General of the Defense Information

DEFENSE INFORMATION SYSTEMS AGENCY P. O. Box 4502 ARLINGTON, VIRGINIA 22204-4502 DISA INSTRUCTION 100-45-1 17 March 2006 Last Certified: 11 April 2008 ORGANIZATION Inspector General of the Defense Information

GUIDANCE. Funds for Title I, Part B of the Rehabilitation Act of 1973, as amended. Made Available Under

GUIDANCE Funds for Title I, Part B of the Rehabilitation Act of 1973, as amended Made Available Under The American Recovery and Reinvestment Act of 2009 U.S. Department of Education Office of Special Education

GUIDANCE Funds for Title I, Part B of the Rehabilitation Act of 1973, as amended Made Available Under The American Recovery and Reinvestment Act of 2009 U.S. Department of Education Office of Special Education

Office of Inspector General Annual Work Plan

BACKGROUND The Office of Inspector General provides the Division of Emergency Management a central point for coordination of and responsibility for activities that promote accountability, integrity, and

BACKGROUND The Office of Inspector General provides the Division of Emergency Management a central point for coordination of and responsibility for activities that promote accountability, integrity, and

Overview of the New EDGAR (formerly the Uniform Grants Guidance)

") Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

The Uniform Guidance (2 CFR, Part 200)

") WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

Uniform Guidance Subpart D Administrative Requirements. Why This Session Is Needed. Lesson Overview & Module Objectives

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

Jason Galloway, Associate Controller HSC Contract and Grant Accounting

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida

Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida") Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

Report No. DODIG Department of Defense AUGUST 26, 2013

Report No. DODIG-2013-124 Inspector General Department of Defense AUGUST 26, 2013 Report on Quality Control Review of the Grant Thornton, LLP, FY 2011 Single Audit of the Henry M. Jackson Foundation for

Report No. DODIG-2013-124 Inspector General Department of Defense AUGUST 26, 2013 Report on Quality Control Review of the Grant Thornton, LLP, FY 2011 Single Audit of the Henry M. Jackson Foundation for

Department of Homeland Security Office of Inspector General

Department of Homeland Security Office of Inspector General Independent Review of the U.S. Immigration and Customs Enforcement's Reporting of FY 2009 Drug Control Obligations OIG-10-46 January 2010 Office

Department of Homeland Security Office of Inspector General Independent Review of the U.S. Immigration and Customs Enforcement's Reporting of FY 2009 Drug Control Obligations OIG-10-46 January 2010 Office

Federal Grant Guidance Compliance

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

Something for Everyone: Adjusting to the OMB s Super Circular May 25, :30 10:10 am 2 CPE

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

UNIFORM GUIDANCE IMPLEMENTATION

UNIFORM GUIDANCE IMPLEMENTATION Presented by Sara Judd, OSR Consultant October 2014 Uniform Guidance Implementation what we know and what we re guessing Ready, Set, Go 2014 Fred Hutchinson Cancer Research

UNIFORM GUIDANCE IMPLEMENTATION Presented by Sara Judd, OSR Consultant October 2014 Uniform Guidance Implementation what we know and what we re guessing Ready, Set, Go 2014 Fred Hutchinson Cancer Research

Financial Grants Management. Session Outline. Grants Management Roles 4/19/10

Financial Grants Management Presented by: Donna Teague Grant Accounting Supervisor El Paso County Auditor s Office Small Counties Large Counties Grants Management Records Session Outline New Application

Financial Grants Management Presented by: Donna Teague Grant Accounting Supervisor El Paso County Auditor s Office Small Counties Large Counties Grants Management Records Session Outline New Application

Seminar on Financial Management. VOCA s National Conference

Seminar on Financial Management VOCA s National Conference Financial Management Systems In summary, a Financial Management System must be able to: Record and report on the -- Receipt; Obligation; and Expenditure

Seminar on Financial Management VOCA s National Conference Financial Management Systems In summary, a Financial Management System must be able to: Record and report on the -- Receipt; Obligation; and Expenditure

Texas Association of County Auditors

Presentation to Texas Association of County Auditors New Uniform Grant Guidance and Update on 2014 OMB Circular A-133 Compliance Supplement by www.padgett-cpa.com Presenters Joel Perez, Jr., Partner Leader

Presentation to Texas Association of County Auditors New Uniform Grant Guidance and Update on 2014 OMB Circular A-133 Compliance Supplement by www.padgett-cpa.com Presenters Joel Perez, Jr., Partner Leader

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. AUSPAN Martha Taylor

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Local Nonprofit Agency Risk Assessments

Local Nonprofit Agency s Howard Gesbeck Jr., CPA, JD, Wipfli LLP PO Box 8700 Madison WI 53708 888.876.4992 gfpinfo@wipfli.com Presenter: Howard Gesbeck Jr., CPA, JD Howard Gesbeck is a partner with Wipfli

Local Nonprofit Agency s Howard Gesbeck Jr., CPA, JD, Wipfli LLP PO Box 8700 Madison WI 53708 888.876.4992 gfpinfo@wipfli.com Presenter: Howard Gesbeck Jr., CPA, JD Howard Gesbeck is a partner with Wipfli

Office of Inspector General Audit Tips for FEMA Public Assistance Grant Recipients and Subrecipients

Office of Inspector General Audit Tips for FEMA Public Assistance Grant Recipients and Subrecipients Tonda L. Hadley, Director Central Regional Office-South Office of Emergency Management Oversight Texas

Office of Inspector General Audit Tips for FEMA Public Assistance Grant Recipients and Subrecipients Tonda L. Hadley, Director Central Regional Office-South Office of Emergency Management Oversight Texas

Presenter. Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance

The New OMB Uniform Guidance") Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance Presenter Richard Cunningham Quality Assurance & Technical Specialist Center

Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance Presenter Richard Cunningham Quality Assurance & Technical Specialist Center

Delayed Federal Grant Closeout: Issues and Impact

Delayed Federal Grant Closeout: Issues and Impact Natalie Keegan Analyst in American Federalism and Emergency Management Policy September 12, 2014 Congressional Research Service 7-5700 www.crs.gov R43726

Delayed Federal Grant Closeout: Issues and Impact Natalie Keegan Analyst in American Federalism and Emergency Management Policy September 12, 2014 Congressional Research Service 7-5700 www.crs.gov R43726

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Renewable Energy Grants and Incentives for Higher Education Institutions. Baker Tilly refers to Baker Tilly Virchow Krause, LLP,

Renewable Energy Grants and Incentives for Higher Education Institutions Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. 2011

Renewable Energy Grants and Incentives for Higher Education Institutions Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. 2011

Using Internal Audits for Successful Grant Administration

Using Internal Audits for Successful Grant Administration Welcome & Speakers Session Objectives Explain key rules and requirements for complying with CDBG-DR Internal Audit requirements Discuss role of

Using Internal Audits for Successful Grant Administration Welcome & Speakers Session Objectives Explain key rules and requirements for complying with CDBG-DR Internal Audit requirements Discuss role of

Roadmap to the Uniform Grant Guidance for School Districts

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN

TO 2 CFR 200 (UNIFORM ADMIN") Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

2009 American Recovery and Reinvestment Act (ARRA)

") 2009 American Recovery and Reinvestment Act (ARRA) Understanding Compliance and Reporting Requirements Associated with ARRA Stimulus Funds November 19, 2009 2009 American Recovery & Reinvestment Act Today

2009 American Recovery and Reinvestment Act (ARRA) Understanding Compliance and Reporting Requirements Associated with ARRA Stimulus Funds November 19, 2009 2009 American Recovery & Reinvestment Act Today

3 rd Annual Symposium for Research Administrators

3 rd Annual Symposium for Research Administrators Cost Transfer Policy Martha Martin, CRA, Grants Administration, School of Information and Library Science Sarah Van Heusen, MHA, Director of Research Administration,

3 rd Annual Symposium for Research Administrators Cost Transfer Policy Martha Martin, CRA, Grants Administration, School of Information and Library Science Sarah Van Heusen, MHA, Director of Research Administration,

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards Thursday, March 20, 2014, 12:30 p.m. 2:00 p.m. ET Venable LLP, Washington, DC Moderator: Jeffrey S. Tenenbaum,

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards Thursday, March 20, 2014, 12:30 p.m. 2:00 p.m. ET Venable LLP, Washington, DC Moderator: Jeffrey S. Tenenbaum,

Are You Ready for This? The New Uniform Guidance 2 CFR 200

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

ADMINISTRATION OF FEDERAL GRANT FUNDS

ADMINISTRATION OF FEDERAL GRANT FUNDS The Board accepts federal funds, which are available, provided that there is a specific need for them and that the required matching funds are available. The Board

ADMINISTRATION OF FEDERAL GRANT FUNDS The Board accepts federal funds, which are available, provided that there is a specific need for them and that the required matching funds are available. The Board

2010 Mauldin & Jenkins Single Audits for for Auditees

2010 Mauldin & Jenkins Single Audits for Auditees SINGLE AUDITS FOR AUDITEES Mauldin & Jenkins July 22, 2010 Macon August 3, 2010 - Atlanta PRESENTER Hope Pendergrass Manager Macon Office hpendergrass@mjcpa.com

2010 Mauldin & Jenkins Single Audits for Auditees SINGLE AUDITS FOR AUDITEES Mauldin & Jenkins July 22, 2010 Macon August 3, 2010 - Atlanta PRESENTER Hope Pendergrass Manager Macon Office hpendergrass@mjcpa.com

City of Fernley GRANTS MANAGEMENT POLICIES AND PROCEDURES

1 of 12 I. PURPOSE The purpose of this policy is to set forth an overall framework for guiding the City s use and management of grant resources. II ` GENERAL POLICY Grant revenues are an important part

1 of 12 I. PURPOSE The purpose of this policy is to set forth an overall framework for guiding the City s use and management of grant resources. II ` GENERAL POLICY Grant revenues are an important part

The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

Hello. National Grants Management Association Monthly Training November 16, Eric J. Russell, CIA, CGAP, CGMS, MPA Crowe Horwath LLP

Hello. National Grants Management Association Monthly Training November 16, 2016 Eric J. Russell, CIA, CGAP, CGMS, MPA Crowe Horwath LLP 2016 Crowe 2016 Crowe Horwath Horwath LLP LLP Agenda Third Party

Hello. National Grants Management Association Monthly Training November 16, 2016 Eric J. Russell, CIA, CGAP, CGMS, MPA Crowe Horwath LLP 2016 Crowe 2016 Crowe Horwath Horwath LLP LLP Agenda Third Party

University of Pittsburgh

I. Guideline Background University sponsors are increasingly relying on institutions for the development of adequate compliance programs for the financial administration of grants and contracts. An adequate

I. Guideline Background University sponsors are increasingly relying on institutions for the development of adequate compliance programs for the financial administration of grants and contracts. An adequate

MONTGOMERY COUNTY INTERMEDIATE UNIT #23

No. 626 MONTGOMERY COUNTY INTERMEDIATE UNIT #23 SECTION: TITLE: FINANCES FEDERAL FISCAL COMPLIANCE ADOPTED: June 22, 2016 REVISED: 626. FEDERAL FISCAL COMPLIANCE 1. Authority Part 200 2. Delegation of

No. 626 MONTGOMERY COUNTY INTERMEDIATE UNIT #23 SECTION: TITLE: FINANCES FEDERAL FISCAL COMPLIANCE ADOPTED: June 22, 2016 REVISED: 626. FEDERAL FISCAL COMPLIANCE 1. Authority Part 200 2. Delegation of

Steve Relyea Executive Vice Chancellor and Chief Financial Officer. Audit Report 18-67, Sponsored Programs Post Award, Office of the Chancellor

Date: May 4, 2018 To: From: Subject: Steve Relyea Executive Vice Chancellor and Chief Financial Officer Larry Mandel Vice Chancellor and Chief Audit Officer Audit Report 18-67, Sponsored Programs Post

Date: May 4, 2018 To: From: Subject: Steve Relyea Executive Vice Chancellor and Chief Financial Officer Larry Mandel Vice Chancellor and Chief Audit Officer Audit Report 18-67, Sponsored Programs Post

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT INTRODUCTION BACKGROUND On December 26, 2013, the Office of

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT INTRODUCTION BACKGROUND On December 26, 2013, the Office of

Playing by the Rules

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Office of Community Planning and Development Community Development Block Grant Program Playing by the Rules A Handbook for CDBG Subrecipients on Administrative

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Office of Community Planning and Development Community Development Block Grant Program Playing by the Rules A Handbook for CDBG Subrecipients on Administrative

Nonprofit Single Audit and Major Program Determination Worksheet

40 HUD 8/14 : Nonprofit Single Audit and Major Program Determination Worksheet Entity: Completed by: Statement of Financial Position Date: Date: IMPORTANT INFORMATION ABOUT CHANGES TO THE SINGLE AUDIT

40 HUD 8/14 : Nonprofit Single Audit and Major Program Determination Worksheet Entity: Completed by: Statement of Financial Position Date: Date: IMPORTANT INFORMATION ABOUT CHANGES TO THE SINGLE AUDIT

Federal Rules for Sponsored Programs. Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Lessons Learned from Prior Reports on Disaster-related Procurement and Contracting

Lessons Learned from Prior Reports on Disaster-related Procurement and Contracting December 5, 2017 OIG-18-29 DHS OIG HIGHLIGHTS Lessons Learned from Prior Reports on Disaster-related Procurement and Contracting

Lessons Learned from Prior Reports on Disaster-related Procurement and Contracting December 5, 2017 OIG-18-29 DHS OIG HIGHLIGHTS Lessons Learned from Prior Reports on Disaster-related Procurement and Contracting

Uniform Guidance - Lessons Learned And To Be Learned

DAY MAY 23, 2017 3:35-4:50PM Uniform Guidance - Lessons Learned And To Be Learned MODERATOR Jerry E. Durham Assistant Director for Research and Compliance, Tennessee Comptroller of the Treasury SPEAKERS

DAY MAY 23, 2017 3:35-4:50PM Uniform Guidance - Lessons Learned And To Be Learned MODERATOR Jerry E. Durham Assistant Director for Research and Compliance, Tennessee Comptroller of the Treasury SPEAKERS

Uniform Guidance and Compliance

Uniform Guidance and Compliance Office of Research Author: Mariel Diaz Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Uniform Guidance Award Management

Uniform Guidance and Compliance Office of Research Author: Mariel Diaz Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Uniform Guidance Award Management

MANAGER S TOOLKIT FOR A SUCCESSFUL FINANCIAL STATEMENT AUDIT

MANAGER S TOOLKIT FOR A SUCCESSFUL FINANCIAL STATEMENT AUDIT Ms. Lorin Venable, DoD OIG ASMC PDI Workshop #79 June 2, 2017 1 Agenda OIG Audit History Complexity of DoD FY 2016 Audit Opinions Status of

MANAGER S TOOLKIT FOR A SUCCESSFUL FINANCIAL STATEMENT AUDIT Ms. Lorin Venable, DoD OIG ASMC PDI Workshop #79 June 2, 2017 1 Agenda OIG Audit History Complexity of DoD FY 2016 Audit Opinions Status of

Uniform Guidance Update. Ruth Boardman, Associate Director Office of Grants and Contracts March 2015

Uniform Guidance Update Ruth Boardman, Associate Director Office of Grants and Contracts March 2015 Objectives Latest Updates Internal Controls Procurement Status of Policies and Procedures Research Terms

Uniform Guidance Update Ruth Boardman, Associate Director Office of Grants and Contracts March 2015 Objectives Latest Updates Internal Controls Procurement Status of Policies and Procedures Research Terms

Single Audit Report. State of North Carolina. For the Year Ended June 30, Office of the State Auditor Beth A. Wood, CPA State Auditor

Single Audit Report For the Year Ended June 30, 2011 Office of the State Auditor Beth A. Wood, CPA State Auditor State of North Carolina STATE OF NORTH CAROLINA SINGLE AUDIT REPORT 2 0 1 1 OFFICE OF THE

Single Audit Report For the Year Ended June 30, 2011 Office of the State Auditor Beth A. Wood, CPA State Auditor State of North Carolina STATE OF NORTH CAROLINA SINGLE AUDIT REPORT 2 0 1 1 OFFICE OF THE

REQUEST FOR PROPOSAL (RFP) PROFESSIONAL AUDITING SERVICES

PROFESSIONAL AUDITING SERVICES") REQUEST FOR PROPOSAL (RFP) PROFESSIONAL AUDITING SERVICES Kathy Cortner Chief Financial Officer Mojave Water Agency 13846 Conference Center Drive Apple Valley, CA 92307 Issue Date: January 24, 2018 Deadline

REQUEST FOR PROPOSAL (RFP) PROFESSIONAL AUDITING SERVICES Kathy Cortner Chief Financial Officer Mojave Water Agency 13846 Conference Center Drive Apple Valley, CA 92307 Issue Date: January 24, 2018 Deadline

4.12 Effort Certification

4.112 Grants and Cooperative Agreements 4.1121 The Public Health Service ("PHS") and the National Science Foundation ("NSF") have regulations promoting objectivity in research by requiring that a university

4.112 Grants and Cooperative Agreements 4.1121 The Public Health Service ("PHS") and the National Science Foundation ("NSF") have regulations promoting objectivity in research by requiring that a university

APPENDIX VII OTHER AUDIT ADVISORIES

APPENDIX VII OTHER AUDIT ADVISORIES I. Effect of Changes to Generally Applicable Compliance Requirements in the 2015 Supplement In the 2015 Supplement, OMB has removed several of the compliance requirements

APPENDIX VII OTHER AUDIT ADVISORIES I. Effect of Changes to Generally Applicable Compliance Requirements in the 2015 Supplement In the 2015 Supplement, OMB has removed several of the compliance requirements

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

CHAPTER Senate Bill No. 400

CHAPTER 98-91 Senate Bill No. 400 An act relating to state financial accountability; creating the Florida Single Audit Act; providing intent and findings; creating s. 216.3491, F.S.; providing purposes

CHAPTER 98-91 Senate Bill No. 400 An act relating to state financial accountability; creating the Florida Single Audit Act; providing intent and findings; creating s. 216.3491, F.S.; providing purposes

Insurance & Federal Claims Services (IFCS)

") Insurance & Federal Claims Services (IFCS) Why? s (IFCS) practice is a group of professionals dedicated to assisting governmental, nonprofit and corporate entities to expedite financial recovery and mitigation

Insurance & Federal Claims Services (IFCS) Why? s (IFCS) practice is a group of professionals dedicated to assisting governmental, nonprofit and corporate entities to expedite financial recovery and mitigation

Federal Grants-in-Aid Administration: A Primer

Federal Grants-in-Aid Administration: A Primer Natalie Keegan Analyst in American Federalism and Emergency Management Policy October 3, 2012 CRS Report for Congress Prepared for Members and Committees

Federal Grants-in-Aid Administration: A Primer Natalie Keegan Analyst in American Federalism and Emergency Management Policy October 3, 2012 CRS Report for Congress Prepared for Members and Committees

Index as: DEPARTMENTAL AUDITS AND INSPECTIONS

Ref: CALEA Standards 53.1.1; 53.2.1 DEPARTMENTAL GENERAL ORDER N-12 Index as: New Order Audits Inspections Office of Inspector General (OIG) DEPARTMENTAL AUDITS AND INSPECTIONS The purpose of this order

Ref: CALEA Standards 53.1.1; 53.2.1 DEPARTMENTAL GENERAL ORDER N-12 Index as: New Order Audits Inspections Office of Inspector General (OIG) DEPARTMENTAL AUDITS AND INSPECTIONS The purpose of this order

REQUEST FOR PROPOSALS AUDIT SERVICES

REQUEST FOR PROPOSALS AUDIT SERVICES Issue Date: January 19, 2017 Proposals Due: February 28, 2017 Issued by: City of Patterson 1 Plaza, P.O. Box 667 Patterson, CA 95363 REQUEST FOR PROPOSALS AUDITING

REQUEST FOR PROPOSALS AUDIT SERVICES Issue Date: January 19, 2017 Proposals Due: February 28, 2017 Issued by: City of Patterson 1 Plaza, P.O. Box 667 Patterson, CA 95363 REQUEST FOR PROPOSALS AUDITING

Uniform Guidance. Overview and Implementation Plan. November 21, 2014

Uniform Guidance Overview and Implementation Plan November 21, 2014 Uniform Guidance. Change is coming! College or Department name here 1 Overarching goal of the reform is to: streamline the rules and

Uniform Guidance Overview and Implementation Plan November 21, 2014 Uniform Guidance. Change is coming! College or Department name here 1 Overarching goal of the reform is to: streamline the rules and

December 26, 2014 NEW ADDITIONAL December 26, 2014 beginning December 26, /31/15, 6/30/16 Contents Reference Origin Appendix

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

Chapter 10 Housing Rehabilitation Revolving Loan Fund

Revolving Loan Fund Recipient Checklist It is absolutely essential that the city/county grant recipient, the nonprofit sub recipient and the perspective assisted private property owner not incur any ACTIVITY

Revolving Loan Fund Recipient Checklist It is absolutely essential that the city/county grant recipient, the nonprofit sub recipient and the perspective assisted private property owner not incur any ACTIVITY

Combating Medicaid Fraud & Abuse NCSL New England Fiscal Leaders Meeting February 22, 2013

Combating Medicaid Fraud & Abuse NCSL New England Fiscal Leaders Meeting February 22, 2013 Kavita Choudhry State Health Care Spending Project Pew Charitable Trusts Pressure on state and local budgets Source:

Combating Medicaid Fraud & Abuse NCSL New England Fiscal Leaders Meeting February 22, 2013 Kavita Choudhry State Health Care Spending Project Pew Charitable Trusts Pressure on state and local budgets Source:

Uniform Guidance and Internal Controls: A Case Study

Uniform Guidance and Internal Controls: A Case Study Rick Moyer, Stanford University Kim Ginn, Baker Tilly Ashley Deihr, Baker Tilly Expected outcomes from this session: Translate university expectations

Uniform Guidance and Internal Controls: A Case Study Rick Moyer, Stanford University Kim Ginn, Baker Tilly Ashley Deihr, Baker Tilly Expected outcomes from this session: Translate university expectations

The OmniCircular - 2 CFR 200

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS. National Historical Publications and Records Commission

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

Graduate Grantsmanship Certificate Series Jo Ann Smith, Ph.D., CRA Joshua Roney, M.A.

Graduate Grantsmanship Certificate Series Jo Ann Smith, Ph.D., CRA Joshua Roney, M.A. Review / Questions? Workshop #4 Content Previous Homework Create a draft research budget and narrative Workshop #5:

Graduate Grantsmanship Certificate Series Jo Ann Smith, Ph.D., CRA Joshua Roney, M.A. Review / Questions? Workshop #4 Content Previous Homework Create a draft research budget and narrative Workshop #5:

FINANCE-315 7/1/2017 SUBRECIPIENT COMMITMENT FORM

SUBRECIPIENT COMMITMENT FORM All subrecipients should complete this form when submitting a proposal to UACES. It provides a checklist of documents and certifications required by sponsors, as well as an

SUBRECIPIENT COMMITMENT FORM All subrecipients should complete this form when submitting a proposal to UACES. It provides a checklist of documents and certifications required by sponsors, as well as an

INVESTIGATIONS. Division of Investigations and Law Enforcement

INVESTIGATIONS Division of Investigations and Law Enforcement ORGANIZATIONAL CHART INVESTIGATIONS INTEGRITY The Role of Ethics in Criminal Justice Agencies The success of any Criminal Justice Agency is

INVESTIGATIONS Division of Investigations and Law Enforcement ORGANIZATIONAL CHART INVESTIGATIONS INTEGRITY The Role of Ethics in Criminal Justice Agencies The success of any Criminal Justice Agency is

Navy s Contract/Vendor Pay Process Was Not Auditable

Inspector General U.S. Department of Defense Report No. DODIG-2015-142 JULY 1, 2015 Navy s Contract/Vendor Pay Process Was Not Auditable INTEGRITY EFFICIENCY ACCOUNTABILITY EXCELLENCE INTEGRITY EFFICIENCY

Inspector General U.S. Department of Defense Report No. DODIG-2015-142 JULY 1, 2015 Navy s Contract/Vendor Pay Process Was Not Auditable INTEGRITY EFFICIENCY ACCOUNTABILITY EXCELLENCE INTEGRITY EFFICIENCY

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Overview of Procurement September

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Overview of Procurement September

Management Emphasis and Organizational Culture; Compliance; and Process and Workforce Development.

---------------------------------------------------------------- The United States Navy on the World Wide Web A service of the Navy Office of Information, Washington DC send feedback/questions to comments@chinfo.navy.mil

---------------------------------------------------------------- The United States Navy on the World Wide Web A service of the Navy Office of Information, Washington DC send feedback/questions to comments@chinfo.navy.mil

Ohio Enterprise Grants & Common Grants Compliance Issues

Ohio Enterprise Grants & Common Grants Compliance Issues Stacie Massey Ohio Office of Budget and Management June 12, 2018 The Growing Grants Business The State of Ohio manages $28 billion in federal grant

Ohio Enterprise Grants & Common Grants Compliance Issues Stacie Massey Ohio Office of Budget and Management June 12, 2018 The Growing Grants Business The State of Ohio manages $28 billion in federal grant

INTRODUCTION TO RESEARCH ADMINISTRATION. Office of Grants and Contracts Administration August 2015

INTRODUCTION TO RESEARCH ADMINISTRATION Office of Grants and Contracts Administration August 2015 THE RESEARCH VESSEL SIKULIAQ FUNDED BY THE NATIONAL SCIENCE FOUNDATION Objectives To understand the UAF

INTRODUCTION TO RESEARCH ADMINISTRATION Office of Grants and Contracts Administration August 2015 THE RESEARCH VESSEL SIKULIAQ FUNDED BY THE NATIONAL SCIENCE FOUNDATION Objectives To understand the UAF

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. AU SPAN Martha Taylor Larry Hankins

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AU SPAN 6 23 2014 Martha Taylor Larry Hankins Grants Reform February 2011 President directed OMB to reduce

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AU SPAN 6 23 2014 Martha Taylor Larry Hankins Grants Reform February 2011 President directed OMB to reduce

BOARD OF COOPERATIVE EDUCATIONAL SERVICES SOLE SUPERVISORY DISTRICT FRANKLIN-ESSEX-HAMILTON COUNTIES MEDICAID COMPLIANCE PROGRAM CODE OF CONDUCT

BOARD OF COOPERATIVE EDUCATIONAL SERVICES SOLE SUPERVISORY DISTRICT FRANKLIN-ESSEX-HAMILTON COUNTIES MEDICAID COMPLIANCE PROGRAM CODE OF CONDUCT Adopted April 22, 2010 BOARD OF COOPERATIVE EDUCATIONAL

BOARD OF COOPERATIVE EDUCATIONAL SERVICES SOLE SUPERVISORY DISTRICT FRANKLIN-ESSEX-HAMILTON COUNTIES MEDICAID COMPLIANCE PROGRAM CODE OF CONDUCT Adopted April 22, 2010 BOARD OF COOPERATIVE EDUCATIONAL

Uniform Grants Guidance. Colorado Charter School Institute Cassie Walgren, Controller

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

EXHIBIT A SPECIAL PROVISIONS

EXHIBIT A SPECIAL PROVISIONS The following provisions supplement or modify the provisions of Items 1 through 9 of the Integrated Standard Contract, as provided herein: A-1. ENGAGEMENT, TERM AND CONTRACT

EXHIBIT A SPECIAL PROVISIONS The following provisions supplement or modify the provisions of Items 1 through 9 of the Integrated Standard Contract, as provided herein: A-1. ENGAGEMENT, TERM AND CONTRACT

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY. Office of Contracts and Grants December, 2014

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

Federal Grants and Financial Assistance 2017 Training Catalog

1 P a g e Who are we? Meet Colleague Consulting Colleague Consulting LLC is a 19-year-old small business specializing in training, human resource development, and organizational development services for

1 P a g e Who are we? Meet Colleague Consulting Colleague Consulting LLC is a 19-year-old small business specializing in training, human resource development, and organizational development services for

Request for Proposal PROFESSIONAL AUDIT SERVICES. Luzerne-Wyoming Counties Mental Health/Mental Retardation Program

Request for Proposal PROFESSIONAL AUDIT SERVICES Luzerne-Wyoming Counties Mental Health/Mental Retardation Program For the Fiscal Year July 1, 2004 June 30, 2005 DUE DATE: Noon on Friday, April 22, 2005

Request for Proposal PROFESSIONAL AUDIT SERVICES Luzerne-Wyoming Counties Mental Health/Mental Retardation Program For the Fiscal Year July 1, 2004 June 30, 2005 DUE DATE: Noon on Friday, April 22, 2005

Office of Inspector General Department of Defense FY 2012 FY 2017 Strategic Plan

Office of Inspector General Department of Defense FY 2012 FY 2017 Strategic Plan Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated

Office of Inspector General Department of Defense FY 2012 FY 2017 Strategic Plan Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated

NOVA SOUTHEASTERN UNIVERSITY OFFICE OF SPONSORED PROGRAMS POLICIES AND PROCEDURES

PAGE 1 OF 14 PURPOSE: The increasing involvement of academic researchers and educators with industry and private entrepreneurial ventures has raised the potential for conflict of interest. Such real or

PAGE 1 OF 14 PURPOSE: The increasing involvement of academic researchers and educators with industry and private entrepreneurial ventures has raised the potential for conflict of interest. Such real or

APPENDIX N FEDERAL AUDIT CLAUSES

APPENDIX N FEDERAL AUDIT CLAUSES APPENDIX N AUDIT CLAUSE TO BE USED IN AGREEMENTS WITH SUBRECIPIENTS RECEIVING FEDERAL AWARDS FROM THE COMMONWEALTH SINGLE AUDIT REPORT REQUIREMENTS. The [NAME OF SUBRECIPIENT]

APPENDIX N FEDERAL AUDIT CLAUSES APPENDIX N AUDIT CLAUSE TO BE USED IN AGREEMENTS WITH SUBRECIPIENTS RECEIVING FEDERAL AWARDS FROM THE COMMONWEALTH SINGLE AUDIT REPORT REQUIREMENTS. The [NAME OF SUBRECIPIENT]

Any observations not included in this report were discussed with your staff at the informal exit conference and may be subject to follow-up.

Larry Mandel Vice Chancellor and Chief Audit Officer Office of Audit and Advisory Services 401 Golden Shore, 4th Floor Long Beach, CA 90802-4210 562-951-4430 562-951-4955 (Fax) lmandel@calstate.edu September

Larry Mandel Vice Chancellor and Chief Audit Officer Office of Audit and Advisory Services 401 Golden Shore, 4th Floor Long Beach, CA 90802-4210 562-951-4430 562-951-4955 (Fax) lmandel@calstate.edu September

FINANCIAL AUDITING SERVICES. July 10, :00 PM

DIRECTORS JOHN D. S. ALLEN, PRESIDENT SERGIO CALDERON, VICE PRESIDENT WILLARD H.MURRAY, JR., SECRETARY ALBERT ROBLES, TREASURER ROB KATHERMAN, DIRECTOR ROBB WHITAKER, P.E., GENERAL MANAGER REQUEST FOR

DIRECTORS JOHN D. S. ALLEN, PRESIDENT SERGIO CALDERON, VICE PRESIDENT WILLARD H.MURRAY, JR., SECRETARY ALBERT ROBLES, TREASURER ROB KATHERMAN, DIRECTOR ROBB WHITAKER, P.E., GENERAL MANAGER REQUEST FOR

WHAT LAWS APPLY TO FEDERAL GRANTS: A HISTORICAL PERSPECTIVE

WHAT LAWS APPLY TO FEDERAL GRANTS: A HISTORICAL PERSPECTIVE LEIGH M. MANASEVIT, ESQ. LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM SPRING FORUM 2013 1 1960s: Congress began recognizing

WHAT LAWS APPLY TO FEDERAL GRANTS: A HISTORICAL PERSPECTIVE LEIGH M. MANASEVIT, ESQ. LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM SPRING FORUM 2013 1 1960s: Congress began recognizing

Clinical Compliance Program

Clinical Compliance Program The University at Buffalo School of Dental Medicine, Daniel Squire Diagnostic and Treatment Center (UBSDM) has always been and remains committed to conducting its business in

Clinical Compliance Program The University at Buffalo School of Dental Medicine, Daniel Squire Diagnostic and Treatment Center (UBSDM) has always been and remains committed to conducting its business in

COMPLIANCE WITH THIS PUBLICATION IS MANDATORY

BY ORDER OF THE SECRETARY OF THE AIR FORCE AIR FORCE INSTRUCTION 65-302 23 AUGUST 2018 Financial Management EXTERNAL AUDIT SERVICES COMPLIANCE WITH THIS PUBLICATION IS MANDATORY ACCESSIBILITY: Publications

BY ORDER OF THE SECRETARY OF THE AIR FORCE AIR FORCE INSTRUCTION 65-302 23 AUGUST 2018 Financial Management EXTERNAL AUDIT SERVICES COMPLIANCE WITH THIS PUBLICATION IS MANDATORY ACCESSIBILITY: Publications

Compliance Program Updated August 2017

Compliance Program Updated August 2017 Table of Contents Section I. Purpose of the Compliance Program... 3 Section II. Elements of an Effective Compliance Program... 4 A. Written Policies and Procedures...

Compliance Program Updated August 2017 Table of Contents Section I. Purpose of the Compliance Program... 3 Section II. Elements of an Effective Compliance Program... 4 A. Written Policies and Procedures...

NOT-FOR-PROFIT INSIDER

NOT-FOR-PROFIT INSIDER VOLUME 9 :: ISSUE 3 In This Issue: Streamlining OMB Guidance For Federal Funding Of Nonprofit Organizations New 1023-EZ Makes Applying For 501(C)(3) Tax-Exempt Status Easier Identifying

NOT-FOR-PROFIT INSIDER VOLUME 9 :: ISSUE 3 In This Issue: Streamlining OMB Guidance For Federal Funding Of Nonprofit Organizations New 1023-EZ Makes Applying For 501(C)(3) Tax-Exempt Status Easier Identifying

Request for Proposal for: Financial Audit Services

Eastern Sierra Transit Authority (ESTA) Request for Proposal for: Financial Audit Services Due Date: March 21, 2018 at 4:00 pm to the attention of: Karie Bentley Administrative Analyst Eastern Sierra Transit

Eastern Sierra Transit Authority (ESTA) Request for Proposal for: Financial Audit Services Due Date: March 21, 2018 at 4:00 pm to the attention of: Karie Bentley Administrative Analyst Eastern Sierra Transit