Regulations Governing The Perkins CTE Program KBOR Summer Conference June 11, 2015

|

|

|

- Hannah Heath

- 5 years ago

- Views:

Transcription

1 Regulations Governing The Perkins CTE Program KBOR Summer Conference June 11, 2015 MICHAEL BRUSTEIN, ESQ. BRUSTEIN & MANASEVIT, PLLC

2 AGENDA Comments on Reauthorization and Funding What You Need to Know About the WIOA Implementation Issues Importance of EDGAR New Structure of EDGAR Roadmap of Part 76 The New 2 CFR Part 200 Major Changes in Administrative and Cost Rules Financial Management Allowability Procurement Inventory Monitoring / Audits Reconsideration of Compliance Supplement Internal Controls 2

3 APPENDICES 1. WIOA Implementation Schedule 2. TEGL TEGL DOL NPRM on WIOA 3

4 REAUTHORIZATION 1. VEA of VEA Amendments of VEA Amendments of Perkins Act Perkins II Perkins III Perkins IV

5 PERKINS IV GEPA Section 414 Contingent Extension of Programs 2013, 2014, 2015,

6 WHERE DOES PERKINS STAND IN REAUTHORIZATION PIPELINE? In the Senate #3 In The House #2 6

7 SENATE CONSIDERATION OF ESEA #1 Bipartisan Every Child Achieves Act of 2015 Reduces Federal footprint Common Core Senate Scott (SC) will push on floor for portability 7

8 SENATE PRIORITY #2 Higher Education Act One or Two Bills? Program/Financial Aid 8

9 HOUSE PRIORITY #1 - ESEA President would veto current House bill Student Success Act HR5 Lack of full Republican support 9

10 HOUSE PRIORITY #2 - PERKINS Chairman Kline with industry demands House will align CTE program 10

11 House CTE Hearings Unlikely Before August recess Highly Unlikely to Have Perkins V on President s Desk This Year 11

12 But Remember the Bipartisan Effort on WIOA Last Year 12

13 Perkins V Most Likely Reauthorized in 2016 with a 07/01/2017 Effective Date 13

14 WHAT WILL PERKINS V LOOK LIKE? No major overhaul Not contentious as ESEA/HEA Align with WIOA DOL Role on Perkins Postsecondary?? 14

15 WHAT HAPPENED TO OCTAE BLUEPRINT?? Competitive funding vs formula Consortia funding Private industry match Innovation fund ($200 million) Programs of study 15

16 PERKINS FUNDING Essentially flat for 20 years Elimination of Tech Prep in 2010 Sequester enacted in 2011 FY 13 cuts See Appendix on State Tables CROmnibus 07/01/ /01/2016 Approximate 1% cut due to sequester 16

17 WHO ARE THE CTE FUNDING CHAMPIONS? Obama? Duncan? Any ED Secretaries (Riley / Pierce) CCSSO Chiefs North Carolina / Washington 17

18 WHAT YOU NEED TO KNOW ABOUT THE WIOA 18

19 IMPLEMENTATION ISSUES 19

")

20 Local Application Plan Local program budgets should reflect efforts to improve on those accountability indicators that were substandard Projects funded must be of sufficient size, scope and quality Sub recipient Monitoring Annual Local Report Funds used for CTSO events Time and Effort Reporting Supplement not supplant Policies and Procedures (recommendation) 20

21 LOCAL APPLICATION PLANS Perkins Section specific content elements Local improvement plan (Section 123(b)) For any failure to meet an adjusted level of performance by at least 90% OCTAE will look for connection between any failure to meet a performance indicator and how funds are being spent. 21

22 CAREER AND TECHNICAL STUDENT ORGANIZATIONS OCTAE: Perkins funds may not be used to support the lodging, feeding, conveying, or furnishing transportation to conventions or other forms of social assemblage for CTSOs. Perkins IV, Non-Regulatory Guidance Q&A Version 3.0, Question D.26 (June 2, 2009) RegulatoryGuidanceQAVersion3.0.pdf 22

part of a larger program to serve special populations or nontraditional students All costs for direct support to students follows same")

23 CAREER AND TECHNICAL STUDENT ORGANIZATIONS Perkins funds may be used for lodging, feeding, conveying, or furnishing transportation if the costs are (1) related to a CTSO that is an integral part of the curriculum, and (2) part of a larger program to serve special populations or nontraditional students All costs for direct support to students follows same standard*** 23

24 SUPPLEMENT NOT SUPPLANT Cannot use federal funds to pay for services, staff, programs or materials that would otherwise be paid for with state or local funds. Always ask: What would have happened in the absence of federal funds? 24

25 A-133 Compliance Supplement presumes supplanting when: Used Perkins funds to provide services the recipient is required to make available under another federal, state, or local law; Used Perkins funds to provide services the recipient provided with state or local funds in the year prior; Used Perkins funds to provide services for CTE students that the recipient provides to non CTE students with non Perkins funds. 25

26 Presumption may be rebutted if: The SEA or LEA demonstrates that it would not have provided the services with state or local funds if the federal funds were not available. 26

in question State or local legislative action Budget histories and")

27 To rebut presumption show: Fiscal or programmatic documentation to confirm that in the absence of federal funds, would have eliminated staff/service(s) in question State or local legislative action Budget histories and information 27

28 COMPENSATION FOR PERSONAL SERVICES Covers all amounts paid currently or accrued by the institution for services of employees rendered during the period of performance. Includes salaries, wages, leave, and fringe benefits. New requirements found in 2 CFR

29 POLICY AND PROCEDURES All recipients are required to have certain written policies and procedures under the UGG. Even where written policies and procedures are not required, it is good practice. Written policies and procedures are always evidence of compliance. OCTAE monitoring reports almost always include a recommendation for written policies and procedures if the recipient does not already have them. 29

30 REQUIRED WRITTEN PROCEDURES: Citation Topic 2 CFR (b)(7) Procedures for determining the allowability of costs, including: Factors affecting allowability Cost principles Selected items of cost 2 CFR (b)(6) & 2 CFR Cash management procedures 2 CFR Procedures for procurement transactions, including: Methods for evaluating proposals and selecting recipients Contract administration 2 CFR (c) Conflict of interest policies, including Reporting process Recusal process Standards regarding gratuities 30 2 CFR (b) Travel policy 30

31 NEW STRUCTURE OF EDGAR 31

32 KEY PARTS OF EDGAR Title 34 Part 75 Direct Grant Programs Part 76 State-Administered Programs Part 77 Definitions Part 81 Enforcement Title 2 Part 200 Cost/Administrative/Audit Rules 32

33 EFFECTIVE DATES FOR 2 CFR PART 200 December 26, 2014 Direct Grants from ED July 1, 2015 State Administered Programs (See Appendix) July 1, 2016 Procurement Rules One Year Grace Period Indirect Cost Rates When Due For Renegotiation 33

34 ADOPTION OF 2 CFR PART FEDERAL REGISTER ED Adopts OMB Guidance in 2 CFR Part 200 except for: 1) 2 CFR (a) 2) 2 CFR (a) 34

35 Exception to 2 CFR (a) Authority for granting exceptions to regulations vested in OMB But Department of Education Organization Act 20 U.S.C does not permit Secretary to delegate exceptions to OMB. Secretary will consult within OMB. 35

36 CLARIFICATION TO 2 CFR HIGH RISK STATUS The Secretary retains the authority under and to impose high risk conditions on individual grants and individual grantees at time award is made or after an award is made. 36

37 ROADMAP OF PART 76 STATE-ADMINISTERED PROGRAMS 37

38 PROGRAMS TO WHICH PART 76 APPLIES 76.1 / / Program Statute Authorizes Fund Allocation to States by Formulas 38

39 State allocates funds by formula (Title I, IDEA-B, Perkins) or Competitively (AEFLA, 21 st Century) 39

40 THE GENERAL STATE APPLICATION Meets requirements of Section 441 of GEPA 40

41 LEA LOCAL APPLICATION Meets requirements of Section 442 of GEPA 41

42 ALLOWABLE COSTS The general principles to be used in determining costs applicable to grants is 2 CFR Part 200 Subpart E 42

43 INDIRECT COST RATES Incorporates language from 2 CFR Part FR

44 GENERAL ADMINISTRATIVE RESPONSIBILITIES Incorporates 2 CFR Part 200 Subpart D 44

45 WHEN OBLIGATIONS ARE MADE Note differences on obligation dates Adds new category pre-agreement costs approved by Secretary are obligated on 1 st day of grant performance period. 45

46 REPORTS AND RECORDS References new reporting requirements on financial management in 2 CFR (performance reporting) 46

47 FUNDS UNDER MORE THAN ONE PROGRAM TO ASSIST A SINGLE ACTIVITY Must comply with req. of each program Proper accounting 47

48 THE NEW 2 CFR PART 200 Subpart A Definitions Subpart B General Provisions Subpart C Pre Award Requirements Subpart D Post Award Requirements Subpart E Cost Principles Subpart F Audit Requirements 48

49 THE MAJOR CHANGES IN FEDERAL GRANTS MANAGEMENT 1. Focus on Outcomes 2. Performance Metrics 3. Risk Assessments 4. Financial Management Policies 5. Equipment Use 6. Micro Purchases 7. Corrective Action 8. Family Friendly Policies 9. False Claims Certifications 10. Audit Thresholds 49

50 FINANCIAL MANAGEMENT CONTROLS THE KEY COMPONENT TO FEDERAL GRANTS 50

51 THE MORE ATTENTION PAID TO FINANCIAL MANAGEMENT CONTROLS, FEWER HEADACHES DOWN THE ROAD!!! 51

52 WHY?? All oversight will examine financial management controls: 1) OIG Audit 2) Single Audit 3) Federal Program Monitoring 4) Pass Through Monitoring 52

53 CROSSWALK BETWEEN OLD RULE 80.20(b) AND OMNI CIRCULAR (b) Current Requirements 1. Financial Reporting 2. Accounting Records 3. Internal Control 4. Budget Control 5. Allowable Cost 6. Source Documentation 7. Cash Management 2 CFR (b) 1. Identification of Awards (NEW) 2. Financial Reporting 3. Accounting Records (Source Docs) 4. Internal Control 5. Budget Control 6. Written Cash Management Procedures (NEW) 7. Written Allowability Procedures (NEW) 53

54 1) IDENTIFICATION OF AWARDS (NEW) All federal awards received and expended The name of the federal program Identification # of award CFDA Title and Number Federal Award I.D. # Fiscal Year of Award Federal Agency Pass-Through (If S/A) 54

55 2) FINANCIAL REPORTING New shift to OMB approved performance metrics 55

56 2) FINANCIAL REPORTING (CONT.) Generally requires accurate, current, complete disclosure of financial results of each award NEW: Federal awarding agency can only collect OMB approved data elements, no less than annually, no more than quarterly NEW: Non federal entity must submit performance reports at intervals required by federal agency or pass through. Annual performance reports due 90 days after reporting period; Quarterly performance reports due 30 days after reporting period 56

200.")

57 2) FINANCIAL REPORTING (CONT.) NEW Performance Metrics: 1. Compare actual accomplishments to objectives (quantify to extent possible) 2. Reasons goals were not met if appropriate 3. Additional pertinent information (e.g. analysis and explanation of cost overruns, high unit costs) (b)(2) 57

58 2) FINANCIAL REPORTING (CONT.) 4. Significant developments a. Problems, delays. Adverse conditions that would impair ability to meet objective of the award b. Favorable developments. Finishing sooner or at less cost (d) 58

59 3) ACCOUNTING RECORDS (SOURCE DOCUMENTATION) Combines 80.20(b)(2) and 80.20(b)(6): Source Documentation Must Be Kept On: 1. Federal Awards 2. Authorizations 3. Obligations 4. Unobligated balances 5. Assets 6. Expenditures 7. Income 8. Interest (New) (Eliminated liabilities) 59

60 4) INTERNAL CONTROLS Essentially same as old requirements 80.20(b)(3): Effective control over and accountability for: 1. All funds 2. Property 3. Other assets Must adequately safeguard all assets Use assets solely for authorized purpose 60

61 5) BUDGET CONTROL Same as old rules 80.20(b)(4) Comparison of expenditures with budget amounts for each award 61

62 6) WRITTEN CASH MANAGEMENT PROCEDURES Written procedures to implement the requirements of (payment) 62

63 6) WRITTEN CASH MANAGEMENT PROCEDURES For states, payments are governed by Treasury State CMIA agreements 31 CFR Part 205 No Change For all other non federal entities, payments must minimize time elapsing between draw from G-5 and disbursement (not obligation) 63

64 6) WRITTEN CASH MANAGEMENT PROCEDURES Written procedures must describe whether non-federal entity uses: 1) Advance Payments (preferred) Limited to minimum amounts needed to meet immediate cash needs 2) Reimbursement Pass through must make payment within 30 calendar days after receipt of the billing 3) Working Capital Advance The pass through determines that the nonfederal entity lacks sufficient working capital. Allows advance payment to cover estimated disbursement needs for initial period 64

65 6) WRITTEN CASH MANAGEMENT PROCEDURES (CONT.) NEW:Advances must be maintained in insured accounts NEW: Pass through cannot require separate depository accounts NEW: Accounts must be interest bearing unless: 1. Aggregate federal awards under $120, Account not expected to earn in excess of $500 per year 3. Bank require minimum balance so high, that such account not feasible 65

66 6) WRITTEN CASH MANAGEMENT PROCEDURES (CONT.) NEW: Interest amounts up to $500 may be retained by non federal entity for administrative purposes Currently $100 for State and local Gov ts Currently $250 for IHEs and Non-profits Interest earned must be remitted annually to HHS 66

67 7) WRITTEN ALLOWABILITY PROCEDURES NEW: Written procedures for determining allowability of costs in accordance with Subpart E Cost Principles 67

Procedures can not simply restate the Uniform Guidance Subpart E Should explain the process used throughout the")

68 7) WRITTEN ALLOWABILITY PROCEDURES (CONT.) Procedures can not simply restate the Uniform Guidance Subpart E Should explain the process used throughout the grant development and budget process Training tool and guide for employees 68

69 SUBPART E COST PRINCIPLES 69

70 COST PRINCIPLES: FACTORS AFFECTING ALLOWABILITY OF COSTS All Costs Must Be: 1. Necessary, Reasonable and Allocable 2. Conform with federal law & grant terms 3. Consistent with state and local policies 4. Consistently treated 5. In accordance with GAAP 6. Not included as match 7. Net of applicable credits (moved to ) 8. Adequately documented 70

71 PRIOR WRITTEN APPROVAL NEW: In order to avoid subsequent disallowance: Non-Federal entity may seek prior written approval of cognizant agency (for indirect cost rate) or Federal awarding agency in advance of the incurrence of special or unusual costs 71

72 DIRECT V. INDIRECT COSTS NEW: Salaries of administrative and clerical staff should be treated as indirect unless all of following are met: 1. Such services are integral to the activity 2. Individuals can be specifically identified with the activity 3. Such costs are explicitly included in the budget 4. Costs not also recovered as indirect 72

73 NEW: REQUIRED CERTIFICATIONS NEW: Official authorized to legally bind the non-federal entity must certify on annual and final fiscal reports or vouchers requesting payment: By signing this report, I certify to the best of my knowledge and belief that the report is true, complete and accurate and the expenditures, disbursements and cash receipts are for the purposes and objectives set forth in the terms and conditions of the federal award. I am aware that any false, fictitious, or fraudulent information or the omission of any material fact, may subject me to criminal civil or administrative penalties for fraud, false statements, false claims, or otherwise. 73

74 SELECTED ITEMS OF COST THE OMNI NOW HAS 55 SPECIFIC ITEMS OF COST!

75 SELECTED ITEMS OF COST (CONT.) Conferences (Changed) Prior Rule: Generally allowable Conference is meeting, seminar, workshop, event for the purpose of disseminating technical info beyond the nonfederal entity (?) Allowable conference costs include rental of facilities, speaker fees, meals and refreshments, and transportation, unless restricted by the federal award New: Costs related to identifying, but not providing, locally available dependent-care resources New: But travel allows costs for above and beyond regular dependent care Conference hosts must exercise discretion in ensuring costs are appropriate, necessary and managed in manner than minimizes costs to federal award 75

76 SELECTED ITEMS OF COST (CONT.) Travel Costs (Changed) Prior rule: allowable with certain restrictions Travel costs may be charged on actual, per diem, or mileage basis Travel charges must be reasonable and consistent with entity s written travel reimbursement policies Grantee must retain documentation that participation of individual in conference is necessary for the project New: Dependent care costs above and beyond regular dependent care that directly result from travel to conferences may be allowable (consistent with written policy) 76

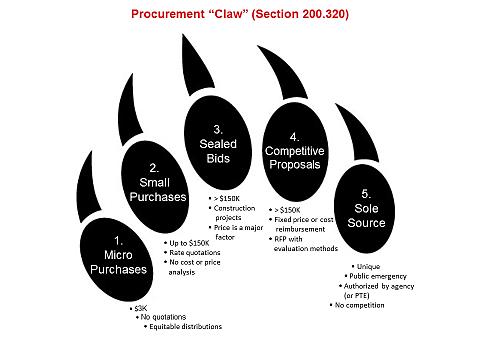

77 OMB CIRCULARS TIME AND EFFORT RULE New Name: Time Distribution Records Standards for Documentation of Personnel Expenses If federal funds are used for salaries, then time distribution records are required. How staff demonstrate allocability Paid in whole or in part with federal funds (i)(1) Used to meet a match/cost share requirement (i)(4) 77

78 COST OBJECTIVES What is a cost objective? (slightly changed) Program, function, activity, award, organizational subdivision, contract, or work unit for which cost data are desired and for which provision is made to accumulate and measure the cost of processes, products, jobs, capital projects, etc. 78

79 TIME AND EFFORT (CURRENT A-87 RULE) Semi-Annual Certifications If an employee works on a single cost objective: After the fact Account for the total activity Signed by employee or supervisor Every six months (at least twice a year) Personnel Activity Report (PAR) If an employee works on multiple cost objectives: After the fact Account for total activity Signed by employee Prepared at least monthly and coincide with one or more pay periods 79

80 STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES NEW: Charges for salaries must be based on records that accurately reflect the work performed 1. Must be supported by a system of internal controls which provides reasonable assurance charges are accurate, allowable and properly allocated 2. Be incorporated into official records 3. Reasonably reflect total activity for which employee is compensated Not to exceed 100% 80

81 STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES (CONT.) 4. Encompass all activities (federal and non-federal) 5. Comply with established accounting polices and practices 6. Support distribution among specific activities or cost objectives 81

82 STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES (CONT.) Budget estimates alone do not qualify as support for charges to Federal awards (i)(1)(viii) NEW: Percentages may be used for distribution of total activities (i)(1)(ix) 82

83 STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES (CONT.) Grantees encouraged to adopt substitute systems if approved by cognizant agency for indirect cost (i)(5) Acceptable to allocate sampled employees supervisors, clerical and support staffs, based on results of sampled employees 83

84 STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES (CONT.) NEW: If records meet the standards: the non-federal entity will NOT be required to provide additional support or documentation for the work performed ( (i)(2)) BUT, if records of grantee do not meet new standards, ED may require PARs ( (i)(8)) PARs are not defined!! 84

85 Procurement 85

86 PROCUREMENT STANDARDS State, Local and Tribal Governments: States may use their own procurement policies and procedures to procure equipment. Other grantees and subgrantees must follow policies and procedures that meet the standards set out in EDGAR

87 PROCUREMENT STANDARDS NEW: All nonfederal entities must have documented procurement procedures which reflect applicable Federal, State, and local laws and regulations. 87

88 CONFLICT OF INTEREST NEW: If the non-federal entity has a parent, affiliate, or subsidiary organization that is not a state or local government the entity must also maintain written standards of conduct covering organization conflicts of interest! (b)(2) 88

89 VENDOR SELECTION PROCESS Method of procurement: NEW: Micro-purchase Small purchase procedures Competitive sealed bids Competitive proposals Noncompetitive proposals 89

90 90 90

91 VENDOR SELECTION PROCESS: MICRO-PURCHASE (a) NEW: Acquisition of supplies and services under $3,000 or less. May be awarded without soliciting competitive quotations if nonfederal entity considers the cost reasonable. To the extent practicable must distribute micro-purchases equitably among qualified suppliers. 91

92 VENDOR SELECTION PROCESS: NONCOMPETITIVE PROPOSALS Appropriate only when: The good or services is available only from a single source (sole source) There is a public emergency The awarding agency authorizes NEW: awarding agency or pass-through must expressly authorize noncompetitive proposals in response to written requires from nonfederal entity (f)(3) After soliciting a number of sources, competition is deemed inadequate 92

93 Property Management 93

94 INVENTORY MANAGEMENT Must have adequate controls in place to account for: Location of equipment Custody of equipment Security of equipment 94

95 EQUIPMENT Defined Significant changes on use and dispositions ( ) Shared use allowed if use will not interfere Clarified: shared use priorities: (1) projects supported by same federal awarding agency; (2) projects funded by other federal agencies; (3) nonfederal programs New: may trade in when acquiring replacement equipment without recourse federal agency 95

96 SUPPLIES Anything that is not equipment is considered supplies. Significant Technological Devices NEW: Computing devices Machines used to acquire, store, analyze, process, public data and other information electronically Includes accessories for printing, transmitting and receiving or storing electronic information Computing devices are supplies if less than $5,000 96

97 INTERNAL CONTROLS (b)(4) Regardless of cost, grantee must maintain effective control and safeguard all assets and assure that they are used solely for authorized purposes. 97

98 Records and Reviews 98

99 METHODS FOR COLLECTION, TRANSMISSION AND STORAGE OF INFORMATION o NEW: When original records are electronic and cannot be altered, there is no need to create and retain paper copies. o When original records are paper, electronic versions may be substituted through the use of duplication or other forms of electronic media provided they: o o o Are subject to periodic quality control reviews, Provide reasonable safeguards against alteration; and Remain readable. 99

100 100 REQUIREMENTS OF PASS- THROUGH ENTITIES 100

101 FEDERAL AWARDING AGENCY REVIEW OF RISK POSED BY APPLICANTS NEW: Fed Agency and Pass-Through must have in place a framework for evaluating risks before applicant receives funding 1. Financial Stability 2. Quality of Management System 3. History of Performance 4. Audit Reports 5. Applicant s Ability to Effectively Implement Program 101

102 SPECIFIC CONDITIONS Fed agency or Pass Through may impose additional Federal award conditions : Require reimbursement; Withhold funds until evidence of acceptable performance; More detailed reporting; Additional monitoring; Require grantee to obtain technical or management assistance; or Establish additional prior approvals. 102

103 MONITORING AND REPORTING PROGRAM PERFORMANCE , NEW: Monitoring by the Nonfederal Entity (self-assessment) Must monitor its activities to assure compliance with applicable federal requirements and performance expectations are achieved Must cover each program, function or activity (see also , Requirements for the Pass Through entity) Must submit performance reports at least annually 103

104 REQUIREMENTS FOR PASS-THROUGH ENTITIES Pass-through must monitor its subrecipients to assure compliance and performance goals are achieved Monitoring must include: 1. Review financial and programmatic reports 2. Ensure corrective action 3. Issue a management decision on audit findings if the award is from the pass-through 104

105 REQUIREMENTS FOR PASS-THROUGH ENTITIES NEW: Depending on assessment of risk, the following monitoring tools may be useful for the pass-through entity to ensure proper accountability and compliance with program requirements and achievement of performance goals: 1. Training + technical assistance on program-related matters 2. On-site reviews 3. Arranging for agreed-upon-procedures engagements (described in ) 105

106 REQUIREMENTS FOR PASS-THROUGH ENTITIES Pass-through must consider taking enforcement action ( ) based on non compliance: 1. Temporarily withhold cash payments pending correction 2. Disallow all or part of the cost 3. Wholly or partly suspend the award 4. Recommend to federal awarding agency suspension / debarment 5. Withhold further federal awards 6. Other remedies that may be legally available

107 AUDIT REQUIREMENTS 107

108 AUDIT REQUIREMENTS Current threshold $500,000. NEW: Threshold increased to $750,000 The federal agency, OIG, or GAO may arrange for audits in addition to single audit 108

109 FEDERAL AGENCY RESPONSIBILITIES NEW: The federal awarding agency must use cooperative audit resolution to improve federal program outcomes Cooperative Audit Resolution: means the use of audit followup techniques which promote prompt corrective action by improving communication, fostering collaboration, promoting trust and developing an understanding between the Federal agency and non-federal entity

110 AUDIT FINDINGS The auditor must report (for major programs): Significant deficiencies and material weaknesses in internal controls Significant instances of abuse Material noncompliance Known questioned costs > $25,000 Auditor will not normally find questioned costs for a program that is not audited as a major program NEW: But if auditor becomes aware of questioned costs > $25,000 for non-major program, must report 110

111 Reconsideration of Compliance Supplement Internal Controls 111

112 NOTICE OF INTENT 2/28/12-77 FR The Uniform Guidance will streamline compliance requirements to better target areas of risk 112

113 NPRM 2/1/13 78 FR 7294 OMB/COFAR proposed limiting the types of requirements for auditors in the Compliance Supplement 113

114 PROPOSED COMPLIANCE SUPPLEMENT TO COVER: 1. Allowable Activities 2. Allowable Costs 3. Cash Management Minimizing Time 4. Eligibility 5. Financial and Performance Reporting 6. Subrecipient Monitoring 7. Requirements Unique to the Program 114

115 PROPOSED COMPLIANCE SUPPLEMENT NOT TO COVER: 1. Davis-Bacon 2. Inventory Management 3. MOE / Earmarking 4. Period of Availability 5. Procurement 6. Program Income 7. Real Property Acquisition 115

116 FINAL RULE 78 FR /26/13 While most comments were in favor of proposed reduction of the number of compliance requirements, many voiced concern about the process Federal Agencies adding back provisions under special tests would increase burden Increased burden on pass-throughs 116

117 2015 COMPLIANCE SUPPLEMENT (APRIL 2015) Streamline the audit objectives and procedures for the 14 types of compliance requirements OMB / COFAR FAQ, Aug/14 (p.15) 117

118 QUESTIONS? 118

119 ~ LEGAL DISCLAIMER ~ This presentation is intended solely to provide general information and does not constitute legal advice or a legal service. This presentation does not create a clientlawyer relationship with Brustein & Manasevit, PLLC and, therefore, carries none of the protections under the D.C. Rules of Professional Conduct. Attendance at this presentation, a later review of any printed or electronic materials, or any follow-up questions or communications arising out of this presentation with any attorney at Brustein & Manasevit, PLLC does not create an attorney-client relationship with Brustein & Manasevit, PLLC. You should not take any action based upon any information in this presentation without first consulting legal counsel familiar with your particular circumstances. 119

Federal Grants Administration Updates. Erin Auerbach Esq. Brustein & Manasevit, PLLC

Federal Grants Administration Updates Erin Auerbach Esq. eauerbach@bruman.com Brustein & Manasevit, PLLC 1 Agenda Perkins Reauthorization Workforce Investment Opportunity Act (WIOA) Navigating the New

Federal Grants Administration Updates Erin Auerbach Esq. eauerbach@bruman.com Brustein & Manasevit, PLLC 1 Agenda Perkins Reauthorization Workforce Investment Opportunity Act (WIOA) Navigating the New

Overview of the New EDGAR (formerly the Uniform Grants Guidance)

") Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Uniform Grants Guidance. Colorado Charter School Institute Cassie Walgren, Controller

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

How to Draft New & Update Old Policies and Procedures. Agenda. Why?

How to Draft New & Update Old Policies and Procedures Brette Kaplan Wurzburg bwurzbrug@bruman.com Jennifer Segal jsegal@bruman.com Fall Forum 2014 Agenda Why policies and procedures are important? Logistics

How to Draft New & Update Old Policies and Procedures Brette Kaplan Wurzburg bwurzbrug@bruman.com Jennifer Segal jsegal@bruman.com Fall Forum 2014 Agenda Why policies and procedures are important? Logistics

TIME AND EFFORT DOCUMENTATION 101 TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR EDGAR AND THE OMB CIRCULARS

TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR TIFFANY R. WINTERS, ESQ. TWINTERS@BRUMAN.COM @TRWINTERS BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NASTID 2014 1

TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR TIFFANY R. WINTERS, ESQ. TWINTERS@BRUMAN.COM @TRWINTERS BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NASTID 2014 1

AGENDA. Subrecipient Monitoring Under the New Uniform Guidance. What is a passthrough

Subrecipient Monitoring Under the New Uniform Guidance Steven A. Spillan, Esq. sspillan@bruman.com Spring Forum 2015 AGENDA What is a pass through entity? How a does a pass through entity s responsibilities

Subrecipient Monitoring Under the New Uniform Guidance Steven A. Spillan, Esq. sspillan@bruman.com Spring Forum 2015 AGENDA What is a pass through entity? How a does a pass through entity s responsibilities

TEA Implementation of the New EDGAR

Implementation of the New EDGAR Office for Grants and Federal Fiscal Compliance Texas Education Agency ESC Cluster Site Implementation Training 2015 by the Texas Education Agency Agenda Introduction Written

Implementation of the New EDGAR Office for Grants and Federal Fiscal Compliance Texas Education Agency ESC Cluster Site Implementation Training 2015 by the Texas Education Agency Agenda Introduction Written

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

Roadmap to the Uniform Grant Guidance for School Districts

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

Presenter. Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance

The New OMB Uniform Guidance") Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance Presenter Richard Cunningham Quality Assurance & Technical Specialist Center

Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance Presenter Richard Cunningham Quality Assurance & Technical Specialist Center

Uniform Guidance Sponsored Projects Services

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

WHAT LAWS APPLY TO FEDERAL GRANTS: A HISTORICAL PERSPECTIVE

WHAT LAWS APPLY TO FEDERAL GRANTS: A HISTORICAL PERSPECTIVE LEIGH M. MANASEVIT, ESQ. LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM SPRING FORUM 2013 1 1960s: Congress began recognizing

WHAT LAWS APPLY TO FEDERAL GRANTS: A HISTORICAL PERSPECTIVE LEIGH M. MANASEVIT, ESQ. LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM SPRING FORUM 2013 1 1960s: Congress began recognizing

Policies and Procedures Under the Uniform Grant Guidance. Florida School Finance Officers Association November 10, 2016

Policies and Procedures Under the Uniform Grant Guidance Florida School Finance Officers Association November 10, 2016 Why? Single Audits Monitoring Staff Changes and Transitions New EDGAR requirements

Policies and Procedures Under the Uniform Grant Guidance Florida School Finance Officers Association November 10, 2016 Why? Single Audits Monitoring Staff Changes and Transitions New EDGAR requirements

Single Audit Entrance Conference Uniform Guidance Refresher

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

The OmniCircular - 2 CFR 200

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

Federal Rules for Sponsored Programs. Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Texas Education Agency. Division of Federal Fiscal Monitoring

Texas Education Agency Division of Federal Fiscal Monitoring The DO s and DON Ts of Administering Federal Grants Copyright 2016 by TEA DO s and DON'Ts of Administering Federal Grants Division of Federal

Texas Education Agency Division of Federal Fiscal Monitoring The DO s and DON Ts of Administering Federal Grants Copyright 2016 by TEA DO s and DON'Ts of Administering Federal Grants Division of Federal

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS. National Historical Publications and Records Commission

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

What EDGAR Is and What ESSA Will Bring! Tiffany R. Winters, Esq. Brustein & Manasevit June 2016

What EDGAR Is and What ESSA Will Bring! Tiffany R. Winters, Esq. Brustein & Manasevit www.bruman.com June 2016 1 From April Sept 2016 the ED OIG has secured approx. $50 Million in settlements, fines, restitutions,

What EDGAR Is and What ESSA Will Bring! Tiffany R. Winters, Esq. Brustein & Manasevit www.bruman.com June 2016 1 From April Sept 2016 the ED OIG has secured approx. $50 Million in settlements, fines, restitutions,

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT INTRODUCTION BACKGROUND On December 26, 2013, the Office of

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT INTRODUCTION BACKGROUND On December 26, 2013, the Office of

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews Denise Dusek, MPA Federal Funding Specialist ESC 20 Image obtained from google.com Education Service Center, Region 20 May 2018 2 1 Participants

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews Denise Dusek, MPA Federal Funding Specialist ESC 20 Image obtained from google.com Education Service Center, Region 20 May 2018 2 1 Participants

NEW EDGAR REGULATIONS

NEW EDGAR REGULATIONS FREQUENTLY ASKED QUESTIONS (FAQ): PRELIMINARY GUIDANCE APPLICABLE TO ALL FEDERALLY FUNDED GRANT PROGRAMS ADMINISTERED BY THE TEXAS EDUCATION AGENCY Blue text identifies changes, updates,

NEW EDGAR REGULATIONS FREQUENTLY ASKED QUESTIONS (FAQ): PRELIMINARY GUIDANCE APPLICABLE TO ALL FEDERALLY FUNDED GRANT PROGRAMS ADMINISTERED BY THE TEXAS EDUCATION AGENCY Blue text identifies changes, updates,

Are You Ready for This? The New Uniform Guidance 2 CFR 200

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN

TO 2 CFR 200 (UNIFORM ADMIN") Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Department of Contracts, Grants and Financial Administration, Texas Education Agency 1/26/18

Federal Grant Procurement Rules and Regulations and Federal Fiscal Monitoring Requirements Cory Green, Associate Commissioner Department of Contracts, Grants and Financial Administration Texas January

Federal Grant Procurement Rules and Regulations and Federal Fiscal Monitoring Requirements Cory Green, Associate Commissioner Department of Contracts, Grants and Financial Administration Texas January

NEW EDGAR REGULATIONS

NEW EDGAR REGULATIONS FREQUENTLY ASKED QUESTIONS (FAQ): PRELIMINARY GUIDANCE APPLICABLE TO ALL FEDERALLY FUNDED GRANT PROGRAMS ADMINISTERED BY THE TEXAS EDUCATION AGENCY Blue text identifies changes, updates,

NEW EDGAR REGULATIONS FREQUENTLY ASKED QUESTIONS (FAQ): PRELIMINARY GUIDANCE APPLICABLE TO ALL FEDERALLY FUNDED GRANT PROGRAMS ADMINISTERED BY THE TEXAS EDUCATION AGENCY Blue text identifies changes, updates,

December 26, 2014 NEW ADDITIONAL December 26, 2014 beginning December 26, /31/15, 6/30/16 Contents Reference Origin Appendix

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

Navigating the New Uniform Grant Guidance. Jack Reagan, Audit Partner Grant Thornton LLP. Grant Thornton. All rights reserved.

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

Federal Grant Guidance Compliance

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

EDGAR and Procurement CHOICE PARTNERS OCTOBER 12, 2016

EDGAR and Procurement CHOICE PARTNERS OCTOBER 12, 2016 Agenda Uniform Guidance Summary (Note: EDGAR for educational entities) General Federal Procurement Laws Thresholds and Implications Sole Source Vendors

EDGAR and Procurement CHOICE PARTNERS OCTOBER 12, 2016 Agenda Uniform Guidance Summary (Note: EDGAR for educational entities) General Federal Procurement Laws Thresholds and Implications Sole Source Vendors

Grants Management Scenarios

Grants Management Scenarios SCENARIO 1: Parker School District received a TIF grant in 2012. It followed the guidelines set forth in the application package and did not list specific vendors in its application.

Grants Management Scenarios SCENARIO 1: Parker School District received a TIF grant in 2012. It followed the guidelines set forth in the application package and did not list specific vendors in its application.

The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS Agenda Uniform Guidance Summary General Federal Procurement Laws Thresholds and Implications Sole Source Vendors Cooperative Purchasing

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS Agenda Uniform Guidance Summary General Federal Procurement Laws Thresholds and Implications Sole Source Vendors Cooperative Purchasing

Dollars & Sense: Federal Grant Financial

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

Uniform Guidance Subpart D Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance)

") Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Felipe Lopez, Vavrinek, Trine, Day & Co., LLP

San Luis Obispo County Community College District & San Luis Obispo County Office of Education 2012 F d l C li T i i 2012 Federal Compliance Training Felipe Lopez, Vavrinek, Trine, Day & Co., LLP Objectives

San Luis Obispo County Community College District & San Luis Obispo County Office of Education 2012 F d l C li T i i 2012 Federal Compliance Training Felipe Lopez, Vavrinek, Trine, Day & Co., LLP Objectives

10 CFR 600: KNOW YOUR REQUIREMENTS

WEATHERIZATION ASSISTANCE PROGRAM 10 CFR 600: KNOW YOUR REQUIREMENTS Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and

WEATHERIZATION ASSISTANCE PROGRAM 10 CFR 600: KNOW YOUR REQUIREMENTS Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

NECA Update The New Uniform Guidance 2 CFR 200

NECA Update The New Uniform Guidance 2 CFR 200 September 23, 2014 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B

NECA Update The New Uniform Guidance 2 CFR 200 September 23, 2014 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Overview of Procurement September

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Overview of Procurement September

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

APRIL 2009 COMMUNITY DEVELOPMENT BLOCK GRANTS/STATE S PROGRAM NORTH CAROLINA SMALL CITIES CDBG AND NEIGHBORHOOD STABILIZATION PROGRAM

APRIL 2009 14.228 State Project/Program: Federal Authorization: State Authorization: COMMUNITY DEVELOPMENT BLOCK GRANTS/STATE S PROGRAM NORTH CAROLINA SMALL CITIES CDBG AND NEIGHBORHOOD STABILIZATION PROGRAM

APRIL 2009 14.228 State Project/Program: Federal Authorization: State Authorization: COMMUNITY DEVELOPMENT BLOCK GRANTS/STATE S PROGRAM NORTH CAROLINA SMALL CITIES CDBG AND NEIGHBORHOOD STABILIZATION PROGRAM

2016 Compliance Supplement. Joe Bergene, CPA Altman, Rogers & Co.

2016 Compliance Supplement Joe Bergene, CPA Altman, Rogers & Co. Overview! Topics to be discussed:! Compliance supplement, what is it and why is it important to be familiar with it.! Overview of the supplement.!

2016 Compliance Supplement Joe Bergene, CPA Altman, Rogers & Co. Overview! Topics to be discussed:! Compliance supplement, what is it and why is it important to be familiar with it.! Overview of the supplement.!

PROCUREMENT POLICY FOR FEDERAL GRANTS

PROCUREMENT POLICY FOR FEDERAL GRANTS I. Introduction This Procurement Policy for Federal Grants applies to all expenditures of monies received through federal grants, whether those monies come directly

PROCUREMENT POLICY FOR FEDERAL GRANTS I. Introduction This Procurement Policy for Federal Grants applies to all expenditures of monies received through federal grants, whether those monies come directly

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO Lealan Miller, CPA, CGFM, Partner lmiller@eidebailly.com 208.383.4756 Organization of the Super-Circular, 2 CFR Part 200 Uniform Guidance

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO Lealan Miller, CPA, CGFM, Partner lmiller@eidebailly.com 208.383.4756 Organization of the Super-Circular, 2 CFR Part 200 Uniform Guidance

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY. Office of Contracts and Grants December, 2014

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

Effective July 1, 2015 Revised (October 2016)

") Lyford CISD Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and

Lyford CISD Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and

Understanding and Complying with Government Grants

Presents... Understanding and Complying with Objectives Obtain information to determine if applying for governmental grants is appropriate for your organization Obtain understanding of internal controls

Presents... Understanding and Complying with Objectives Obtain information to determine if applying for governmental grants is appropriate for your organization Obtain understanding of internal controls

CHAPTER 10 Grant Management

CHAPTER 10 Grant Management Table of Contents Page GRANT MANAGEMENT 1 Introduction... 1 Financial Management of Grants... 1 Planning and Budgeting... 1 Application and Implementation... 2 Monitoring...

CHAPTER 10 Grant Management Table of Contents Page GRANT MANAGEMENT 1 Introduction... 1 Financial Management of Grants... 1 Planning and Budgeting... 1 Application and Implementation... 2 Monitoring...

Administrative Regulation SANGER UNIFIED SCHOOL DISTRICT. Business and Noninstructional Operations FEDERAL GRANT FUNDS

Administrative Regulation SANGER UNIFIED SCHOOL DISTRICT AR 3230(a) Business and Noninstructional Operations FEDERAL GRANT FUNDS Allowable Costs Prior to obligating or spending any federal grant funds,

Administrative Regulation SANGER UNIFIED SCHOOL DISTRICT AR 3230(a) Business and Noninstructional Operations FEDERAL GRANT FUNDS Allowable Costs Prior to obligating or spending any federal grant funds,

General Procurement Requirements

Effective Date: July 1, 2018 Applicability: Grant Purchasing and Procurement Policy Related Policies: Moravian College Purchasing Policy and Business Travel Policy Policy: This policy provides guidelines

Effective Date: July 1, 2018 Applicability: Grant Purchasing and Procurement Policy Related Policies: Moravian College Purchasing Policy and Business Travel Policy Policy: This policy provides guidelines

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. AUSPAN Martha Taylor

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards Thursday, March 20, 2014, 12:30 p.m. 2:00 p.m. ET Venable LLP, Washington, DC Moderator: Jeffrey S. Tenenbaum,

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards Thursday, March 20, 2014, 12:30 p.m. 2:00 p.m. ET Venable LLP, Washington, DC Moderator: Jeffrey S. Tenenbaum,

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT)

") GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

Presented by: Jennifer Carrougher, Director of Federal Fiscal Policy Toni Bernethy, Director of Audit Resolution Annual Conference, Spokane WA

Presented by: Jennifer Carrougher, Director of Federal Fiscal Policy Toni Bernethy, Director of Audit Resolution 2017 Annual Conference, Spokane WA Agenda Federal Budget/ESSA Procurement/Suspension & Debarment

Presented by: Jennifer Carrougher, Director of Federal Fiscal Policy Toni Bernethy, Director of Audit Resolution 2017 Annual Conference, Spokane WA Agenda Federal Budget/ESSA Procurement/Suspension & Debarment

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida

Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida") Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

What were the Changes from the OMB Circulars to the Uniform Guidance Bag Lunch Webinar June 21, 2016

What were the Changes from the OMB Circulars to the Uniform Guidance Bag Lunch Webinar June 21, 2016 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

What were the Changes from the OMB Circulars to the Uniform Guidance Bag Lunch Webinar June 21, 2016 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES)

") TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES) The Texas General Land Office Community Development & Revitalization

TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES) The Texas General Land Office Community Development & Revitalization

Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs

3/15/14 Draft Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs Prepared for the Council of Chief State School Officers Federal

3/15/14 Draft Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs Prepared for the Council of Chief State School Officers Federal

The Uniform Guidance (2 CFR, Part 200)

") WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

N O N-PR O FI T O R G A NI Z A T I O NS

FIN A N C I A L M A N A G E M E N T G UID E F O R N O N-PR O FI T O R G A NI Z A T I O NS N A T I O N A L E ND O W M E N T F O R T H E A R TS O F F I C E O F INSP E C T O R G E N E R A L SEP T E M B E

FIN A N C I A L M A N A G E M E N T G UID E F O R N O N-PR O FI T O R G A NI Z A T I O NS N A T I O N A L E ND O W M E N T F O R T H E A R TS O F F I C E O F INSP E C T O R G E N E R A L SEP T E M B E

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist 1 Learning Objectives Participants will gain an understanding of the elements of preaward and how to think through required

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist 1 Learning Objectives Participants will gain an understanding of the elements of preaward and how to think through required

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT. July 1, 2017 June 30, 2018

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT July 1, 2017 June 30, 2018 This Grant Agreement (the Agreement ) is entered into by and between the Family and Children First Administrative Agency

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT July 1, 2017 June 30, 2018 This Grant Agreement (the Agreement ) is entered into by and between the Family and Children First Administrative Agency

WIOA SEC Administrative Provisions. Subparts: A - H. Presented by: 11/ 16/2016. Office of Grants Management

1 WIOA SEC. 683 Administrative Provisions Subparts: A - H Presented by: Office of Grants Management 11/ 16/2016 2 Today's Presenters Deborah Galloway Fiscal Policy Manager Division of Policy, Review &

1 WIOA SEC. 683 Administrative Provisions Subparts: A - H Presented by: Office of Grants Management 11/ 16/2016 2 Today's Presenters Deborah Galloway Fiscal Policy Manager Division of Policy, Review &

2010 Mauldin & Jenkins Single Audits for for Auditees

2010 Mauldin & Jenkins Single Audits for Auditees SINGLE AUDITS FOR AUDITEES Mauldin & Jenkins July 22, 2010 Macon August 3, 2010 - Atlanta PRESENTER Hope Pendergrass Manager Macon Office hpendergrass@mjcpa.com

2010 Mauldin & Jenkins Single Audits for Auditees SINGLE AUDITS FOR AUDITEES Mauldin & Jenkins July 22, 2010 Macon August 3, 2010 - Atlanta PRESENTER Hope Pendergrass Manager Macon Office hpendergrass@mjcpa.com

The State of Texas HELP AMERICA VOTE ACT PROVIDE THE SAME OPPORTUNITY FOR ACCESS AND PARTICIPATION TO INDIVIDUALS WITH DISABILITIES

The State of Texas Elections Division Phone: 512-463-5650 P.O. Box 12060 Fax: 512-475-2811 Austin, Texas 78711-2060 TTY: 7-1-1 www.sos.state.tx.us (800) 252-VOTE (8683) The Office of The Secretary of State

The State of Texas Elections Division Phone: 512-463-5650 P.O. Box 12060 Fax: 512-475-2811 Austin, Texas 78711-2060 TTY: 7-1-1 www.sos.state.tx.us (800) 252-VOTE (8683) The Office of The Secretary of State

Something for Everyone: Adjusting to the OMB s Super Circular May 25, :30 10:10 am 2 CPE

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees SHERYL L. STEPHENS BURKE, CPA, MST Nashua Office 102 Perimeter Road

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees SHERYL L. STEPHENS BURKE, CPA, MST Nashua Office 102 Perimeter Road

HAVA GRANTS AND MONITORING. Presented by: Dan Glotzer, Election Funds Manager and Venessa Miller, HAVA Grant Monitor

HAVA GRANTS AND MONITORING Presented by: Dan Glotzer, Election Funds Manager and Venessa Miller, HAVA Grant Monitor Overview of the Help America Vote Act (HAVA) Grants Types of Grants Benefit Periods Program

HAVA GRANTS AND MONITORING Presented by: Dan Glotzer, Election Funds Manager and Venessa Miller, HAVA Grant Monitor Overview of the Help America Vote Act (HAVA) Grants Types of Grants Benefit Periods Program

FY2016 Grant Application Workshop. Basics of Financial Management for Grant Applicants

FY2016 Grant Application Workshop Basics of Financial Management for Grant Applicants Jerron M. Johnson Chief Field Program Officer Missouri Community Service Commission November 19, 2015 Session Overview

FY2016 Grant Application Workshop Basics of Financial Management for Grant Applicants Jerron M. Johnson Chief Field Program Officer Missouri Community Service Commission November 19, 2015 Session Overview

PART 34-ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH FOR-PROFIT ORGANIZATIONS. Subpart A-General

PART 34-ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH FOR-PROFIT ORGANIZATIONS 34.1 Purpose. Subpart A-General (a) This part prescribes administrative requirements for awards to for-profit

PART 34-ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH FOR-PROFIT ORGANIZATIONS 34.1 Purpose. Subpart A-General (a) This part prescribes administrative requirements for awards to for-profit

U. S. Virgin Islands Compliance Agreement

U. S. Virgin Islands Compliance Agreement I. Overview of Issues... 3 II. Consequences for Not Meeting the Terms and Conditions of the Agreement... 4 A. Mutual Agreements and Understandings Regarding the

U. S. Virgin Islands Compliance Agreement I. Overview of Issues... 3 II. Consequences for Not Meeting the Terms and Conditions of the Agreement... 4 A. Mutual Agreements and Understandings Regarding the

Uniform Guidance Subpart D Administrative Requirements. Why This Session Is Needed. Lesson Overview & Module Objectives

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC 20410-0050 Special Attention of: NOTICE: SD-2015-01 Issued: FEB 2 6 2015 HUO Regional Directors HUD Field

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC 20410-0050 Special Attention of: NOTICE: SD-2015-01 Issued: FEB 2 6 2015 HUO Regional Directors HUD Field

DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION. CFDA No. Program Name Listed as

April 2018 ED Cross-Cutting Section ED DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION This section contains compliance requirements that apply to more than one Department of Education (ED)

April 2018 ED Cross-Cutting Section ED DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION This section contains compliance requirements that apply to more than one Department of Education (ED)

ATTACHMENTS A & B GRANT AGREEMENT TERMS AND CONDITIONS DEPARTMENT OF EDUCATION

ATTACHMENTS A & B GRANT AGREEMENT TERMS AND CONDITIONS DEPARTMENT OF EDUCATION I. COMPLIANCE WITH APPLICABLE LAWS The Grantee shall, at all times, comply with all federal, state and local laws, ordinances

ATTACHMENTS A & B GRANT AGREEMENT TERMS AND CONDITIONS DEPARTMENT OF EDUCATION I. COMPLIANCE WITH APPLICABLE LAWS The Grantee shall, at all times, comply with all federal, state and local laws, ordinances

Michigan Department of Education Guidance on Federal Grant Programs May 26, 2016

RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF EDUCATION LANSING BRIAN J. WHISTON STATE SUPERINTENDENT Michigan Department of Education Guidance on Federal Grant Programs May 26, 2016 BACKGROUND

RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF EDUCATION LANSING BRIAN J. WHISTON STATE SUPERINTENDENT Michigan Department of Education Guidance on Federal Grant Programs May 26, 2016 BACKGROUND

Effective July 1, 2015 Revised (Date)

") Brownsville Independent School District Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements

Brownsville Independent School District Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements

Grants to States for Low-Income Housing Projects in Lieu of Low-Income Housing Credits for 2009 GRANTEE TERMS AND CONDITIONS

Grants to States for Low-Income Housing Projects in Lieu of Low-Income Housing Credits for 2009 GRANTEE TERMS AND CONDITIONS 1. Authority a. Section 1602 of the American Recovery and Reinvestment Tax Act

Grants to States for Low-Income Housing Projects in Lieu of Low-Income Housing Credits for 2009 GRANTEE TERMS AND CONDITIONS 1. Authority a. Section 1602 of the American Recovery and Reinvestment Tax Act

A-133 Single Audits: Common Audit Findings & Ways to Mitigate and Prevent Them

A-133 Single Audits: Common Audit Findings & Ways to Mitigate and Prevent Them Wayne Finley, MBA, CGMS Mayor s Office Education & Government Services City of St. Petersburg, Florida Session Objectives

A-133 Single Audits: Common Audit Findings & Ways to Mitigate and Prevent Them Wayne Finley, MBA, CGMS Mayor s Office Education & Government Services City of St. Petersburg, Florida Session Objectives

Department of Defense Education Activity (DoDEA) DIVISION I: AWARD COVER PAGES

DIVISION I: AWARD COVER PAGES") DIVISION I: AWARD COVER PAGES Grant Number: (to be completed at the time of award) Type of award & Award Action: Grant New Award Total Grant Amount: (to be completed at the time of award) Obligation and

DIVISION I: AWARD COVER PAGES Grant Number: (to be completed at the time of award) Type of award & Award Action: Grant New Award Total Grant Amount: (to be completed at the time of award) Obligation and

Financial Grants Management. Session Outline. Grants Management Roles 4/19/10

Financial Grants Management Presented by: Donna Teague Grant Accounting Supervisor El Paso County Auditor s Office Small Counties Large Counties Grants Management Records Session Outline New Application

Financial Grants Management Presented by: Donna Teague Grant Accounting Supervisor El Paso County Auditor s Office Small Counties Large Counties Grants Management Records Session Outline New Application

FEDERAL TIME AND EFFORT REPORTING GUIDANCE HANDBOOK

FEDERAL TIME AND EFFORT REPORTING GUIDANCE HANDBOOK FOR LOCAL EDUCATIONAL AGENCIES (INDEPENDENT SCHOOL DISTRICTS, OPEN ENROLLMENT CHARTER SCHOOLS, AND EDUCATION SERVICE CENTERS) Texas Education Agency

FEDERAL TIME AND EFFORT REPORTING GUIDANCE HANDBOOK FOR LOCAL EDUCATIONAL AGENCIES (INDEPENDENT SCHOOL DISTRICTS, OPEN ENROLLMENT CHARTER SCHOOLS, AND EDUCATION SERVICE CENTERS) Texas Education Agency

Seminar on Financial Management. VOCA s National Conference

Seminar on Financial Management VOCA s National Conference Financial Management Systems In summary, a Financial Management System must be able to: Record and report on the -- Receipt; Obligation; and Expenditure

Seminar on Financial Management VOCA s National Conference Financial Management Systems In summary, a Financial Management System must be able to: Record and report on the -- Receipt; Obligation; and Expenditure

Jason Galloway, Associate Controller HSC Contract and Grant Accounting

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

MAXIMUS Higher Education Practice

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director, MAXIMUS Jason Guilbeault, Senior Consultant, MAXIMUS 1 MAXIMUS Higher Education Practice Headquartered in Northbrook,

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director, MAXIMUS Jason Guilbeault, Senior Consultant, MAXIMUS 1 MAXIMUS Higher Education Practice Headquartered in Northbrook,

Understanding the Adult Education State Director s Fiscal Responsibilities

Understanding the Adult Education State Director s Fiscal Responsibilities Office of Vocational and Adult Education Training for New State Staff November 5, 2013 Jay LeMaster OVERVIEW Sections of statute

Understanding the Adult Education State Director s Fiscal Responsibilities Office of Vocational and Adult Education Training for New State Staff November 5, 2013 Jay LeMaster OVERVIEW Sections of statute

GUIDANCE. Funds for Title I, Part B of the Rehabilitation Act of 1973, as amended. Made Available Under

GUIDANCE Funds for Title I, Part B of the Rehabilitation Act of 1973, as amended Made Available Under The American Recovery and Reinvestment Act of 2009 U.S. Department of Education Office of Special Education

GUIDANCE Funds for Title I, Part B of the Rehabilitation Act of 1973, as amended Made Available Under The American Recovery and Reinvestment Act of 2009 U.S. Department of Education Office of Special Education

Monitoring Your Adult Education Providers: Policy and Guidance for State Adult Education Directors

Monitoring Your Adult Education Providers: Policy and Guidance for State Adult Education Directors 2011 Annual State Directors Meeting Crystal City, VA May 2011 1 Introductions Name and Agency? How many

Monitoring Your Adult Education Providers: Policy and Guidance for State Adult Education Directors 2011 Annual State Directors Meeting Crystal City, VA May 2011 1 Introductions Name and Agency? How many

PERALTA COMMUNITY COLLEGE DISTRICT SINGLE AUDIT REPORT JUNE 30, 2010

PERALTA COMMUNITY COLLEGE DISTRICT SINGLE AUDIT REPORT JUNE 30, 2010 TABLE OF CONTENTS JUNE 30, 2010 Independent Auditors' Report on Internal Control Over Financial Reporting and on Compliance and Other

PERALTA COMMUNITY COLLEGE DISTRICT SINGLE AUDIT REPORT JUNE 30, 2010 TABLE OF CONTENTS JUNE 30, 2010 Independent Auditors' Report on Internal Control Over Financial Reporting and on Compliance and Other

2 CFR PART 215--UNIFORM ADMINISTRATIVE REQUIREMENTS

2 CFR PART 215--UNIFORM ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH INSTITUTIONS OF HIGHER EDUCATION, HOSPITALS, AND OTHER NON-PROFIT ORGANIZATIONS (OMB CIRCULAR A-110) May 11, 2004 OFFICE

2 CFR PART 215--UNIFORM ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH INSTITUTIONS OF HIGHER EDUCATION, HOSPITALS, AND OTHER NON-PROFIT ORGANIZATIONS (OMB CIRCULAR A-110) May 11, 2004 OFFICE

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT. July 1, 2018 June 30, 2019

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT July 1, 2018 June 30, 2019 This Grant Agreement (the Agreement ) is entered into by and between the Family and Children First Administrative Agency

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT July 1, 2018 June 30, 2019 This Grant Agreement (the Agreement ) is entered into by and between the Family and Children First Administrative Agency

Texas Association of County Auditors

Presentation to Texas Association of County Auditors New Uniform Grant Guidance and Update on 2014 OMB Circular A-133 Compliance Supplement by www.padgett-cpa.com Presenters Joel Perez, Jr., Partner Leader

Presentation to Texas Association of County Auditors New Uniform Grant Guidance and Update on 2014 OMB Circular A-133 Compliance Supplement by www.padgett-cpa.com Presenters Joel Perez, Jr., Partner Leader

Georgia Department of Education 7/19/2016

How to Draft and Revise Internal Controls: Fiscal and Programmatic Implementation of Title II, Part A July 19, 2016 Collaboratively Presented by the Georgia Department of Education Office of Internal Audits

How to Draft and Revise Internal Controls: Fiscal and Programmatic Implementation of Title II, Part A July 19, 2016 Collaboratively Presented by the Georgia Department of Education Office of Internal Audits

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards Frances Hodge Public Health Analyst, Southern Services Branch Division of Metropolitan

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards Frances Hodge Public Health Analyst, Southern Services Branch Division of Metropolitan

Ohio Enterprise Grants & Common Grants Compliance Issues

Ohio Enterprise Grants & Common Grants Compliance Issues Stacie Massey Ohio Office of Budget and Management June 12, 2018 The Growing Grants Business The State of Ohio manages $28 billion in federal grant

Ohio Enterprise Grants & Common Grants Compliance Issues Stacie Massey Ohio Office of Budget and Management June 12, 2018 The Growing Grants Business The State of Ohio manages $28 billion in federal grant

U.S. Department of Justice 42 U.S.C (a) N.C. Department of Public Safety

N.C. Department of Public Safety") APRIL 2016 16.575 CRIME VICTIM ASSISTANCE State Project/Program: VICTIMS OF CRIME ACT (VOCA) Federal Authorization: U.S. Department of Justice 42 U.S.C. 10603(a) Governor s Crime Commission Agency Contact

APRIL 2016 16.575 CRIME VICTIM ASSISTANCE State Project/Program: VICTIMS OF CRIME ACT (VOCA) Federal Authorization: U.S. Department of Justice 42 U.S.C. 10603(a) Governor s Crime Commission Agency Contact

AFFORDABLE CARE ACT (ACA) PERSONAL RESPONSIBILITY EDUCATION PROGRAM. N. C. Department of Health and Human Services Division of Public Health

PERSONAL RESPONSIBILITY EDUCATION PROGRAM. N. C. Department of Health and Human Services Division of Public Health") APRIL 2017 93.092 AFFORDABLE CARE ACT (ACA) PERSONAL RESPONSIBILITY EDUCATION PROGRAM State Project/Program: PERSONAL RESPONSIBILITY EDUCATION PROGRAM (PREP) Federal Authorization: State Authorization:

APRIL 2017 93.092 AFFORDABLE CARE ACT (ACA) PERSONAL RESPONSIBILITY EDUCATION PROGRAM State Project/Program: PERSONAL RESPONSIBILITY EDUCATION PROGRAM (PREP) Federal Authorization: State Authorization:

Federal Grant Policies and

Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and Education Department

Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and Education Department