REPORT 2014/100 INTERNAL AUDIT DIVISION

|

|

|

- Jesse Gaines

- 6 years ago

- Views:

Transcription

1 INTERNAL AUDIT DIVISION REPORT 2014/100 Audit of the administration of entitlements and benefits of uniformed personnel by the Departments of Peacekeeping Operations, Field Support, Management and selected field missions Overall results relating to the effective administration of entitlements and benefits of uniformed personnel by the Departments of Peacekeeping Operations, Field Support, Management and selected field missions were initially assessed as partially satisfactory. Implementation of two important recommendations remains in progress FINAL OVERALL RATING: PARTIALLY SATISFACTORY 30 September 2014 Assignment No. AP2013/615/01

2 CONTENTS Page I. BACKGROUND 1 II. OBJECTIVE AND SCOPE 1-2 III. AUDIT RESULTS 2-6 A. Regulatory framework 3-6 IV. ACKNOWLEDGEMENT 7 ANNEX I APPENDIX I APPENDIX II APPENDIX III APPENDIX IV APPENDIX V Status of audit recommendations Management response - DM Management response - MONUSCO Management response - UNAMID Management response - UNIFIL Management response - UNOCI

3 AUDIT REPORT Audit of the administration of entitlements and benefits of uniformed personnel by the Departments of Peacekeeping Operations, Field Support, Management, and selected field missions I. BACKGROUND 1. The Office of Internal Oversight Services (OIOS) conducted an audit of the administration of entitlements and benefits of uniformed personnel by: the Departments of Peacekeeping Operations (DPKO), Field Support (DFS), Management (DM) at headquarters; and selected field missions. 2. In accordance with its mandate, OIOS provides assurance and advice on the adequacy and effectiveness of the United Nations internal control system, the primary objectives of which are to ensure (a) efficient and effective operations; (b) accurate financial and operational reporting; (c) safeguarding of assets; and (d) compliance with mandates, regulations and rules. 3. In fiscal year 2013/14, the United Nations had approximately 93,500 uniformed personnel (1,800 military observers, advisors and liaison officers, 79,000 military personnel, 5,500 individual police officers, 6,900 formed police unit personnel and 300 corrections officers) and paid entitlements and benefits totaling $759 million, as shown in Table 1 below. Entitlement/Benefit Table 1: Entitlements and benefits paid in fiscal year 2013/14 Military observers, advisors and liaison officers Military contingent personnel Individual police officers Formed police units Corrections officers Mission subsistence allowance $89,974,662 $108,389,608 $270,638,940 $ - $10,449,172 $479,452,382 Travel on emplacement, rotation and repatriation 7,997, ,538,974 24,233,420 12,344, , ,586,322 Daily allowance - 44,816,212-3,859,220-48,675,432 Recreational leave allowance - 23,515,591-2,124,877-25,640,468 Death and disability compensation 305,300 4,569, , ,151-6,131,452 Clothing allowance 554,870-1,926, ,480,970 Total $98,832,570 $332,829,386 $297,390,460 $18,993,749 $10,920,861 $758,967, The administration of the entitlements of uniformed personnel was governed by policies established by the General Assembly, memoranda of understanding between the United Nations and troop-/police-contributing countries, as well as policies, standard operating procedures and guidelines promulgated by DPKO, DFS and DM. 5. Comments provided by DPKO, DFS, DM and field missions are incorporated in italics. Total II. OBJECTIVE AND SCOPE 6. The audit of was conducted to assess the adequacy and effectiveness of DPKO, DFS, DM and selected field missions governance, risk management and control processes in providing reasonable 1

4 assurance regarding the effective administration of entitlements and benefits of uniformed personnel by DPKO, DFS, DM and selected field missions. 7. This audit was included in the OIOS 2013 risk-based work plan due to the financial risks related to the administration of entitlements and benefits of uniformed personnel. 8. The key control tested for the audit was regulatory framework. For the purpose of this audit, OIOS defined this key control as one that provides reasonable assurance that policies and procedures: (a) exist to guide the administration of entitlements and benefits for uniformed personnel; (b) are implemented consistently; and (c) ensure reliability and integrity of financial and operational information. 9. The key control was assessed for the control objectives shown in Table OIOS conducted this audit from February to April 2013 at Headquarters, and in January and February 2014 at five field missions: the United Nations Organization Stabilization Mission in the Democratic Republic of the Congo (MONUSCO); the African Union-United Nations Hybrid Operation in Darfur (UNAMID); the United Nations Interim Force in Lebanon (UNIFIL); the United Nations Mission in Liberia (UNMIL); and the United Nations Operation in Côte d'ivoire (UNOCI). The audit covered the period from 1 July 2010 to 30 June 2013 in respect of the following payments made directly to uniformed personnel in field missions: (a) mission subsistence allowance (MSA); (b) travel on emplacement, rotation and repatriation to uniformed personnel; (c) daily allowance; and (d) recreational leave allowance. The audit did not cover approximately $151.5 million related air charter services and for travel of military contingents on emplacement, rotation and repatriation. This was because two on-going audits of vendor payments and air operations covering this expenditure were currently in progress. 11. OIOS conducted an activity-level risk assessment to identify and assess specific risk exposures, and to confirm the relevance of the selected key controls in mitigating associated risks. Through interviews, analytical reviews and tests of controls, OIOS assessed the existence and adequacy of internal controls and conducted necessary tests to determine their effectiveness. III. AUDIT RESULTS 12. The DPKO, DFS, DM and selected field missions governance, risk management and control processes examined were initially assessed as partially satisfactory 1 in providing reasonable assurance regarding the effective administration of entitlements and benefits of uniformed personnel by DPKO, DFS, DM and selected field missions. OIOS made six recommendations to address the issues identified. The United Nations had adequate policies, standard operating procedures and guidelines promulgated by the General Assembly, DPKO, DFS, DM and respective field missions for the administration of entitlements. However, DM did not periodically review and revise subsistence allowance rates as required. Also, while for the most part, field missions complied with established policies and procedures, some missions needed to strengthen controls over: (a) payment of MSA; (b) travel on emplacement, rotation and repatriation; and (c) payment of daily and recreational leave allowances. 13. The initial overall rating was based on the assessment of the key control presented in Table 2 below. The final overall rating is partially satisfactory as implementation of two important recommendations remains in progress. 1 A rating of partially satisfactory means that important (but not critical or pervasive) deficiencies exist in governance, risk management or control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 2

5 Table 2: Assessment of key control Business objective Effective administration of entitlements and benefits of uniformed personnel by DPKO, DFS, DM, and selected field missions Key control Regulatory framework Efficient and effective operations Partially satisfactory FINAL OVERALL RATING: PARTIALLY SATISFACTORY Control objectives Accurate financial and operational reporting Partially satisfactory Safeguarding of assets Partially satisfactory Compliance with mandates, regulations and rules Partially satisfactory Regulatory framework Mission subsistence allowance rates were not regularly reviewed and updated 14. According to the Administrative Instruction on MSA, rates were to be established, periodically reviewed and published for each mission by the Office of Human Resources Management (OHRM). The systematic review and updating of MSA rates was not conducted as DM no longer had a dedicated budget for this activity, as payment of MSA to civilian staff was discontinued after the 2009 human resources management reform. The website of OHRM showed that rates for 24 of 27 missions, including the 5 selected missions covered by this audit, were last reviewed and published on or before The rates for three missions including the United Nations Multidimensional Integrated Stabilization Mission in Mali, the United Nations Assistance Mission for Iraq (Baghdad), and the United Nations Disengagement Observer Force (Syria) were reviewed and published in 2012 and There was thus a risk that most MSA rates may not reflect the current cost of accommodation, food and miscellaneous expenses. (1) OHRM should take steps to ensure that mission subsistence allowance rates are periodically reviewed, revised and published accordingly. DM accepted recommendation 1 and stated that OHRM would use the special operations living allowance rates published by the International Civil Service Commission to update its MSA rates and, for locations without special operations living allowance rates, OHRM would establish MSA rates. Recommendation 1 remains open pending receipt of evidence that OHRM has taken adequate action to ensure that subsistence rates/living allowance rates are periodically reviewed and published. The administration of mission subsistence allowances in two missions needed improvement 15. The Administrative Instruction on MSA required that eligible uniformed personnel on temporary assignment be paid MSA to cover living expenses. According to Amendment 1 of the Instruction, personnel residing in mission-provided accommodation that had been assessed by DFS as meeting certain criteria should be paid a reduced MSA rate. 3

6 16. MSA payments processed by MONUSCO, UNAMID and UNMIL were paid at established rates to eligible uniformed personnel on temporary assignments and appropriate deductions were made from payments to staff residing in mission-provided accommodations. However: In UNIFIL, 20 staff officers were paid 50 per cent of their MSA which was $172,000 during the period covered by the audit. This was done without approval from DFS on the classification of the accommodations as substandard, although UNIFIL had requested DFS approval to classify accommodations as substandard; and In UNOCI, MSA payments were not always supported by the relevant documentation. For example, a review of 44 payments totaling $226,466 showed that: (a) documents for four MSA payments totaling $9,196 were not available; and (b) attendance sheets supporting two other payments totaling $12,525 were neither signed nor approved by the responsible military official. This was due to the lack of adequate and effective procedures implemented by the Mission to recalculate and verify that the correct amounts were paid and properly supported. (2) UNIFIL should obtain approval of the Department of Field Support on the classification of facilities used by staff officers and use such classification when calculating mission subsistence allowance payments to officers residing in mission-provided accommodation. UNIFIL accepted recommendation 2 and issued an Administrative Instruction to ensure no overpayment of MSA was being made. Based on the action taken by UNIFIL, recommendation 2 has been closed. (3) UNOCI should establish and implement additional procedures to ensure that the calculation and payment of mission subsistence allowance are properly supported. UNOCI accepted recommendation 3 and stated that the finance checklist for MSA now included a reconciliation of the numbers of personnel at the beginning and end of each month and UNOCI would issue guidelines on the checks to be performed and information to be obtained from military and police finance officers. Recommendation 3 remains open pending receipt of a copy of the guidelines issued by UNOCI on the additional checks being done on the calculation and payment of MSA. Administration of entitlements for travel on emplacement, rotation and repatriation needed to improve for one mission 17. The United Nations was required to pay official travel expenses upon emplacement, rotation and repatriation of uniformed personnel excluding members of military contingents that routinely travelled on United Nations charter flights. Administrative instructions on official travels and the directive of DM provided for: (a) standard of accommodation for official air travel; (b) official travel to be authorized and signed by designated officials; (c) daily substance and terminal expenses be paid based on actual expenses incurred; (d) repatriation travel claims for subsistence allowance and terminal expense be processed and a payable account set up prior to the repatriation of the personnel; (e) a minimum of three price quotations be obtained for airfare; (f) official travel be authorized; and (g) the processing of travel requests to commence at least 16 days before the date of travel. 18. Transactions by UNAMID, UNIFIL, UNMIL and UNOCI for travel on emplacement, rotation and repatriation were administered and paid in compliance with the required policies and procedures. However, MONUSCO did not require uniformed personnel to submit their travel claims for daily subsistence allowances and terminal expenses that were paid prior to travel on repatriation, and expected 4

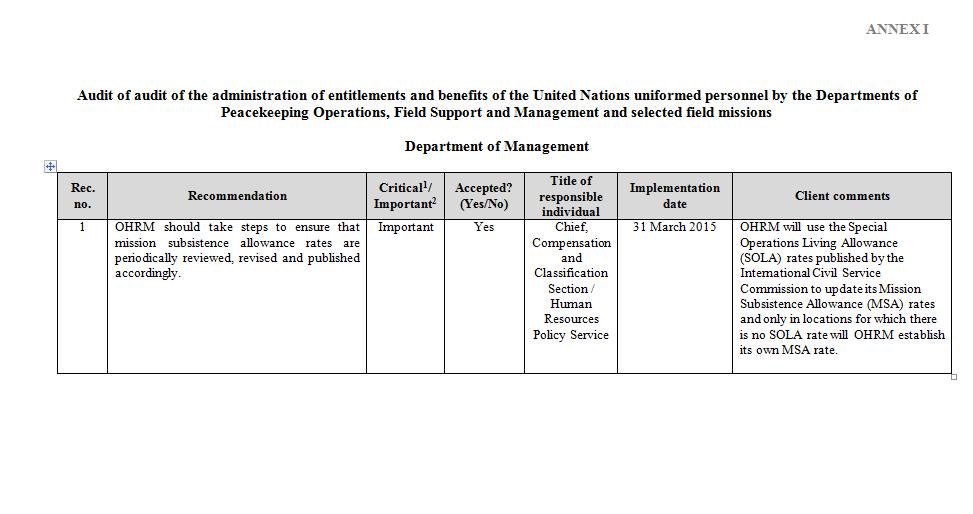

7 uniformed personnel to mail their claims back upon arrival in their respective countries. During 2012/13, MONUSCO authorized 1,287 repatriations totaling $3.1 million. In 10 out of 11 reviewed travels costing $66,749, personnel did not submit their claims to MONUSCO. MONUSCO confirmed that the procedure established to obtain travel claims was not working. (4) MONUSCO, in conjunction with the Regional Service Centre in Entebbe, should process repatriation travel claims for uniformed personnel prior to their departure in compliance with required procedures. MONUSCO accepted recommendation 4 and stated that procedures had been established in which the Regional Service Centre in Entebbe was paying repatriation travel claims for uniformed personnel prior to their end of mission assignment. Based on the action taken by MONUSCO, recommendation 4 has been closed. Three missions needed to enhance controls over payment of daily allowances 19. A daily allowance was payable to military contingents and Formed Police Unit personnel at the rate of $1.28 per day through their respective paymasters. Daily allowance was not payable in advance to staff officers and to troop strengths above the authorized level. The mission Finance Section was required to obtain from contingent paymasters disbursement pay sheets containing the signatures of recipients of daily allowances and verify them to ensure that recipients were in the mission during the period. For those who were not present in the Mission, the undisbursed amounts were to be remitted back to the mission Finance Section. 20. UNIFIL and UNMIL administered and paid daily allowances in compliance with policies and procedures. However: In MONUSCO, contingent paymasters for 25 batches of daily allowances did not return the original signed distribution sheets back to the Finance Section. This was due to the lack of adequate procedures to ensure the Mission s paymasters provided evidence of their disbursement of daily allowances to beneficiaries; In UNAMID, the contingent paymaster did not provide five distribution sheets for 1,309 personnel amounting to $50,624 to the Finance Section. UNAMID attributed this to high turnover of staff and inadequate hand-over procedures for documents; and In UNOCI, there were no signed distribution sheets of recipients or leave records to verify the presence of uniformed personnel in the Mission during the period for which they were paid. Also, daily allowances were signed for by the same individual on behalf of a number of beneficiaries. For example, signed distribution sheets attached to seven daily allowance payments totaling $177,549 were made between 31 July 2012 and 16 April 2013 were signed by the same individual. (5) MONUSCO, UNAMID and UNOCI should develop and implement procedures to ensure that all contingent paymasters return original signed daily allowance distribution sheets to the Finance Section for review and filing, including a requirement that each individual signs for amounts received. MONUSCO, UNAMID and UNOCI accepted recommendation 5. MONUSCO had developed procedures in coordination with its military offices requiring contingent paymasters to provide 5

8 signed distribution lists to the Finance Section for review, verification and filing. UNAMID were preparing personnel analysis sheets and ensuring the signed Formed Police Units attendance sheets were submitted to the Mission s Monitoring Unit. UNOCI had established procedures to ensure payments are not made to the paymaster without the signature sheet confirming that beneficiaries received the previous month s amounts. Based on the actions taken by MONUSCO, UNAMID and UNOCI, recommendation 5 has been closed. Payment of recreational leave allowances were not administered in compliance with established policies in two missions 21. Military contingent personnel were entitled to a recreational leave allowance of $10.50 per day for up to 15 days of leave during each six-month period. Verification of claims for recreational leave allowance was processed by the mission Military Personnel Office and the Financial Section. In case of repatriation before completion of the six-month period, no recreation leave allowance was payable and prorating the six-month period was not allowed. The mission Finance Section was required to verify contingent paymasters disbursement pay sheets containing the signatures of recipients of daily allowances and verify them to ensure whether the recipient had been in the mission during the period. For those who were not present in the Mission, the undisbursed amounts were to be remitted back to the mission Finance Section. 22. Recreational allowance payments for MONUSCO, UNIFIL and UNMIL were properly administered and paid. However: In UNAMID, the contingent paymasters did not provide recreational leave allowance distribution sheets to the Finance Section for 13 batches reviewed. UNAMID attributed this to high staff turnover and inadequate hand-over procedures for documents; and In UNOCI, there were no signed distribution sheets of recipients or leave records to verify the presence of personnel in the Mission during the period for which they were paid. Recreational leave allowances were collected and signed for by the same individual on behalf of a number of beneficiaries. For example, three daily recreational leave payments totaling $354,375 paid from October to November 2012 were signed by the same individual. This was due to the lack of adequate procedures over the payment of daily allowances by contingents paymasters. (6) UNAMID and UNOCI should implement procedures to ensure that contingent paymasters return their signed recreational leave allowance distribution sheets to the Finance Section for review and filing. UNAMID and UNOCI accepted recommendation 6. UNAMID were preparing personnel analysis sheets and ensuring the signed Formed Police Units attendance sheets were submitted to the Mission s Monitoring Unit. UNOCI had established new procedures to ensure payments are not made to the paymaster without the signature sheet confirming that beneficiaries received the previous month s amounts. Based on the actions taken by UNAMID and UNOCI, recommendation 6 has been closed. 6

9 IV. ACKNOWLEDGEMENT 23. OIOS wishes to express its appreciation to the Management and staff of DM, DFS, DPKO, MONUSCO, UNAMID, UNIFIL, and UNOCI for the assistance and cooperation extended to the auditors during this assignment. (Signed) David Kanja Assistant Secretary-General for Internal Oversight Services 7

10 APPENDIX I STATUS OF AUDIT RECOMMENDATIONS Audit of the administration of entitlements and benefits of uniformed personnel by the Departments of Peacekeeping Operations, Field Support, Management and selected field missions Department of Management Recom. no. Recommendation 1 OHRM should take steps to ensure that mission subsistence allowance rates are periodically reviewed, revised and published accordingly. Critical 2 / C/ Important 3 O 4 Actions needed to close recommendation Important O Receipt of evidence that OHRM has taken adequate action to ensure that subsistence rates/living allowance rates are periodically reviewed and published. Implementation date 5 31 March Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 3 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 4 C = closed, O = open 5 Date provided by DM in response to the recommendation. 1

11 APPENDIX II STATUS OF AUDIT RECOMMENDATIONS Audit of the administration of entitlements and benefits of uniformed personnel by the Departments of Peacekeeping Operations, Field Support, Management and selected field missions United Nations Organization Stabilization Mission in the Democratic Republic of the Congo Recom. no. Recommendation 4 MONUSCO, in conjunction with the Regional Service Centre in Entebbe, should process repatriation travel claims for uniformed personnel prior to their departure in compliance with required procedures. 5 MONUSCO should develop and implement procedures to ensure that all contingent paymasters return original signed daily allowance distribution sheets to the Finance Section for review and filing, including a requirement that each individual signs for amounts received. Critical 6 / C/ Implementation Important 7 O 8 Actions needed to close recommendation date 9 Important C Action taken Implemented Important C Action taken Implemented 6 Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 7 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 8 C = closed, O = open 9 Date provided by MONUSCO in response to recommendations. 2

12 APPENDIX III STATUS OF AUDIT RECOMMENDATIONS Audit of the administration of entitlements and benefits of uniformed personnel by the Departments of Peacekeeping Operations, Field Support, Management and selected field missions African Union-United Nations Hybrid Operation in Darfur Recom. Recommendation no. 5 UNAMID should develop and implement procedures to ensure that all contingent paymasters return original signed daily allowance distribution sheets to the Finance Section for review and filing, including a requirement that each individual signs for amounts received. 6 UNAMID should implement procedures to ensure that contingent paymasters return their signed recreational leave allowance distribution sheets to the Finance Section for review and filing. Critical 10 / C/ Implementation Important 11 O 12 Actions needed to close recommendation date 13 Important C Action taken Implemented Important C Action taken Implemented 10 Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 11 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 12 C = closed, O = open 13 Date provided by UNAMID in response to recommendations. 3

13 APPENDIX IV STATUS OF AUDIT RECOMMENDATIONS Audit of the administration of entitlements and benefits of uniformed personnel by the Departments of Peacekeeping Operations, Field Support, Management and selected field missions United Nations Interim Force in Lebanon Recom. Recommendation no. 2 UNIFIL should obtain approval of the Department of Field Support on the classification of facilities used by staff officers and use such classification when calculating mission subsistence allowance payments to officers residing in Mission-provided accommodation. Critical 14 / C/ Implementation Important 15 O 16 Actions needed to close recommendation date 17 Important C Action taken Implemented 14 Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 15 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 16 C = closed, O = open 17 Date provided by UNIFIL in response to the recommendation. 4

14 APPENDIX V STATUS OF AUDIT RECOMMENDATIONS Audit of the administration of entitlements and benefits of uniformed personnel by the Departments of Peacekeeping Operations, Field Support, Management and selected field missions United Nations Operation in Côte d'ivoire Recom. Recommendation no. 3 UNOCI should establish and implement additional procedures to ensure that the calculation and payment of mission subsistence allowance are properly supported. 5 UNOCI should develop and implement procedures to ensure that all contingent paymasters return original signed daily allowance distribution sheets to the Finance Section for review and filing, including a requirement that each individual signs for amounts received. 6 UNOCI should implement procedures to ensure that contingent paymasters return their signed recreational leave allowance distribution sheets to the Finance Section for review and filing. Critical 18 / C/ Important 19 O 20 Actions needed to close recommendation Important O Receipt of a copy of the guidelines issued by UNOCI on the additional checks to being done on the calculation and payment of MSA. Implementation date November 2014 Important C Action taken Implemented Important C Action taken Implemented 18 Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 19 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 20 C = closed, O = open 21 Date provided by UNOCI in response to recommendations. 5

15 APPENDIX I Management Response

16

17

18

19 ANNEX II Audit of the administration of entitlements and benefits of the United Nations uniformed personnel by the Departments of Peacekeeping Operations, Field Support and Management and selected field missions United Nations Organization Stabilization Mission in the Democratic Republic of the Congo Rec. Recommendation no. 4 MONUSCO, in conjunction with the Regional Service Centre in Entebbe, should process repatriation travel claims for uniformed personnel prior to their departure in compliance with required procedures. Critical 22 / Important 23 Accepted? (Yes/No) Title of responsible individual Important Yes Chief, RSCE / Chief Finance Officer, MONUSCO Implementation date Client comments Implemented The recommendation has been implemented. MONUSCO coordinated with the Regional Service Centre in Entebbe (RSCE) to streamline Military repatriation travel claims in compliance with the established procedures. The RSCE now pays the travel repatriation claims (terminal expenses) for United Nations uniformed personnel prior to their end of mission assignment. A Personnel Officer has been designated as focal point and tasked to oversee issues related to Military F10 claims. A copy of memorandum reference ODMS/2014/086 dated 15 April 2014 was provided to OIOS under a separate cover. 22 Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 23 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review.

20 ANNEX II Audit of the administration of entitlements and benefits of the United Nations uniformed personnel by the Departments of Peacekeeping Operations, Field Support and Management and selected field missions United Nations Organization Stabilization Mission in the Democratic Republic of the Congo Critical 24 / Title of Accepted? Implementation Important responsible 25 (Yes/No) date Rec. Recommendation no. 5 MONUSCO should develop and implement procedures to ensure that all contingent paymasters return original signed daily allowance distribution sheets to the Finance Section for review and filing, including a requirement that each individual signs for amounts received. individual Important Yes Chief Finance Officer, MONUSCO Implemented Client comments MONUSCO developed procedures in coordination with the Military Contingent s Office in which it was agreed that all contingent paymasters will be responsible for signed daily allowance distribution lists. A copy is now submitted to the Finance Section for review, verification and filing after completion. The original copy is retained at the Military Contingent s Office for audit purpose(s). A copy of the signed distribution list was provided to OIOS under a separate cover. 24 Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 25 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review.

21 ANNEX III Audit of the administration of entitlements and benefits of the United Nations uniformed personnel by the Departments of Peacekeeping Operations, Field Support and Management and selected field missions African Union-United Nations Hybrid Operation in Darfur Rec. no. Recommendation 5 UNAMID should develop and implement procedures to ensure that all contingent paymasters return original signed daily allowance distribution sheets to the Finance Section for review and filing, including a requirement that each individual signs for amounts received. Critical 26 / Important 27 Accepted? (Yes/No) Title of responsible individual Important Yes FPU Coordinator/ Finance Officer - Office of the Chief Military Personnel Officer Implementation date Implemented Client comments Formed Police Units (FPUs) prepare claims based on personnel strength analysis reports. Duly signed attendance sheets are submitted to the Monitoring Unit, which further coordinates with the Finance Section for payment of entitlements and benefits. Since October 2013, the FPU Coordinator has created a mechanism to archive and keep record of these reports for reference purposes and to avoid duplication of work and confusion in the payment system. Copies of the signed allowance sheets were provided to OIOS under a separate cover. The Military component has also developed and implemented procedures to address this recommendation. It is now a standard procedure that paymasters submit the original signed daily allowance sheet to the Finance Office for review and 26 Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 27 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review.

22 ANNEX III Audit of the administration of entitlements and benefits of the United Nations uniformed personnel by the Departments of Peacekeeping Operations, Field Support and Management and selected field missions Rec. no. Recommendation 6 UNAMID should implement procedures to ensure that contingent paymasters return their signed recreational leave allowance distribution sheets to the Finance Section for review and filing. African Union-United Nations Hybrid Operation in Darfur Critical 26 / Title of Accepted? Implementation Important responsible 27 (Yes/No) date individual Important Yes FPU Coordinator/ Finance Officer - Office of the Chief Military Personnel Officer Implemented Client comments filing. The requirement to have each individual signs for amounts received are also strictly adhered to. Without following the established standard procedure, the Finance Office would not issue any cheques. Copies of the signed allowance sheets were provided to OIOS under a separate cover. FPUs personnel are entitled to Recreational Leave Allowance of $10.50 per day for 15 days during each six months period. FPUs prepare claims based on personnel strength analysis reports. Duly signed attendance sheets are submitted to the Monitoring Unit, which further coordinates with the Finance Section for payment of entitlement and benefits. Since October 2013, the FPU Coordinator created a mechanism to archive and keep record of these reports for reference purposes and to avoid duplication of work and confusion in the payment system. A copy of a report of recreational allowance was provided to OIOS under a separate cover. Just as for the procedures on the daily

23 ANNEX III Audit of the administration of entitlements and benefits of the United Nations uniformed personnel by the Departments of Peacekeeping Operations, Field Support and Management and selected field missions Rec. no. Recommendation African Union-United Nations Hybrid Operation in Darfur Critical 26 / Title of Accepted? Implementation Important responsible 27 (Yes/No) date individual Client comments allowance sheet, recreational leave allowance distribution sheets are also submitted to the Finance office for review and filing. This is a prerequisite for the contingent to be paid. The office of the Chief Military Personnel Officer (CMPO) will further ensure that copies of the recreational leave allowances are kept for records. Copies of the signed recreational leave allowance sheets were provided to OIOS under a separate cover.

24 ANNEX IV Audit of the administration of entitlements and benefits of the United Nations uniformed personnel by the Departments of Peacekeeping Operations, Field Support and Management and selected field missions United Nations Interim Force in Lebanon Rec. no. Recommendation 2 UNIFIL should obtain approval of the Department of Field Support on the classification of facilities used by staff officers and use such classification when calculating mission subsistence allowance payments to officers residing in Mission-provided accommodation. Critical 28 / Important 29 Accepted? (Yes/No) Title of responsible individual Implementation date Important Yes N/A Implemented on 4 June 2014 Client comments UNIFIL issued an Administrative Instruction (AI) dated 04 June 2014 providing guidance in compliance with the utilization of accommodation provided for UNIFIL personnel ensuring that no overpayment of mission subsistence allowance is made. The guidance is mainly reflected in paragraphs 3 and 8 of the AI. Supporting documents have been shared with the OIOS Resident Auditors in UNIFIL who confirmed the implementation and closure of the recommendation. 28 Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 29 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review.

25 ANNEX V Audit of the administration of entitlements and benefits of the United Nations uniformed personnel by the Departments of Peacekeeping Operations, Field Support and Management and selected field missions United Nations Operation in Côte d'ivoire Rec. no. Recommendation 3 UNOCI should establish and implement additional procedure to ensure that the calculation and payment of mission subsistence allowance are properly supported. Critical 30 / Important 31 Accepted? (Yes/No) Title of responsible individual Important Yes Chief, Finance and Budget Officer Implementation date Fourth quarter of 2014 Client comments The finance checklist for mission subsistence allowance (MSA) payments now includes a reconciliation of the numbers of new starters and leavers in the month, using E.O.D. (entry on duty) and C.O.B. (close of business) inputs from the Military and Police Finance Officers. A guideline will be issued by the implementation date to outline the required checks and information requirements from Military and Police Finance Officers, including the need to submit all relevant information before the payroll processing deadline. 30 Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 31 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review.

26 ANNEX V Audit of the administration of entitlements and benefits of the United Nations uniformed personnel by the Departments of Peacekeeping Operations, Field Support and Management and selected field missions Rec. no. Recommendation 5 UNOCI should develop and implement procedures to ensure that all contingent paymasters return original signed daily allowance distribution sheets to the Finance Section for review and filing, including a requirement that each individual signs for amounts received. United Nations Operation in Côte d'ivoire Critical 32 / Title of Accepted? Implementation Important responsible 33 (Yes/No) date individual Important Yes Chief, Finance and Budget Officer Implemented Client comments A new procedure is now in place to ensure no new payments are made to the paymaster(s) without a signature sheet confirming that beneficiaries of the previous month s amounts have received payment. These signature sheets are kept on file by the Finance Section. A copy of the signed sheets was provided to OIOS under a separate cover. 6 UNOCI should implement procedures to ensure that contingent paymasters return their signed recreational leave allowance distribution sheets to the Finance Section for review and filing. Important Yes Chief, Finance and Budget Officer Implemented A new procedure is now in place to ensure no new payments are made to the paymaster(s) without a signature sheet confirming that beneficiaries of the previous month s amounts have received payment. These signature sheets are kept on file by the Finance Section. Copies of the signed sheets were provided to OIOS under a separate cover. 32 Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 33 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review.

REPORT 2015/029 INTERNAL AUDIT DIVISION. Audit of personnel entitlements and allowances in the United Nations Disengagement Observer Force

INTERNAL AUDIT DIVISION REPORT 2015/029 Audit of personnel entitlements and allowances in the United Nations Disengagement Observer Force Overall results relating to the effective administration of personnel

INTERNAL AUDIT DIVISION REPORT 2015/029 Audit of personnel entitlements and allowances in the United Nations Disengagement Observer Force Overall results relating to the effective administration of personnel

REPORT 2016/111 INTERNAL AUDIT DIVISION. Audit of contingent-owned equipment in the United Nations Interim Force in Lebanon

INTERNAL AUDIT DIVISION REPORT 2016/111 Audit of contingent-owned equipment in the United Nations Interim Force in Lebanon Overall results relating to the management of contingent-owned equipment were

INTERNAL AUDIT DIVISION REPORT 2016/111 Audit of contingent-owned equipment in the United Nations Interim Force in Lebanon Overall results relating to the management of contingent-owned equipment were

REPORT 2015/005 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/005 Audit of the disarmament, demobilization and reintegration programme in the United Nations Operation in Côte d'ivoire Overall results relating to the disarmament,

INTERNAL AUDIT DIVISION REPORT 2015/005 Audit of the disarmament, demobilization and reintegration programme in the United Nations Operation in Côte d'ivoire Overall results relating to the disarmament,

INTERNAL AUDIT DIVISION REPORT 2018/025

INTERNAL AUDIT DIVISION REPORT 2018/025 Audit of education grant disbursement at the Regional Service Centre in Entebbe, the United Nations Interim Force in Lebanon and the Kuwait Joint Support Office

INTERNAL AUDIT DIVISION REPORT 2018/025 Audit of education grant disbursement at the Regional Service Centre in Entebbe, the United Nations Interim Force in Lebanon and the Kuwait Joint Support Office

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/119. Audit of military observer activities in the United Nations Truce Supervision Organization

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/119 Audit of military observer activities in the United Nations Truce Supervision Organization Overall results relating to the effective management of military

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/119 Audit of military observer activities in the United Nations Truce Supervision Organization Overall results relating to the effective management of military

REPORT 2015/056 INTERNAL AUDIT DIVISION. Audit of the conduct and discipline function in the United Nations Interim Force in Lebanon

INTERNAL AUDIT DIVISION REPORT 2015/056 Audit of the conduct and discipline function in the United Nations Interim Force in Lebanon Overall results relating to the effective management of the conduct and

INTERNAL AUDIT DIVISION REPORT 2015/056 Audit of the conduct and discipline function in the United Nations Interim Force in Lebanon Overall results relating to the effective management of the conduct and

REPORT 2015/046 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/046 Audit of the management of super camp facilities in the African Union- United Nations Hybrid Operation in Darfur Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2015/046 Audit of the management of super camp facilities in the African Union- United Nations Hybrid Operation in Darfur Overall results relating to the effective management

REPORT 2015/189 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/189 Audit of the management of the Central Emergency Response Fund in the Office for the Coordination of Humanitarian Affairs Overall results relating to the effective

INTERNAL AUDIT DIVISION REPORT 2015/189 Audit of the management of the Central Emergency Response Fund in the Office for the Coordination of Humanitarian Affairs Overall results relating to the effective

REPORT 2016/106. Audit of management of implementing partners at the International Trade Centre FINAL OVERALL RATING: PARTIALLY SATISFACTORY

INTERNAL AUDIT DIVISION REPORT 2016/106 Audit of management of implementing partners at the International Trade Centre Overall results relating to management of implementing partners were initially assessed

INTERNAL AUDIT DIVISION REPORT 2016/106 Audit of management of implementing partners at the International Trade Centre Overall results relating to management of implementing partners were initially assessed

INTERNAL AUDIT DIVISION REPORT 2017/118. Audit of demining activities in the United Nations Interim Force in Lebanon

INTERNAL AUDIT DIVISION REPORT 2017/118 Audit of demining activities in the United Nations Interim Force in Lebanon The Mission needed to improve utilization of its demining capacity and monitor performance

INTERNAL AUDIT DIVISION REPORT 2017/118 Audit of demining activities in the United Nations Interim Force in Lebanon The Mission needed to improve utilization of its demining capacity and monitor performance

REPORT 2015/155 INTERNAL AUDIT DIVISION. Audit of the United Nations Military Observer Group in India and Pakistan

INTERNAL AUDIT DIVISION REPORT 2015/155 Audit of the United Nations Military Observer Group in India and Pakistan Overall results relating to the effective management of military observation operations

INTERNAL AUDIT DIVISION REPORT 2015/155 Audit of the United Nations Military Observer Group in India and Pakistan Overall results relating to the effective management of military observation operations

REPORT 2015/187 INTERNAL AUDIT DIVISION. Audit of the operations of the Office for the Coordination of Humanitarian Affairs in Afghanistan

INTERNAL AUDIT DIVISION REPORT 2015/187 Audit of the operations of the Office for the Coordination of Humanitarian Affairs in Afghanistan Overall results relating to effective management of operations

INTERNAL AUDIT DIVISION REPORT 2015/187 Audit of the operations of the Office for the Coordination of Humanitarian Affairs in Afghanistan Overall results relating to effective management of operations

REPORT 2015/042 INTERNAL AUDIT DIVISION. Audit of the child protection programme in the African Union-United Nations Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2015/042 Audit of the child protection programme in the African Union-United Nations Hybrid Operation in Darfur Overall results relating to the effective management of the

INTERNAL AUDIT DIVISION REPORT 2015/042 Audit of the child protection programme in the African Union-United Nations Hybrid Operation in Darfur Overall results relating to the effective management of the

REPORT 2014/002 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2014/002 Audit of the United Nations Secretariat s management of the United Nations assistance to the Khmer Rouge Trials technical cooperation project Overall results relating

INTERNAL AUDIT DIVISION REPORT 2014/002 Audit of the United Nations Secretariat s management of the United Nations assistance to the Khmer Rouge Trials technical cooperation project Overall results relating

INTERNAL AUDIT DIVISION REPORT 2016/154. Audit of facilities management in the United Nations Interim Force in Lebanon

INTERNAL AUDIT DIVISION REPORT 2016/154 Audit of facilities management in the United Nations Interim Force in Lebanon Facilities management needed to be strengthened by conducting required preventive maintenance

INTERNAL AUDIT DIVISION REPORT 2016/154 Audit of facilities management in the United Nations Interim Force in Lebanon Facilities management needed to be strengthened by conducting required preventive maintenance

INTERNAL AUDIT DIVISION REPORT 2018/043. Thematic audit of education grant disbursements at the United Nations Secretariat

INTERNAL AUDIT DIVISION REPORT 2018/043 Thematic audit of education grant disbursements at the United Nations Secretariat While education grants were disbursed to employees who met eligibility requirements

INTERNAL AUDIT DIVISION REPORT 2018/043 Thematic audit of education grant disbursements at the United Nations Secretariat While education grants were disbursed to employees who met eligibility requirements

INTERNAL AUDIT DIVISION REPORT 2017/087. Audit of education grant disbursement at the United Nations Office at Vienna

INTERNAL AUDIT DIVISION REPORT 2017/087 Audit of education grant disbursement at the United Nations Office at Vienna There was a need to strengthen controls in administration of education grant entitlements

INTERNAL AUDIT DIVISION REPORT 2017/087 Audit of education grant disbursement at the United Nations Office at Vienna There was a need to strengthen controls in administration of education grant entitlements

INTERNAL AUDIT DIVISION REPORT 2017/107. Audit of police operations in the United Nations Multidimensional Integrated Stabilization Mission in Mali

INTERNAL AUDIT DIVISION REPORT 2017/107 Audit of police operations in the United Nations Multidimensional Integrated Stabilization Mission in Mali Harmonized efforts between the Mission and the highest

INTERNAL AUDIT DIVISION REPORT 2017/107 Audit of police operations in the United Nations Multidimensional Integrated Stabilization Mission in Mali Harmonized efforts between the Mission and the highest

INTERNAL AUDIT DIVISION REPORT 2017/090. Audit of military patrolling operations in United Nations Interim Force in Lebanon

INTERNAL AUDIT DIVISION REPORT 2017/090 Audit of military patrolling operations in United Nations Interim Force in Lebanon The Mission was successfully conducting day-to-day patrols but needed to strengthen

INTERNAL AUDIT DIVISION REPORT 2017/090 Audit of military patrolling operations in United Nations Interim Force in Lebanon The Mission was successfully conducting day-to-day patrols but needed to strengthen

Statement by Under-Secretary-General for Peacekeeping Operations Hervé Ladsous to the Fourth Committee 28 October 2013

[Introduction] Statement by Under-Secretary-General for Peacekeeping Operations Hervé Ladsous to the Fourth Committee 28 October 2013 Good morning, ladies and gentleman. It is my sincere pleasure to be

[Introduction] Statement by Under-Secretary-General for Peacekeeping Operations Hervé Ladsous to the Fourth Committee 28 October 2013 Good morning, ladies and gentleman. It is my sincere pleasure to be

INTERNAL AUDIT DIVISION REPORT 2017/086. Audit of education grant disbursement at the United Nations Office at Geneva

INTERNAL AUDIT DIVISION REPORT 2017/086 Audit of education grant disbursement at the United Nations Office at Geneva There was a need to strengthen controls in administration of education grant entitlements

INTERNAL AUDIT DIVISION REPORT 2017/086 Audit of education grant disbursement at the United Nations Office at Geneva There was a need to strengthen controls in administration of education grant entitlements

INTERNAL AUDIT DIVISION REPORT 2018/063

INTERNAL AUDIT DIVISION REPORT 2018/063 Audit of the civil affairs programme in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic There was a need to

INTERNAL AUDIT DIVISION REPORT 2018/063 Audit of the civil affairs programme in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic There was a need to

INTERNAL AUDIT DIVISION REPORT 2018/076

INTERNAL AUDIT DIVISION REPORT 2018/076 Audit of the United Nations police operations in the United Nations Organization Stabilization Mission in the Democratic Republic of the Congo Coordinated efforts

INTERNAL AUDIT DIVISION REPORT 2018/076 Audit of the United Nations police operations in the United Nations Organization Stabilization Mission in the Democratic Republic of the Congo Coordinated efforts

REPORT 2016/052 INTERNAL AUDIT DIVISION. Audit of Office for the Coordination of Humanitarian Affairs Syria operations

INTERNAL AUDIT DIVISION REPORT 2016/052 Audit of Office for the Coordination of Humanitarian Affairs Syria operations Overall results relating to the effective management of the Office for the Coordination

INTERNAL AUDIT DIVISION REPORT 2016/052 Audit of Office for the Coordination of Humanitarian Affairs Syria operations Overall results relating to the effective management of the Office for the Coordination

INTERNAL AUDIT DIVISION REPORT 2017/141. Audit of the protection of civilians programme in the African Union-United Nations Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2017/141 Audit of the protection of civilians programme in the African Union-United Nations Hybrid Operation in Darfur UNAMID needed to improve strategic planning and oversight

INTERNAL AUDIT DIVISION REPORT 2017/141 Audit of the protection of civilians programme in the African Union-United Nations Hybrid Operation in Darfur UNAMID needed to improve strategic planning and oversight

INTERNAL AUDIT DIVISION REPORT 2017/109

INTERNAL AUDIT DIVISION REPORT 2017/109 Audit of education grant disbursement at the United Nations Office at Nairobi, the United Nations Environment Programme and the United Nations Human Settlements

INTERNAL AUDIT DIVISION REPORT 2017/109 Audit of education grant disbursement at the United Nations Office at Nairobi, the United Nations Environment Programme and the United Nations Human Settlements

Audit Report Grant Closure Processes Follow-up Review

Audit Report Grant Closure Processes Follow-up Review GF-OIG-16-017 Geneva, Switzerland Table of Contents I. Background... 3 II. Objectives, Scope, Methodology and Rating... 5 1) Objectives... 5 2) Scope&

Audit Report Grant Closure Processes Follow-up Review GF-OIG-16-017 Geneva, Switzerland Table of Contents I. Background... 3 II. Objectives, Scope, Methodology and Rating... 5 1) Objectives... 5 2) Scope&

INTERNAL AUDIT DIVISION REPORT 2018/023

INTERNAL AUDIT DIVISION REPORT 2018/023 Audit of the disarmament, demobilization and reintegration programme in the United Nations Multidimensional Integrated Stabilization Mission in the Central African

INTERNAL AUDIT DIVISION REPORT 2018/023 Audit of the disarmament, demobilization and reintegration programme in the United Nations Multidimensional Integrated Stabilization Mission in the Central African

INTERNAL AUDIT DIVISION REPORT 2016/166. Audit of the United Nations Integrated Peacebuilding Office in Guinea-Bissau

INTERNAL AUDIT DIVISION REPORT 2016/166 Audit of the United Nations Integrated Peacebuilding Office in Guinea-Bissau Efforts were needed to improve the effectiveness of the Office s substantive programmes

INTERNAL AUDIT DIVISION REPORT 2016/166 Audit of the United Nations Integrated Peacebuilding Office in Guinea-Bissau Efforts were needed to improve the effectiveness of the Office s substantive programmes

STUDENT ACTIVITY FUNDS

STUDENT ACTIVITY FUNDS INTRODUCTION: Student activities are defined as school clubs, classes or other related activities which organize to raise money and/or promote a particular program, project or subject

STUDENT ACTIVITY FUNDS INTRODUCTION: Student activities are defined as school clubs, classes or other related activities which organize to raise money and/or promote a particular program, project or subject

Terms of Reference AUDIT OF SOLAR HOME SYSTEMS PROJECT. The assignment is to engage an auditor for the following.

Note: Bank solar home systems projects receiving grant funds from the Global Environment Facility (GEF) are normally required to have their records and accounts audited by an independent entity each fiscal

Note: Bank solar home systems projects receiving grant funds from the Global Environment Facility (GEF) are normally required to have their records and accounts audited by an independent entity each fiscal

Cancer Prevention & Research Institute of Texas

Cancer Prevention & Research Institute of Texas IA # 01-18 Internal Audit Report over Post-Award C O N T E N T S Page Internal Audit Report Transmittal Letter to the Oversight Committee... 1 Background...

Cancer Prevention & Research Institute of Texas IA # 01-18 Internal Audit Report over Post-Award C O N T E N T S Page Internal Audit Report Transmittal Letter to the Oversight Committee... 1 Background...

Accountability for Conduct and Discipline in Field Missions

United Nations Department of Political Affairs Department of Peacekeeping Operations Department of Field Support Ref. 2015.10 Policy Accountability for Conduct and Discipline in Field Missions Approved

United Nations Department of Political Affairs Department of Peacekeeping Operations Department of Field Support Ref. 2015.10 Policy Accountability for Conduct and Discipline in Field Missions Approved

Auburn University. Contracts and Grants Accounting

Auburn University Contracts and Grants Accounting Introduction to Contracts and Grants Accounting Contracts and grants are important to Auburn University. Much of the research that Auburn faculty, staff,

Auburn University Contracts and Grants Accounting Introduction to Contracts and Grants Accounting Contracts and grants are important to Auburn University. Much of the research that Auburn faculty, staff,

Navy s Contract/Vendor Pay Process Was Not Auditable

Inspector General U.S. Department of Defense Report No. DODIG-2015-142 JULY 1, 2015 Navy s Contract/Vendor Pay Process Was Not Auditable INTEGRITY EFFICIENCY ACCOUNTABILITY EXCELLENCE INTEGRITY EFFICIENCY

Inspector General U.S. Department of Defense Report No. DODIG-2015-142 JULY 1, 2015 Navy s Contract/Vendor Pay Process Was Not Auditable INTEGRITY EFFICIENCY ACCOUNTABILITY EXCELLENCE INTEGRITY EFFICIENCY

DOD FINANCIAL MANAGEMENT. Improved Documentation Needed to Support the Air Force s Military Payroll and Meet Audit Readiness Goals

United States Government Accountability Office Report to Congressional Requesters December 2015 DOD FINANCIAL MANAGEMENT Improved Documentation Needed to Support the Air Force s Military Payroll and Meet

United States Government Accountability Office Report to Congressional Requesters December 2015 DOD FINANCIAL MANAGEMENT Improved Documentation Needed to Support the Air Force s Military Payroll and Meet

Work of Internal Auditors

IFAC Board Final Pronouncements March 2012 International Standards on Auditing ISA 610 (Revised), Using the Work of Internal Auditors Conforming Amendments to Other ISAs The International Auditing and

IFAC Board Final Pronouncements March 2012 International Standards on Auditing ISA 610 (Revised), Using the Work of Internal Auditors Conforming Amendments to Other ISAs The International Auditing and

Education grant and special education grant for children with a disability

United Nations ST/AI/2004/2 Secretariat 24 June 2004 Administrative instruction Education grant and special education grant for children with a disability The Under-Secretary-General for Management, pursuant

United Nations ST/AI/2004/2 Secretariat 24 June 2004 Administrative instruction Education grant and special education grant for children with a disability The Under-Secretary-General for Management, pursuant

Legacy General Operating Grant Guidelines for Operators without Service Agreement for Fee Subsidy: Operator Guide

Legacy General Operating Grant Guidelines for Operators without Service Agreement for Fee Subsidy: Operator Guide Children's Services City of Toronto December 21, 2016 Transitional Table of Contents Introduction

Legacy General Operating Grant Guidelines for Operators without Service Agreement for Fee Subsidy: Operator Guide Children's Services City of Toronto December 21, 2016 Transitional Table of Contents Introduction

General Assembly. United Nations A/65/715*

United Nations A/65/715* General Assembly Distr.: General 2 February 2011 Original: English Sixty-fifth session Agenda item 143 Administrative and budgetary aspects of the financing of the United Nations

United Nations A/65/715* General Assembly Distr.: General 2 February 2011 Original: English Sixty-fifth session Agenda item 143 Administrative and budgetary aspects of the financing of the United Nations

CSU COLLEGE REVIEWS. The California State University Office of Audit and Advisory Services. California State Polytechnic University, Pomona

CSU The California State University Office of Audit and Advisory Services COLLEGE REVIEWS California State Polytechnic University, Pomona College of Agriculture Audit Report 15-30 May 20, 2015 EXECUTIVE

CSU The California State University Office of Audit and Advisory Services COLLEGE REVIEWS California State Polytechnic University, Pomona College of Agriculture Audit Report 15-30 May 20, 2015 EXECUTIVE

EVALUATION REPORT INSPECTION AND EVALUATION DIVISION. Programme evaluation of the Standing Police Capacity of the Police Division, DPKO.

INSPECTION AND EVALUATION DIVISION EVALUATION REPORT Programme evaluation of the Standing Police Capacity of the Police Division, DPKO 12 June 2015* (*Reissued 6 July 2015 for technical reasons) Assignment

INSPECTION AND EVALUATION DIVISION EVALUATION REPORT Programme evaluation of the Standing Police Capacity of the Police Division, DPKO 12 June 2015* (*Reissued 6 July 2015 for technical reasons) Assignment

EXHIBIT A SPECIAL PROVISIONS

EXHIBIT A SPECIAL PROVISIONS The following provisions supplement or modify the provisions of Items 1 through 9 of the Integrated Standard Contract, as provided herein: A-1. ENGAGEMENT, TERM AND CONTRACT

EXHIBIT A SPECIAL PROVISIONS The following provisions supplement or modify the provisions of Items 1 through 9 of the Integrated Standard Contract, as provided herein: A-1. ENGAGEMENT, TERM AND CONTRACT

Global Partnership on Output-based Aid. Grant Agreement. GPOBA GRANT NUMBER TF I1rD

GPOBA GRANT NUMBER TF091511-I1rD Global Partnership on Output-based Aid Grant Agreement (Expanding Piped Water Supply to Surabaya's Urban Poor Project) between REPUBLIC OF INDONESIA and INTERNATIONAL BANK

GPOBA GRANT NUMBER TF091511-I1rD Global Partnership on Output-based Aid Grant Agreement (Expanding Piped Water Supply to Surabaya's Urban Poor Project) between REPUBLIC OF INDONESIA and INTERNATIONAL BANK

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS. National Historical Publications and Records Commission

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

Uniform Guidance Sponsored Projects Services

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Department of Health and Mental Hygiene Alcohol and Drug Abuse Administration

Audit Report Department of Health and Mental Hygiene Alcohol and Drug Abuse Administration December 2006 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report

Audit Report Department of Health and Mental Hygiene Alcohol and Drug Abuse Administration December 2006 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report

Regulation on the implementation of the European Economic Area (EEA) Financial Mechanism

Financial Mechanism") the European Economic Area (EEA) Financial Mechanism 2009-2014 adopted by the EEA Financial Mechanism Committee pursuant to Article 8.8 of Protocol 38b to the EEA Agreement on 13 January 2011 and confirmed

the European Economic Area (EEA) Financial Mechanism 2009-2014 adopted by the EEA Financial Mechanism Committee pursuant to Article 8.8 of Protocol 38b to the EEA Agreement on 13 January 2011 and confirmed

NOVA SOUTHEASTERN UNIVERSITY

NOVA SOUTHEASTERN UNIVERSITY DIVISION OF RESPONSIBILITIES FOR RESEARCH AND SPONSORED PROGRAMS Vice President of Research & Technology Transfer: The responsibilities of the Vice President of Research &

NOVA SOUTHEASTERN UNIVERSITY DIVISION OF RESPONSIBILITIES FOR RESEARCH AND SPONSORED PROGRAMS Vice President of Research & Technology Transfer: The responsibilities of the Vice President of Research &

Global Environment Facility Grant Agreement

Public Disclosure Authorized CONFORMED COPY GEF TF GRANT NUMBER TF097126 Public Disclosure Authorized Global Environment Facility Grant Agreement (Financing Energy Efficiency at MSMEs Project) Public Disclosure

Public Disclosure Authorized CONFORMED COPY GEF TF GRANT NUMBER TF097126 Public Disclosure Authorized Global Environment Facility Grant Agreement (Financing Energy Efficiency at MSMEs Project) Public Disclosure

ANNEX III FINANCIAL AND CONTRACTUAL RULES I. RULES APPLICABLE TO BUDGET CATEGORIES BASED ON UNIT CONTRIBUTIONS

ANNEX III FINANCIAL AND CONTRACTUAL RULES I. RULES APPLICABLE TO BUDGET CATEGORIES BASED ON UNIT CONTRIBUTIONS I.1 Conditions for eligibility of unit contributions Where the grant takes the form of a unit

ANNEX III FINANCIAL AND CONTRACTUAL RULES I. RULES APPLICABLE TO BUDGET CATEGORIES BASED ON UNIT CONTRIBUTIONS I.1 Conditions for eligibility of unit contributions Where the grant takes the form of a unit

30. GRANTS AND FUNDING ASSISTANCE POLICY

30. GRANTS AND FUNDING ASSISTANCE POLICY POLICY It is the policy of Scott County to account for, and file all appropriate documentation in relation to, any grants or other funding that the county applies

30. GRANTS AND FUNDING ASSISTANCE POLICY POLICY It is the policy of Scott County to account for, and file all appropriate documentation in relation to, any grants or other funding that the county applies

FINANCIAL AUDITING SERVICES. July 10, :00 PM

DIRECTORS JOHN D. S. ALLEN, PRESIDENT SERGIO CALDERON, VICE PRESIDENT WILLARD H.MURRAY, JR., SECRETARY ALBERT ROBLES, TREASURER ROB KATHERMAN, DIRECTOR ROBB WHITAKER, P.E., GENERAL MANAGER REQUEST FOR

DIRECTORS JOHN D. S. ALLEN, PRESIDENT SERGIO CALDERON, VICE PRESIDENT WILLARD H.MURRAY, JR., SECRETARY ALBERT ROBLES, TREASURER ROB KATHERMAN, DIRECTOR ROBB WHITAKER, P.E., GENERAL MANAGER REQUEST FOR

PERALTA COMMUNITY COLLEGE DISTRICT SINGLE AUDIT REPORT JUNE 30, 2010

PERALTA COMMUNITY COLLEGE DISTRICT SINGLE AUDIT REPORT JUNE 30, 2010 TABLE OF CONTENTS JUNE 30, 2010 Independent Auditors' Report on Internal Control Over Financial Reporting and on Compliance and Other

PERALTA COMMUNITY COLLEGE DISTRICT SINGLE AUDIT REPORT JUNE 30, 2010 TABLE OF CONTENTS JUNE 30, 2010 Independent Auditors' Report on Internal Control Over Financial Reporting and on Compliance and Other

CSU COLLEGE REVIEWS. The California State University Office of Audit and Advisory Services. California State University, Sacramento

CSU The California State University Office of Audit and Advisory Services COLLEGE REVIEWS California State University, Sacramento College of Arts and Letters Audit Report 15-31 May 22, 2015 EXECUTIVE SUMMARY

CSU The California State University Office of Audit and Advisory Services COLLEGE REVIEWS California State University, Sacramento College of Arts and Letters Audit Report 15-31 May 22, 2015 EXECUTIVE SUMMARY

Board Report Agreed Management Actions Status Update

Board Report Agreed Management Actions Status Update For information 33 rd Board Meeting Geneva, Switzerland 31 March 1 April 2015 Purpose: This paper gives a status update on Agreed Management Actions

Board Report Agreed Management Actions Status Update For information 33 rd Board Meeting Geneva, Switzerland 31 March 1 April 2015 Purpose: This paper gives a status update on Agreed Management Actions

EUROPEAN COMMISSION DIRECTORATE-GENERAL JUSTICE

EUROPEAN COMMISSION DIRECTORATE-GENERAL JUSTICE SPECIFIC PROGRAMME "ISEC" (2007-2013) PREVENTION OF AND FIGHT AGAINST CRIME CALL FOR PROPOSALS JUST/2013/ISEC/DRUGS/AG Action grants Targeted call on cross

EUROPEAN COMMISSION DIRECTORATE-GENERAL JUSTICE SPECIFIC PROGRAMME "ISEC" (2007-2013) PREVENTION OF AND FIGHT AGAINST CRIME CALL FOR PROPOSALS JUST/2013/ISEC/DRUGS/AG Action grants Targeted call on cross

The Office of Innovation and Improvement s Oversight and Monitoring of the Charter Schools Program s Planning and Implementation Grants

The Office of Innovation and Improvement s Oversight and Monitoring of the Charter Schools Program s Planning and Implementation Grants FINAL AUDIT REPORT ED-OIG/A02L0002 September 2012 Our mission is

The Office of Innovation and Improvement s Oversight and Monitoring of the Charter Schools Program s Planning and Implementation Grants FINAL AUDIT REPORT ED-OIG/A02L0002 September 2012 Our mission is

Department of Human Resources Department of Housing and Community Development Electric Universal Service Program

Performance Audit Report Department of Human Resources Department of Housing and Community Development Electric Universal Service Program Procedures for the Processing and Disbursement of Benefits Should

Performance Audit Report Department of Human Resources Department of Housing and Community Development Electric Universal Service Program Procedures for the Processing and Disbursement of Benefits Should

Request for Proposal for: Financial Audit Services

Eastern Sierra Transit Authority (ESTA) Request for Proposal for: Financial Audit Services Due Date: March 21, 2018 at 4:00 pm to the attention of: Karie Bentley Administrative Analyst Eastern Sierra Transit

Eastern Sierra Transit Authority (ESTA) Request for Proposal for: Financial Audit Services Due Date: March 21, 2018 at 4:00 pm to the attention of: Karie Bentley Administrative Analyst Eastern Sierra Transit

REQUEST FOR QUOTATION (RFQ)

") REQUEST FOR QUOTATION (RFQ) DATE: 12 March 2014 REFERENCE: RFQ/BAR002/2014 Dear Sir / Madam: UN Women Multi Country Office in the Caribbean is seeking a qualified national or international Auditing Firm

REQUEST FOR QUOTATION (RFQ) DATE: 12 March 2014 REFERENCE: RFQ/BAR002/2014 Dear Sir / Madam: UN Women Multi Country Office in the Caribbean is seeking a qualified national or international Auditing Firm

OFFICIAL DOCUMENTS, Democratic Republic of Congo: IDF Grant for the Private Sector Development and Competitiveness Project IDF Grant No.

Public Disclosure Authorized OFFICIAL DOCUMENTS, Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The World Bank 1818 H Street N.W. (202) 477-1234 INTERNATIONAL BANK

Public Disclosure Authorized OFFICIAL DOCUMENTS, Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The World Bank 1818 H Street N.W. (202) 477-1234 INTERNATIONAL BANK

34 CFR 690 Federal Pell Grant Program

34 CFR 690 Federal Pell Grant Program 77 FR 25893, May 2, 2012 Interim Final Rule The Secretary amends four sections of the Federal Pell Grant Program regulations to make them consistent with recent changes

34 CFR 690 Federal Pell Grant Program 77 FR 25893, May 2, 2012 Interim Final Rule The Secretary amends four sections of the Federal Pell Grant Program regulations to make them consistent with recent changes

AWARDING FIXED OBLIGATION GRANTS TO NON-GOVERNMENTAL ORGANIZATIONS

AWARDING FIXED OBLIGATION GRANTS TO NON-GOVERNMENTAL ORGANIZATIONS An Additional Help Document For ADS Chapter 303 New Reference: 11/08/2010 Responsible Office: M/OAA File Name: 303saj_110810 I. PURPOSE

AWARDING FIXED OBLIGATION GRANTS TO NON-GOVERNMENTAL ORGANIZATIONS An Additional Help Document For ADS Chapter 303 New Reference: 11/08/2010 Responsible Office: M/OAA File Name: 303saj_110810 I. PURPOSE

BYLAWS MARINE CORPS LEAGUE DEPARTMENT OF PENNSYLVANIA

BYLAWS ARTICLE ONE DEPARTMENT CONVENTION SECTION 100 - AUTHORITY - The Supreme legislative and policy making power of the Department of Pennsylvania, shall be vested in a Department Convention composed

BYLAWS ARTICLE ONE DEPARTMENT CONVENTION SECTION 100 - AUTHORITY - The Supreme legislative and policy making power of the Department of Pennsylvania, shall be vested in a Department Convention composed

Controls Over Navy Military Payroll Disbursed in Support of Operations in Southwest Asia at San Diego-Area Disbursing Centers

Report No. D-2010-036 January 22, 2010 Controls Over Navy Military Payroll Disbursed in Support of Operations in Southwest Asia at San Diego-Area Disbursing Centers Additional Copies To obtain additional

Report No. D-2010-036 January 22, 2010 Controls Over Navy Military Payroll Disbursed in Support of Operations in Southwest Asia at San Diego-Area Disbursing Centers Additional Copies To obtain additional

Objectives for Financial Control over Grant Programs

Objectives for Financial Control over Grant Programs I. Cash management of grant funds is monitored for appropriate timing of receipts and disbursements of grant funds. (Cash Management) II. Procedures

Objectives for Financial Control over Grant Programs I. Cash management of grant funds is monitored for appropriate timing of receipts and disbursements of grant funds. (Cash Management) II. Procedures

THE WORLD BANK BANKGROUP. DOCUMENTS 15 ap

Public Disclosure Authorized THE WORLD BANK BANKGROUP DOCUMENTS 15 ap Public Disclosure Authorized Hon. Patrick Anthony Chinamasa Minister of Finance and Economic Development Ministry of Finance and Economic

Public Disclosure Authorized THE WORLD BANK BANKGROUP DOCUMENTS 15 ap Public Disclosure Authorized Hon. Patrick Anthony Chinamasa Minister of Finance and Economic Development Ministry of Finance and Economic

AUDIT UNDP BOSNIA AND HERZEGOVINA GRANTS FROM THE GLOBAL FUND TO FIGHT AIDS, TUBERCULOSIS AND MALARIA. Report No Issue Date: 15 January 2014

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP BOSNIA AND HERZEGOVINA GRANTS FROM THE GLOBAL FUND TO FIGHT AIDS, TUBERCULOSIS AND MALARIA Report No. 1130 Issue Date: 15 January 2014 Table of Contents

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP BOSNIA AND HERZEGOVINA GRANTS FROM THE GLOBAL FUND TO FIGHT AIDS, TUBERCULOSIS AND MALARIA Report No. 1130 Issue Date: 15 January 2014 Table of Contents

FULTON COUNTY, GEORGIA OFFICE OF INTERNAL AUDIT FRESH and HUMAN SERVICES GRANT REVIEW

FULTON COUNTY, GEORGIA OFFICE OF INTERNAL AUDIT FRESH and HUMAN SERVICES GRANT REVIEW June 5, 2015 TABLE OF CONTENTS PAGE Introduction... 1 Background... 1 Objective... 1 Scope... 2 Methodology... 2 Findings

FULTON COUNTY, GEORGIA OFFICE OF INTERNAL AUDIT FRESH and HUMAN SERVICES GRANT REVIEW June 5, 2015 TABLE OF CONTENTS PAGE Introduction... 1 Background... 1 Objective... 1 Scope... 2 Methodology... 2 Findings

Report No. D February 22, Internal Controls over FY 2007 Army Adjusting Journal Vouchers

Report No. D-2008-055 February 22, 2008 Internal Controls over FY 2007 Army Adjusting Journal Vouchers Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection

Report No. D-2008-055 February 22, 2008 Internal Controls over FY 2007 Army Adjusting Journal Vouchers Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection

SECTION D - ONGOING GRANT MANAGEMENT

SECTION D - ONGOING GRANT MANAGEMENT D1 Introduction... 2 Risk Differentiation and Tailoring of LFA Services... 2 Identification of Operational Risks including Fraud Risk... 3 D2 Key Services... 5 D2.1

SECTION D - ONGOING GRANT MANAGEMENT D1 Introduction... 2 Risk Differentiation and Tailoring of LFA Services... 2 Identification of Operational Risks including Fraud Risk... 3 D2 Key Services... 5 D2.1

Incomplete Contract Files for Southwest Asia Task Orders on the Warfighter Field Operations Customer Support Contract

Report No. D-2011-066 June 1, 2011 Incomplete Contract Files for Southwest Asia Task Orders on the Warfighter Field Operations Customer Support Contract Report Documentation Page Form Approved OMB No.

Report No. D-2011-066 June 1, 2011 Incomplete Contract Files for Southwest Asia Task Orders on the Warfighter Field Operations Customer Support Contract Report Documentation Page Form Approved OMB No.

WATERFRONT COMMISSION OF NEW YORK HARBOR

WATERFRONT COMMISSION OF NEW YORK HARBOR An Instrumentality of the States of New York and New Jersey Request for Proposal Group 79037Audit Services Classification Code(s): 84-Financial and Financial Related

WATERFRONT COMMISSION OF NEW YORK HARBOR An Instrumentality of the States of New York and New Jersey Request for Proposal Group 79037Audit Services Classification Code(s): 84-Financial and Financial Related

2. This SA does not apply if the entity does not have an internal audit function. (Ref: Para. A2)