Government-Nonprofit Contracting: From 30,000 Feet to Your Bottom Line

|

|

|

- Jessica Mariah West

- 5 years ago

- Views:

Transcription

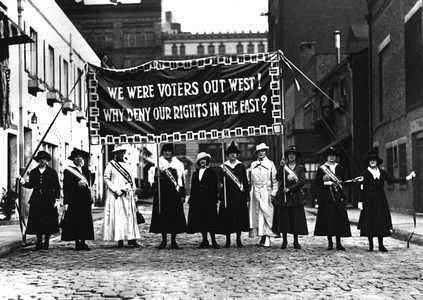

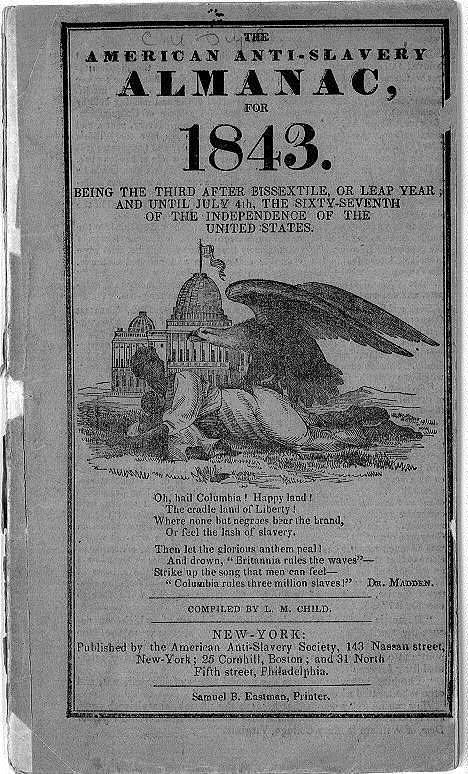

1 Government-Nonprofit Contracting: From 30,000 Feet to Your Bottom Line Tim Delaney President & CEO Nonprofit Missouri & UMKC s Center for Nonprofit Leadership Nov. 13, National Council of

2 25,000+ nonprofit members 42 State Associations & Nonprofit Allies 280+ Employees 500+ Board members Coast to Coast, Border to Border

3 The Problems Nationwide Missouri The Solutions General OMB Uniform Guidance Everywhere Missouri

4 The Problems

5 Great Threat Lack of Understanding Health Care Reform Citizen United Indifference/ Ignorance Nonprofit independence March of the States 2013 Localities & PILOTs

6 Lack of Understanding Passive & Meek

7 Challenges we ve faced

8 Together, a successful legacy Abolition Groups Suffrage Groups Townsend Clubs Civil Rights Groups

9 Lack of Understanding Sources of Nonprofit Revenues (e.g., hospital fees, tuition, ticket sales) One-third of nonprofit community revenues earned from government contracts and grants.

5.Paying Late SEE: special web portal http://govtcontracting.org/")

10 Withholding Money from Nonprofits Special Report Costs, Complexification, and Crisis: Government s Human Services Contracting System Hurts Everyone 1.Failure to Pay Full Costs (e.g., match; GAO) 2.Changing the Agreement Mid-Stream 3.Complexification of Application Process 4.Complexification of Reporting (Oversight) 5.Paying Late SEE: special web portal

11 Magnitude of Government s Reliance on Nonprofits Urban Institute s findings: In 2009: governments had 200,000 contracts with almost 33,000 human service nonprofits $100 billion worth of contracts governments doing their work through nonprofits

12 Costs & Consequences Who Gets Hurt: All around Nonprofits Donors/Funders Nonprofit Employees Nonprofits without Government Contracts

13 Government Contracting Problems: The Negative Ripple Effect Nonprofits with Government Contracts Nonprofits without Government Contracts Typically might include: After-school programs Children and family nonprofits Developmental disability Domestic violence shelters Food & nutrition programs Foster homes Health care clinics Health research Homeless shelters Hospitals Mental health nonprofits Soup kitchens The additional competition for limited grantmaking capacity then squeezes the nonprofits without any government contracts. Typically (but not always) include: Advocacy nonprofits Amateur sports Arts groups Associations Cultural institutions Community foundations Environmental groups Historic preservation Land conservation Religious schools Think tanks Watchdog groups

14 The Problems in Missouri

15 Withholding Money from Nonprofits 1. Failure to Pay Full Costs (e.g., GAO) 54% problem Missouri = 10 th worst at 61% 2. Changing the Agreement Mid-Stream 43% problem Missouri = 30 th worst at 39% 3. Complexification of Application Process 72% problem Missouri = 22 nd worst at 71% 4. Complexification of Reporting 72% problem Missouri = 14 th worst at 74% 5. Paying Late 45% problem Missouri = 29 th worst at 37% Nonprofits on average owed: $200,000+ by state governments; $108,000 by federal, $85,000 by local governments

16 Failure to Pay Full Costs Nonprofits Reporting Limitations on Full Costs in Government Contracts and Grants: In Missouri: 48% of nonprofits reported that governments imposed limits on program administrative/overhead costs 20% reported being paid ~zero~ 28% reported being paid between 1-7% 44% reported being paid between 8-10% 92% paid 10% or less In Missouri: 59% of nonprofits reported that governments imposed limits on general administrative/overhead costs 15% reported being paid ~zero~ 34% reported being paid between 1-7% 43% reported being paid between 8-10% 90% paid 10% or less

17 Compare Overhead Cost Ratios Business Norm Research shows that the average overhead ratio among for-profits and nonprofits alike is about 25-35% to be efficient and effective.

18 Compare Overhead Cost Ratios Business Norm Research shows that the average overhead ratio among for-profits and nonprofits alike is about 25-35% to be efficient and effective. Government Norm (CA State Govt) 76% of state agencies have indirect cost rates higher than 30%, 81% have rates higher than 20%, and no state agency has indirect cost rate of 10%.

19 Compare Overhead Cost Ratios Business Norm Research shows that the average overhead ratio among for-profits and nonprofits alike is about 25-35% to be efficient and effective. Government Norm (CA State Govt) 76% of state agencies have indirect cost rates higher than 30%, 81% have rates higher than 20%, and no state agency has indirect cost rate of 10%. What Missouri Governments Pay Nonprofits 92% of nonprofits facing caps reported being reimbursed at a rate of 10% or less.

20 Compare Overhead Cost Ratios Business Norm Research shows that the average overhead ratio among for-profits and nonprofits alike is about 25-35% to be efficient and effective. Government Norm (CA State Govt) 76% of state agencies have indirect cost rates higher than 30%, 81% have rates higher than 20%, and no state agency has indirect cost rate of 10%. What Missouri Governments Pay Nonprofits 92% of nonprofits facing caps reported being reimbursed at a rate of 10% or less.

21 Compounding the problem Off-loading/ Abandoning Programs cutting funding, not human need states: eliminated/reduced services for: Mental illness Disabled Elderly Children

22 The Solutions

23 The New OMB Uniform Guidance The BIG Deal How We Got Here Key Changes in the OMB Uniform Guidance How You Can Prepare for Implementation What You Can Do to Ensure the Promise Becomes Reality

24 (So, What s) The Big Deal? OMB Uniform Guidance

25 How We Got Here A Happy Advocacy Story An Advocacy Saga with a Happy Middle

26 How We Got Here Government-Nonprofit Contracting Work Recession, late payments, opportunity for reform Research, scope of the problems, solutions, implementation Abuses identified Recurring problems Solutions

27 Trend: Failure to pay indirect costs Research: for-profit/nonprofit avg overhead range=25-35% 53% nonprofits report governments limit indirect costs Of those governments a quarter paid = 0 half paid 7% or less three-quarters paid 10% or less

28 How We Got Here Government-Nonprofit Contracting Work OMB Draft Grants Reform Purpose: Streamline, reduce burdens, increase accountability Nonprofits Left Out: Main focus was governments and higher education Advocacy Campaign: Conference calls, webinars, surveys/polls, comments GAO, State Associations, national nonprofits National Task Force OMB Listened: Uniform Guidance 12/26/2013

29 How We Got Here Government-Nonprofit Contracting Work 2014 OMB Uniform Guidance Effective 12/26/2014 (agencies revise regs) Outreach Efforts information and clarity Federal webcast Frequently Asked Questions Oct. 2 Webcast a discussion 2014 New Data and Solutions

30 Federal Law Congress Appropriates the $$ Executive Branch Manages the $$

")

31 Sustainable Nonprofits Are Needed! Report GAO (May 2010) OMB Uniform Guidance

32 Reforms in OMB Uniform Guidance Some highlights (from 700+ pages): State & local governments, tribes, and other pass-through entities using federal funds will be required to reimburse nonprofit contractors and grantees for reasonable indirect costs. In some cases, it expands which administrative expenses can be reported as direct costs, rather than indirect. Eliminates some duplicative audit criteria, and clarifies cost allocation rules.

To negotiate a rate with the government")

33 What = reasonable indirect costs? 1. Apply the nonprofit s federally negotiated indirect cost rate if it already exists. 2. If a federally negotiated indirect cost rate does not already exist, then the NONPROFIT has the power to pick either option: a) To negotiate a rate with the government entity, OR b) To use the default minimum rate of 10%.

34 Step 1 of 3: Aware of the Reforms

35 Step 2: Advocacy to Protect the Reforms Federal State/Local Implementation & Compliance State/Local Application to Non-federal Funds

36 Step 3: Accounting Skills to Secure the Reforms Cost Allocations Common Knowledge Direct Costs Indirect Costs Other Costs Nonprofits Grantmakers Governments Negotiations

37 REFORMS Administrative Changes Cost Principles Audit Requirements

38 REFORMS & IMPLEMENTATION Administrative Reforms (A-110) Acronyms and Definitions General Provisions Pre-Award Requirements and Contents Post-Award Requirements for Financial and Program Management Cost Principle Reforms (A-122) Allowable and Unallowable Costs Indirect Cost Reimbursement Direct and Indirect Costs Procurement Requirements Audit Reforms (A-133) New Threshold Additional Government Audits and Internal Controls New Roles and Approaches

39 APPLICABILITY Key Dates Types of Awards and Subawards Impacted

40 PRE-AWARD REQUIREMENTS 200.1XX Requirements for Federal Agencies Award Posting RFP Content Standard Application Merit Review Risk Assessments

41 POST AWARD: PASS-THROUGH ENTITY REQUIREMENTS Single Audits Provide Subawardee Information Perform Risk Assessment for Subrecipient Monitoring Verify Audit Compliance Report in Accordance with FFATA Pay Subrecipient Indirect Cost Rate

42 REQUIRED INDIRECT COST REIMBURSEMENT With Federally Approved Negotiated Indirect Rate All Federal Agencies All Pass-through Entities 1 Four-Year Extension Option Without Federally Approved Indirect Rate 10% of MTDC De Minimis (Indefinite Use) or Negotiate a Rate Based on Federal Guidelines

43 DIRECT vs INDIRECT Generalizations Direct: Easily attributable to a specific program Indirect: Organizational or shared across programs Situational Determination Changes in OMB Uniform Guidance

44 ALLOWABLE vs UNALLOWABLE Allowable Reasonable Necessary Conforms with policies Treated consistently In accordance with GAAP Not used for cost share or match requirement Typical Unallowable Costs Fundraising Most Advertising and Public Relations Lobbying Entertainment, except program related Salaries above established caps

45 OMB Uniform Guidance: From Promise to Reality Advocacy Efforts to Clarify, Protect, and Fix Recap of what we know Nonprofit rights follow the money Waivers, intimidation prohibited Other Areas of continuing confusion Who triggers negotiations over indirect cost rate? Grant vs. Contract Other

Government audits (3 years later) State contracting review process Direct communications")

46 OMB Uniform Guidance: From Promise to Reality Advocacy Efforts to Clarify, Fix, and Protect Tools for Clarifying/Fixing the Uniform Guidance Nonprofit Survey Engagement through State Association National Task Force, Ad Hoc Advisory Committee, other Protecting Nonprofit Rights (a work in progress) Government audits (3 years later) State contracting review process Direct communications government officials What other ideas do you have?

47 Free Resources

48 Spread Data, Facts, Research, Trends (free!) Nonprofit Policy Agenda Bi-weekly Advocacy Matters Top 10 Nonprofit State & Local Policy Issues

49 Tim Delaney President & CEO Questions?

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Are You Ready for This? The New Uniform Guidance 2 CFR 200

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards Frances Hodge Public Health Analyst, Southern Services Branch Division of Metropolitan

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards Frances Hodge Public Health Analyst, Southern Services Branch Division of Metropolitan

NECA Update The New Uniform Guidance 2 CFR 200

NECA Update The New Uniform Guidance 2 CFR 200 September 23, 2014 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B

NECA Update The New Uniform Guidance 2 CFR 200 September 23, 2014 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B

Federal Grant Guidance Compliance

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN

TO 2 CFR 200 (UNIFORM ADMIN") Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS. AOA Conference Sacramento, CA January 12, 2014

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS AOA Conference Sacramento, CA January 12, 2014 Agenda 1. Introduction 2. History 3. Learning Objectives 4.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS AOA Conference Sacramento, CA January 12, 2014 Agenda 1. Introduction 2. History 3. Learning Objectives 4.

Presenter. Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance

The New OMB Uniform Guidance") Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance Presenter Richard Cunningham Quality Assurance & Technical Specialist Center

Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance Presenter Richard Cunningham Quality Assurance & Technical Specialist Center

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY. Office of Contracts and Grants December, 2014

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance)

") Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

UNCLE SAM S MONEY: Fundamentals of Federal Grant Law

UNCLE SAM S MONEY: Fundamentals of Federal Grant Law Webinar One April 5, 2016 Eleanor Evans, Esq. and Veronica Zhang, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 Uncle Sam s Money: Fundamentals of

UNCLE SAM S MONEY: Fundamentals of Federal Grant Law Webinar One April 5, 2016 Eleanor Evans, Esq. and Veronica Zhang, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 Uncle Sam s Money: Fundamentals of

Federal Rules for Sponsored Programs. Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Dollars & Sense: Federal Grant Financial

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards Thursday, March 20, 2014, 12:30 p.m. 2:00 p.m. ET Venable LLP, Washington, DC Moderator: Jeffrey S. Tenenbaum,

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards Thursday, March 20, 2014, 12:30 p.m. 2:00 p.m. ET Venable LLP, Washington, DC Moderator: Jeffrey S. Tenenbaum,

Roadmap to the Uniform Grant Guidance for School Districts

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

The OmniCircular - 2 CFR 200

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

Navigating the New Uniform Grant Guidance. Jack Reagan, Audit Partner Grant Thornton LLP. Grant Thornton. All rights reserved.

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

EMERGENCY SHELTER GRANTS PROGRAM EMERGENCY SHELTER GRANTS PROGRAM. U. S. Department of Housing and Urban Development

APRIL 2008 14.231 EMERGENCY SHELTER GRANTS PROGRAM State Project/Program: EMERGENCY SHELTER GRANTS PROGRAM U. S. Department of Housing and Urban Development Federal Authorization: 24 Code of Federal Regulations

APRIL 2008 14.231 EMERGENCY SHELTER GRANTS PROGRAM State Project/Program: EMERGENCY SHELTER GRANTS PROGRAM U. S. Department of Housing and Urban Development Federal Authorization: 24 Code of Federal Regulations

Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs

3/15/14 Draft Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs Prepared for the Council of Chief State School Officers Federal

3/15/14 Draft Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs Prepared for the Council of Chief State School Officers Federal

GATA GRANT ACCOUNTABILITY AND TRANSPARENCY ACT OVERVIEW T.H.E. CONFERENCE

GATA GRANT ACCOUNTABILITY AND TRANSPARENCY ACT OVERVIEW T.H.E. CONFERENCE 2.28.17 Topics of Discussion GATA Myths Applicability of GATA GATA Overview What s New Roles and Responsibilities Consequences

GATA GRANT ACCOUNTABILITY AND TRANSPARENCY ACT OVERVIEW T.H.E. CONFERENCE 2.28.17 Topics of Discussion GATA Myths Applicability of GATA GATA Overview What s New Roles and Responsibilities Consequences

EMERGENCY SHELTER GRANTS PROGRAM EMERGENCY SHELTER GRANTS PROGRAM. U. S. Department of Housing and Urban Development

APRIL 2011 14.231 EMERGENCY SHELTER GRANTS PROGRAM State Project/Program: EMERGENCY SHELTER GRANTS PROGRAM U. S. Department of Housing and Urban Development Federal Authorization: 24 Code of Federal Regulations

APRIL 2011 14.231 EMERGENCY SHELTER GRANTS PROGRAM State Project/Program: EMERGENCY SHELTER GRANTS PROGRAM U. S. Department of Housing and Urban Development Federal Authorization: 24 Code of Federal Regulations

UNIFORM GUIDANCE UPDATE

UNIFORM GUIDANCE UPDATE CINDY KIEL Executive Associate Vice Chancellor Office of Research Michael Allred Associate Vice Chancellor for Finance/Controller What is the Uniform Guidance? Uniform Administrative

UNIFORM GUIDANCE UPDATE CINDY KIEL Executive Associate Vice Chancellor Office of Research Michael Allred Associate Vice Chancellor for Finance/Controller What is the Uniform Guidance? Uniform Administrative

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist 1 Learning Objectives Participants will gain an understanding of the elements of preaward and how to think through required

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist 1 Learning Objectives Participants will gain an understanding of the elements of preaward and how to think through required

Federal Grants and Financial Assistance 2017 Training Catalog

1 P a g e Who are we? Meet Colleague Consulting Colleague Consulting LLC is a 19-year-old small business specializing in training, human resource development, and organizational development services for

1 P a g e Who are we? Meet Colleague Consulting Colleague Consulting LLC is a 19-year-old small business specializing in training, human resource development, and organizational development services for

AGENDA. Subrecipient Monitoring Under the New Uniform Guidance. What is a passthrough

Subrecipient Monitoring Under the New Uniform Guidance Steven A. Spillan, Esq. sspillan@bruman.com Spring Forum 2015 AGENDA What is a pass through entity? How a does a pass through entity s responsibilities

Subrecipient Monitoring Under the New Uniform Guidance Steven A. Spillan, Esq. sspillan@bruman.com Spring Forum 2015 AGENDA What is a pass through entity? How a does a pass through entity s responsibilities

WELCOME. Pre-Award Phase Training

WELCOME Pre-Award Phase Training Morning Session Welcome GATA and New Federal Guidance Overview Cost Principles - Basic Considerations 10:00 10:15 BREAK Cost Principles Basic Consideration Cost Principles

WELCOME Pre-Award Phase Training Morning Session Welcome GATA and New Federal Guidance Overview Cost Principles - Basic Considerations 10:00 10:15 BREAK Cost Principles Basic Consideration Cost Principles

Uniform Guidance Sponsored Projects Services

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

University of Pittsburgh SPONSORED PROJECT FINANCIAL GUIDELINE Subject: SUBRECIPIENT MONITORING

I. Scope Subrecipient monitoring is the process by which the University selects, monitors, controls, and accounts for University subcontractors or subrecipients utilized on sponsored projects in accordance

I. Scope Subrecipient monitoring is the process by which the University selects, monitors, controls, and accounts for University subcontractors or subrecipients utilized on sponsored projects in accordance

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO Lealan Miller, CPA, CGFM, Partner lmiller@eidebailly.com 208.383.4756 Organization of the Super-Circular, 2 CFR Part 200 Uniform Guidance

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO Lealan Miller, CPA, CGFM, Partner lmiller@eidebailly.com 208.383.4756 Organization of the Super-Circular, 2 CFR Part 200 Uniform Guidance

ADMINISTRATIVE PRACTICE LETTER

UNIVERSITY OF MAINE SYSTEM Number 50 Issue 1 Page 1 of 7 Date 1/09/04 ADMINISTRATIVE PRACTICE LETTER General SUBJECT: Sponsored Agreements Subrecipient Audits and Monitoring Requirements OMB Circular A-133:

UNIVERSITY OF MAINE SYSTEM Number 50 Issue 1 Page 1 of 7 Date 1/09/04 ADMINISTRATIVE PRACTICE LETTER General SUBJECT: Sponsored Agreements Subrecipient Audits and Monitoring Requirements OMB Circular A-133:

Welcome. Please help yourself to breakfast.

Welcome Please help yourself to breakfast. 1 Agenda 8:00-8:45am Registration and Breakfast 8:45-8:55am Welcome 8:55-9:25am Rhea Hubbard, OMB Office of Federal Financial Management 9:25-9:55am Q&A and Discussion

Welcome Please help yourself to breakfast. 1 Agenda 8:00-8:45am Registration and Breakfast 8:45-8:55am Welcome 8:55-9:25am Rhea Hubbard, OMB Office of Federal Financial Management 9:25-9:55am Q&A and Discussion

OMB Uniform Guidance 2 CFR Part 200

OMB Uniform Guidance 2 CFR Part 200 What has changed - What hasn t What works What doesn t March 24, 2015 This session will focus on Brief outline of changes under the new OMB Uniform Guidance 2 CFR Part

OMB Uniform Guidance 2 CFR Part 200 What has changed - What hasn t What works What doesn t March 24, 2015 This session will focus on Brief outline of changes under the new OMB Uniform Guidance 2 CFR Part

The Uniform Guidance (2 CFR, Part 200)

") WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

Updated. The Minimalist s Guide to the New Procurement Standards in 2 CFR Part 200 Uniform Guidance

Updated The Minimalist s Guide to the New Procurement Standards in 2 CFR Part 200 Uniform Guidance 1 Procurement Standards General Standards must use documented procurement procedures which

Updated The Minimalist s Guide to the New Procurement Standards in 2 CFR Part 200 Uniform Guidance 1 Procurement Standards General Standards must use documented procurement procedures which

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT INTRODUCTION BACKGROUND On December 26, 2013, the Office of

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT INTRODUCTION BACKGROUND On December 26, 2013, the Office of

UNIFORM GUIDANCE OVERVIEW. Budget Officers Meeting January 28, 2015

UNIFORM GUIDANCE OVERVIEW Budget Officers Meeting January 28, 2015 OMB Circulars Before and After Eight circulars condensed to one new comprehensive set of requirements for recipients of federal awards

UNIFORM GUIDANCE OVERVIEW Budget Officers Meeting January 28, 2015 OMB Circulars Before and After Eight circulars condensed to one new comprehensive set of requirements for recipients of federal awards

Victims of Crime Act (VOCA) Grant Application Frequently Asked Questions (FAQs) for the Supplemental Competitive Funding Announcement

Grant Application Frequently Asked Questions (FAQs) for the Supplemental Competitive Funding Announcement") Victims of Crime Act (VOCA) Grant Application Frequently Asked Questions (FAQs) for the 2015-2016 Supplemental Competitive Funding Announcement Overview: OCVS recognizes that current VOCA subgrantees have

Victims of Crime Act (VOCA) Grant Application Frequently Asked Questions (FAQs) for the 2015-2016 Supplemental Competitive Funding Announcement Overview: OCVS recognizes that current VOCA subgrantees have

AAU Association of American Universities APLU Association of Public and Land-grant Universities

AAU Association of American Universities APLU Association of Public and Land-grant Universities June 2, 2013 Mr. Daniel I. Werfel Controller, Office of Federal Financial Management Office of Management

AAU Association of American Universities APLU Association of Public and Land-grant Universities June 2, 2013 Mr. Daniel I. Werfel Controller, Office of Federal Financial Management Office of Management

FY2016 Grant Application Workshop. Basics of Financial Management for Grant Applicants

FY2016 Grant Application Workshop Basics of Financial Management for Grant Applicants Jerron M. Johnson Chief Field Program Officer Missouri Community Service Commission November 19, 2015 Session Overview

FY2016 Grant Application Workshop Basics of Financial Management for Grant Applicants Jerron M. Johnson Chief Field Program Officer Missouri Community Service Commission November 19, 2015 Session Overview

Post Uniform Grant Guidance implementation from an auditor perspective

Post Uniform Grant Guidance implementation from an auditor perspective Jeff Zeichner Patrick Smith Agenda Uniform Grant Guidance review Challenges with UGG implementation SEFA Internal controls and compliance

Post Uniform Grant Guidance implementation from an auditor perspective Jeff Zeichner Patrick Smith Agenda Uniform Grant Guidance review Challenges with UGG implementation SEFA Internal controls and compliance

Uniform Guidance Subpart D Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

New Uniform Consolidated Grants Guidance

New Uniform Consolidated Grants Guidance From Accountability for Compliance to Accountability for Results The Honorable Jim Taylor and Robert Shea December 2014 Agenda Background Former circulars Consolidated

New Uniform Consolidated Grants Guidance From Accountability for Compliance to Accountability for Results The Honorable Jim Taylor and Robert Shea December 2014 Agenda Background Former circulars Consolidated

Performance and Financial Monitoring and Reporting

2 CFR 200 Uniform Guidance Performance & Financial Monitoring / Reporting and Subrecipient Monitoring Kris Rhodes, Director MAXIMUS Performance and Financial Monitoring and Reporting 1 Financial Reporting

2 CFR 200 Uniform Guidance Performance & Financial Monitoring / Reporting and Subrecipient Monitoring Kris Rhodes, Director MAXIMUS Performance and Financial Monitoring and Reporting 1 Financial Reporting

Uniform Guidance Subpart D Administrative Requirements. Why This Session Is Needed. Lesson Overview & Module Objectives

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

Single Audit Entrance Conference Uniform Guidance Refresher

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

North Carolina Department of Administration NC Council for Women

April 2016 93.671 Family Violence Prevention & Services Grant Federal Authorization: Funding was initially authorized through the Family Violence Prevention and Services Act, which was enacted in Sections

April 2016 93.671 Family Violence Prevention & Services Grant Federal Authorization: Funding was initially authorized through the Family Violence Prevention and Services Act, which was enacted in Sections

OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards

OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Research Advisory Board What PIs Need to Know January 2015 1 Background o When and Why? o Overview Important

OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Research Advisory Board What PIs Need to Know January 2015 1 Background o When and Why? o Overview Important

Hooray! My Project Is Funded. now what? The Grants Management Handbook. Southwestern Community College

Hooray! My Project Is Funded now what? The Grants Management Handbook Southwestern Community College Table of Contents: Overview... 3 Getting Started... 4 Who Does What? Key People and Places... 7 Records

Hooray! My Project Is Funded now what? The Grants Management Handbook Southwestern Community College Table of Contents: Overview... 3 Getting Started... 4 Who Does What? Key People and Places... 7 Records

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. AUSPAN Martha Taylor

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

OMB New Uniform Guidance

ICCCFO Spring 2015 Conference April 8 10, 2015 Oglesby, IL Starved Rock Lodge and Convention Center OMB New Uniform Guidance Wednesday, April 8, 2015 4:15 pm 4:45 pm Presented by: Katherine Eilers, CPA,

ICCCFO Spring 2015 Conference April 8 10, 2015 Oglesby, IL Starved Rock Lodge and Convention Center OMB New Uniform Guidance Wednesday, April 8, 2015 4:15 pm 4:45 pm Presented by: Katherine Eilers, CPA,

Office of Sponsored Programs RESEARCH ADMINISTRATORS FORUM. December 2017

Office of Sponsored Programs RESEARCH ADMINISTRATORS FORUM December 2017 Agenda Feedback on Subawards Process What is FFATA and what does it mean to the Research Administration community at NYU? University

Office of Sponsored Programs RESEARCH ADMINISTRATORS FORUM December 2017 Agenda Feedback on Subawards Process What is FFATA and what does it mean to the Research Administration community at NYU? University

COMMUNITY DEVELOPMENT BLOCK GRANT PROGRAM OVERVIEW. Town of Union CDBG Program

COMMUNITY DEVELOPMENT BLOCK GRANT PROGRAM OVERVIEW Town of Union CDBG Program Contact Sara L. Zubalsky-Peer Community Development Coordinator 3111 E. Main Street Endwell, NY 13760 Email: szubalsky@townofunion.com

COMMUNITY DEVELOPMENT BLOCK GRANT PROGRAM OVERVIEW Town of Union CDBG Program Contact Sara L. Zubalsky-Peer Community Development Coordinator 3111 E. Main Street Endwell, NY 13760 Email: szubalsky@townofunion.com

NOT-FOR-PROFIT INSIDER

NOT-FOR-PROFIT INSIDER VOLUME 9 :: ISSUE 3 In This Issue: Streamlining OMB Guidance For Federal Funding Of Nonprofit Organizations New 1023-EZ Makes Applying For 501(C)(3) Tax-Exempt Status Easier Identifying

NOT-FOR-PROFIT INSIDER VOLUME 9 :: ISSUE 3 In This Issue: Streamlining OMB Guidance For Federal Funding Of Nonprofit Organizations New 1023-EZ Makes Applying For 501(C)(3) Tax-Exempt Status Easier Identifying

Trainer(s): Dr. Beverly A. Browning ecivis, Inc.

: Dr. Beverly A. Browning ecivis, Inc.") 01: Securing and Managing Federal Grants Trainer(s): Dr. Beverly A. Browning ecivis, Inc. Securing and Managing Federal Grants Dr. Beverly A. Browning Vice President Grants Professional Services (GPS)

01: Securing and Managing Federal Grants Trainer(s): Dr. Beverly A. Browning ecivis, Inc. Securing and Managing Federal Grants Dr. Beverly A. Browning Vice President Grants Professional Services (GPS)

December 26, 2014 NEW ADDITIONAL December 26, 2014 beginning December 26, /31/15, 6/30/16 Contents Reference Origin Appendix

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees SHERYL L. STEPHENS BURKE, CPA, MST Nashua Office 102 Perimeter Road

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees SHERYL L. STEPHENS BURKE, CPA, MST Nashua Office 102 Perimeter Road

Through its advocacy and public education work, the Center seeks to champion and protect the nonprofit

2016 Advocacy Plan Introduction: The Center for Non-Profits mission is to build the power of New Jersey s non-profit community to improve the quality of life for the people of our state. To pursue its

2016 Advocacy Plan Introduction: The Center for Non-Profits mission is to build the power of New Jersey s non-profit community to improve the quality of life for the people of our state. To pursue its

COMMUNITY DEVELOPMENT BLOCK GRANT (CDBG) Subrecipient Workshop

Subrecipient Workshop") COMMUNITY DEVELOPMENT BLOCK GRANT (CDBG) Subrecipient Workshop CDBG Subrecipient Training CDBG Overview Grant Requirements Client Files Administration Monitoring Considerations Anticipated Timeline Application

COMMUNITY DEVELOPMENT BLOCK GRANT (CDBG) Subrecipient Workshop CDBG Subrecipient Training CDBG Overview Grant Requirements Client Files Administration Monitoring Considerations Anticipated Timeline Application

Subrecipient Monitoring Procedures

Subrecipient Monitoring Procedures This procedure describes the proper management of subrecipient activity under Purdue sponsored program awards. Definitions Award: An award is a binding agreement between

Subrecipient Monitoring Procedures This procedure describes the proper management of subrecipient activity under Purdue sponsored program awards. Definitions Award: An award is a binding agreement between

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC 20410-0050 Special Attention of: NOTICE: SD-2015-01 Issued: FEB 2 6 2015 HUO Regional Directors HUD Field

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC 20410-0050 Special Attention of: NOTICE: SD-2015-01 Issued: FEB 2 6 2015 HUO Regional Directors HUD Field

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Overview of Procurement September

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Overview of Procurement September

Texas Association of County Auditors

Presentation to Texas Association of County Auditors New Uniform Grant Guidance and Update on 2014 OMB Circular A-133 Compliance Supplement by www.padgett-cpa.com Presenters Joel Perez, Jr., Partner Leader

Presentation to Texas Association of County Auditors New Uniform Grant Guidance and Update on 2014 OMB Circular A-133 Compliance Supplement by www.padgett-cpa.com Presenters Joel Perez, Jr., Partner Leader

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS. National Historical Publications and Records Commission

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

Grants Management Scenarios

Grants Management Scenarios SCENARIO 1: Parker School District received a TIF grant in 2012. It followed the guidelines set forth in the application package and did not list specific vendors in its application.

Grants Management Scenarios SCENARIO 1: Parker School District received a TIF grant in 2012. It followed the guidelines set forth in the application package and did not list specific vendors in its application.

OUTGOING SUBAWARD GUIDE: INFORMATION FOR UWM PRINCIPAL INVESTIGATORS VERSION 1, JULY 2015

OUTGOING SUBAWARD GUIDE: INFORMATION FOR UWM PRINCIPAL INVESTIGATORS VERSION 1, JULY 2015 INTRODUCTION The University of Wisconsin-Milwaukee (UWM) is the prime recipient on a wide range of sponsored awards

OUTGOING SUBAWARD GUIDE: INFORMATION FOR UWM PRINCIPAL INVESTIGATORS VERSION 1, JULY 2015 INTRODUCTION The University of Wisconsin-Milwaukee (UWM) is the prime recipient on a wide range of sponsored awards

Subrecipient Monitoring Under 2 CFR 200. Kris Rhodes, MS Director, Higher Education Practice

Subrecipient Monitoring Under 2 CFR 200 Kris Rhodes, MS Director, Higher Education Practice krisrhodes@maximus.com 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL Satellite Offices

Subrecipient Monitoring Under 2 CFR 200 Kris Rhodes, MS Director, Higher Education Practice krisrhodes@maximus.com 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL Satellite Offices

POOR AND NEEDY DIVISION Grant Application Resources Operating Programs

POOR AND NEEDY DIVISION Grant Application Resources Operating Programs May 2012 Notes These resources are meant to be used in conjunction with the Poor and Needy Division Guidelines posted on our website.

POOR AND NEEDY DIVISION Grant Application Resources Operating Programs May 2012 Notes These resources are meant to be used in conjunction with the Poor and Needy Division Guidelines posted on our website.

Overview of the New EDGAR (formerly the Uniform Grants Guidance)

") Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida

Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida") Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

OMB Uniform Guidance ( UG ) Briefing. ASRSP & OSR Brown Bag Tuesday, January 27 th

Briefing. ASRSP & OSR Brown Bag Tuesday, January 27 th") OMB Uniform Guidance ( UG ) Briefing ASRSP & OSR Brown Bag Tuesday, January 27 th Background The UG is the single biggest regulatory change in the last fifty years in research administration Interesting

OMB Uniform Guidance ( UG ) Briefing ASRSP & OSR Brown Bag Tuesday, January 27 th Background The UG is the single biggest regulatory change in the last fifty years in research administration Interesting

Models of Accountability and the American Recovery and Reinvestment Act

Models of Accountability and the American Recovery and Reinvestment Act J. Christopher Mihm Managing Director, Strategic Issues U.S. Government Accountability Office June 2, 2011 The Bottom Line The Recovery

Models of Accountability and the American Recovery and Reinvestment Act J. Christopher Mihm Managing Director, Strategic Issues U.S. Government Accountability Office June 2, 2011 The Bottom Line The Recovery

INTRODUCTION FUNDS AVAILABILITY

Request for Proposals (RFP) HUD Continuum of Care (CoC) Homeless Assistance Issued June 9, 2016 Corrected June 21, 2016 Pursuant to HUD Correction of Permanent Housing Bonus Percentage to 5% INTRODUCTION

Request for Proposals (RFP) HUD Continuum of Care (CoC) Homeless Assistance Issued June 9, 2016 Corrected June 21, 2016 Pursuant to HUD Correction of Permanent Housing Bonus Percentage to 5% INTRODUCTION

MAXIMUS Higher Education Practice

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director, MAXIMUS Jason Guilbeault, Senior Consultant, MAXIMUS 1 MAXIMUS Higher Education Practice Headquartered in Northbrook,

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director, MAXIMUS Jason Guilbeault, Senior Consultant, MAXIMUS 1 MAXIMUS Higher Education Practice Headquartered in Northbrook,

UNIFORM GUIDANCE IMPLEMENTATION

UNIFORM GUIDANCE IMPLEMENTATION Presented by Sara Judd, OSR Consultant October 2014 Uniform Guidance Implementation what we know and what we re guessing Ready, Set, Go 2014 Fred Hutchinson Cancer Research

UNIFORM GUIDANCE IMPLEMENTATION Presented by Sara Judd, OSR Consultant October 2014 Uniform Guidance Implementation what we know and what we re guessing Ready, Set, Go 2014 Fred Hutchinson Cancer Research

CoC Eligible Costs, Match, and Leverage

CoC Eligible Costs, Match, and Leverage Illinois TA Discussion Series November 7, 2017 Today s Agenda Introductions Who we are, about the Illinois TA Discussion Series, and additional information about

CoC Eligible Costs, Match, and Leverage Illinois TA Discussion Series November 7, 2017 Today s Agenda Introductions Who we are, about the Illinois TA Discussion Series, and additional information about

City of Alameda Program Guidelines for CDBG FY18-19

Notice of Funding Availability Request for Proposal (NOFA/RFP) Community Development Block Grant (CDBG) & HOME Investment Partnerships Program (HOME) Program Guidelines July 1, 2018 - June 30, 2019 City

Notice of Funding Availability Request for Proposal (NOFA/RFP) Community Development Block Grant (CDBG) & HOME Investment Partnerships Program (HOME) Program Guidelines July 1, 2018 - June 30, 2019 City

Request for Proposals Frequently Asked Questions RFP III: INCREASING FOUNDATION OPENNESS. March RFP FAQ v

Request for Proposals Frequently Asked Questions RFP III: INCREASING FOUNDATION OPENNESS March 2015 RFP FAQ v03042015 1 The following frequently asked questions and answers reflect the questions we received

Request for Proposals Frequently Asked Questions RFP III: INCREASING FOUNDATION OPENNESS March 2015 RFP FAQ v03042015 1 The following frequently asked questions and answers reflect the questions we received

2009 American Recovery and Reinvestment Act (ARRA)

") 2009 American Recovery and Reinvestment Act (ARRA) Understanding Compliance and Reporting Requirements Associated with ARRA Stimulus Funds November 19, 2009 2009 American Recovery & Reinvestment Act Today

2009 American Recovery and Reinvestment Act (ARRA) Understanding Compliance and Reporting Requirements Associated with ARRA Stimulus Funds November 19, 2009 2009 American Recovery & Reinvestment Act Today

2017 Advancing Health Reform Through Advocacy Request for Proposals Frequently Asked Questions: February 3, 2017

1 2017 Advancing Health Reform Through Advocacy Request for Proposals Frequently Asked Questions: February 3, 2017 ELIGIBILITY Q. Who can apply for a grant from MeHAF? A. Generally, the applicant organization

1 2017 Advancing Health Reform Through Advocacy Request for Proposals Frequently Asked Questions: February 3, 2017 ELIGIBILITY Q. Who can apply for a grant from MeHAF? A. Generally, the applicant organization

TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES)

") TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES) The Texas General Land Office Community Development & Revitalization

TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES) The Texas General Land Office Community Development & Revitalization

Subrecipient vs. Contractor: Guidance on Appropriate Classification of Legal Relationship

HARVARD UNIVERSITY Responsible Office: Office for Sponsored Programs Date First Effective: October 18, 2011 Revision Date: December 26, 2014 Subrecipient vs. Contractor: Guidance on Appropriate Classification

HARVARD UNIVERSITY Responsible Office: Office for Sponsored Programs Date First Effective: October 18, 2011 Revision Date: December 26, 2014 Subrecipient vs. Contractor: Guidance on Appropriate Classification

Something for Everyone: Adjusting to the OMB s Super Circular May 25, :30 10:10 am 2 CPE

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

Safeguarding Federal Funds

Safeguarding Federal Funds Purpose Understand the mission of the OIG Preventing fraud in your organization Know how to contact the OIG What the OIG Does Promotes Economy, Efficiency, and Effectiveness

Safeguarding Federal Funds Purpose Understand the mission of the OIG Preventing fraud in your organization Know how to contact the OIG What the OIG Does Promotes Economy, Efficiency, and Effectiveness

Ryan White HIV/AIDS Program Fiscal Health Series. Systems to Sustainability TM. Federal Grants

Ryan White HIV/AIDS Program Fiscal Health Series Systems to Sustainability TM Federal Grants INTRODUCTION Sound fiscal management is critical for organizations to improve access to health care, advance

Ryan White HIV/AIDS Program Fiscal Health Series Systems to Sustainability TM Federal Grants INTRODUCTION Sound fiscal management is critical for organizations to improve access to health care, advance

PART 3 COMPLIANCE REQUIREMENTS

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION Overview The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribes, institutions of higher

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION Overview The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribes, institutions of higher

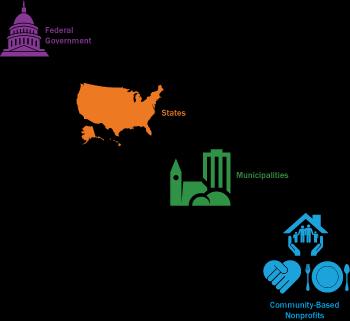

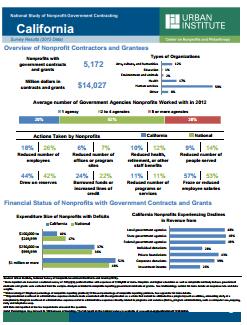

Contracts and Grants between Nonprofits and Government

br I e f # 03 DeC. 2013 Government-Nonprofit Contracting Relationships www.urban.org INsIDe this IssUe In 2012, local, state, and federal governments worked with nearly 56,000 nonprofit organizations.

br I e f # 03 DeC. 2013 Government-Nonprofit Contracting Relationships www.urban.org INsIDe this IssUe In 2012, local, state, and federal governments worked with nearly 56,000 nonprofit organizations.

Base. Base Determination and Cost Sharing. Bases represent the direct cost activities of an institution. Generally they consist of: 2/10/2014

Determination and Cost Sharing s represent the direct cost activities of an institution. Generally they consist of:» Instruction & departmental research» Organized research» Other sponsored activity (public

Determination and Cost Sharing s represent the direct cost activities of an institution. Generally they consist of:» Instruction & departmental research» Organized research» Other sponsored activity (public

Match and Leveraged Resources

Match and Leveraged Resources Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, Designed requirements for DOL-ETA governing direct cost recipients principles, and administrative their subrecipients

Match and Leveraged Resources Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, Designed requirements for DOL-ETA governing direct cost recipients principles, and administrative their subrecipients

NSF OIG Audit Update NORTHEAST CONFERENCE ON COLLEGE COST ACCOUNTING

NSF OIG Audit Update 1 NORTHEAST CONFERENCE ON COLLEGE COST ACCOUNTING S e p t e m b e r 2 3, 2 0 1 4 Overview 2 Overview of NSF OIG Office of Audit Overview of Federal financial assistance in the U.S.

NSF OIG Audit Update 1 NORTHEAST CONFERENCE ON COLLEGE COST ACCOUNTING S e p t e m b e r 2 3, 2 0 1 4 Overview 2 Overview of NSF OIG Office of Audit Overview of Federal financial assistance in the U.S.

State of Louisiana Disaster Recovery Unit. CDBG-DR Economic Development Programs

State of Louisiana Disaster Recovery Unit CDBG-DR Economic Development Programs Agenda Louisiana Hurricanes: An Overview To engage or not to engage a subrecipient? Pros and Cons Programmatic Design and

State of Louisiana Disaster Recovery Unit CDBG-DR Economic Development Programs Agenda Louisiana Hurricanes: An Overview To engage or not to engage a subrecipient? Pros and Cons Programmatic Design and

Uniform Guidance - Lessons Learned And To Be Learned

DAY MAY 23, 2017 3:35-4:50PM Uniform Guidance - Lessons Learned And To Be Learned MODERATOR Jerry E. Durham Assistant Director for Research and Compliance, Tennessee Comptroller of the Treasury SPEAKERS

DAY MAY 23, 2017 3:35-4:50PM Uniform Guidance - Lessons Learned And To Be Learned MODERATOR Jerry E. Durham Assistant Director for Research and Compliance, Tennessee Comptroller of the Treasury SPEAKERS

Procurement 101: Developing a Code of Conduct and. Written Procurement Procedures

Procurement 101: Developing a Code of Conduct and Written Procurement Procedures Presented by: Laurie Pennings, MS, RD Courtney Hardoin, MS, RD Nutrition Education Consultants California Department of

Procurement 101: Developing a Code of Conduct and Written Procurement Procedures Presented by: Laurie Pennings, MS, RD Courtney Hardoin, MS, RD Nutrition Education Consultants California Department of

The Federal government places many requirements on the entities that seek

OFFICE OF MANAGEMENT AND BUDGET ISSUES THE SUPERCIRCULAR : UNIFORM GUIDANCE ON COST PRINCIPLES, AUDIT, AND ADMINISTRATIVE REQUIREMENTS FOR FEDERAL AWARDS Rachel Conway, Director of Contracts, Save the

OFFICE OF MANAGEMENT AND BUDGET ISSUES THE SUPERCIRCULAR : UNIFORM GUIDANCE ON COST PRINCIPLES, AUDIT, AND ADMINISTRATIVE REQUIREMENTS FOR FEDERAL AWARDS Rachel Conway, Director of Contracts, Save the

Jason Galloway, Associate Controller HSC Contract and Grant Accounting

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

AESA Members FROM: Noelle Ellerson Ng, Director Federal Advocacy DATE: February 13, 2018 AESA Response to President Trump s Proposed FY18 Budget

TO: AESA Members FROM: Noelle Ellerson Ng, Director Federal Advocacy DATE: February 13, 2018 RE: AESA Response to President Trump s Proposed FY18 Budget Overview Money talks, and how you allocate money

TO: AESA Members FROM: Noelle Ellerson Ng, Director Federal Advocacy DATE: February 13, 2018 RE: AESA Response to President Trump s Proposed FY18 Budget Overview Money talks, and how you allocate money

Building Your Foundation: Administrative Requirements Boot Camp (Modules 1-8: Administrative Requirements for Non-Federal Entities)

") Course #400 Syllabus Grant Management Boot Camp (Covers 12 Grant Management Modules) This Boot Camp bundle includes 12 Grants Management training courses including 8 modules on the Administrative Requirements

Course #400 Syllabus Grant Management Boot Camp (Covers 12 Grant Management Modules) This Boot Camp bundle includes 12 Grants Management training courses including 8 modules on the Administrative Requirements

How to Use CDBG for Public Service Activities

How to Use CDBG for Public Service Activities Introduction to Public Service Activities In this module we will show you how to build an effective public services program to maximize the positive impacts

How to Use CDBG for Public Service Activities Introduction to Public Service Activities In this module we will show you how to build an effective public services program to maximize the positive impacts