Federal Grants Administration Updates. Erin Auerbach Esq. Brustein & Manasevit, PLLC

|

|

|

- Sharon George

- 5 years ago

- Views:

Transcription

1 Federal Grants Administration Updates Erin Auerbach Esq. Brustein & Manasevit, PLLC 1

2 Agenda Perkins Reauthorization Workforce Investment Opportunity Act (WIOA) Navigating the New EDGAR Education Department General Administrative Regulations (EDGAR) Uniform Grants Guidance (UGG) 2

3 Perkins Reauthorization 3

4 Reauthorization 1.VEA of VEA Amendments of VEA Amendments of Perkins Act Perkins II Perkins III Perkins IV

5 Perkins IV GEPA Section 414 Contingent Extension of Programs 5

6 Where Does Perkins Stand In Reauthorization Pipeline? In the Senate #3 In The House #2 6

7 Senate Consideration of ESEA #1 Bipartisan Every Child Achieves Act of 2015 Reduces Federal footprint Common Core 7

8 Senate Priority #2 Higher Education Act One or Two Bills? Program/Financial Aid 8

9 House Priority #1 - ESEA President would veto current House bill Student Success Act HR5 Portability Lack of full Republican support No Democratic support 9

10 House Priority #2 - Perkins Chairman Kline House will align CTE program with industry demands 10

11 Currently no CTE hearings scheduled for the fall Highly Unlikely to Have Perkins V on President s Desk This Year 11

12 But Remember the Bipartisan Effort on WIOA Last Year 12

13 Perkins V Most Likely Reauthorized in 2016 with a 07/01/2017 Effective Date 13

14 What Will Perkins V Look Like? No major overhaul Not contentious as ESEA/HEA Align with WIOA DOL Role on Perkins Postsecondary?? 14

15 What Happened to OCTAE Blueprint?? Competitive funding vs formula Consortia funding Private industry match Innovation fund ($200 million) Programs of study 15

16 Perkins Funding Essentially flat for 20 years Elimination of Tech Prep in 2010 Sequester enacted in 2011 FY 13 cuts CRomnibus 07/01/ /01/2016 Approximate 1% cut due to sequester (?) 16

17 What you need to know about the WIOA 17

18 Navigating the New EDGAR 18

19 EDGAR Old Friend, New Look 19

20 Key Parts of EDGAR Title 34 Part 75 Direct Grant Programs Part 76 State-Administered Programs Part 77 Definitions Part 81 Enforcement Title 2 Part 200 Cost/Administrative/Audit Rules 20

21 Effective dates for 2 CFR Part 200 December 26, 2014 Direct Grants from ED July 1, 2015 State Administered Programs July 1, 2016 Procurement Rules One Year Grace Period Indirect Cost Rates When Due For Renegotiation 21

22 Adoption of 2 CFR Part Federal Register ED Adopts OMB Guidance in 2 CFR Part 200 except for: 1) 2 CFR (a) 2) 2 CFR (a) 22

23 Exception to 2 CFR (a) Authority for granting exceptions to regulations vested in OMB But Department of Education Organization Act 20 U.S.C does not permit Secretary to delegate exceptions to OMB. Secretary will consult within OMB. 23

24 Clarification to 2 CFR High Risk Status The Secretary retains the authority under and to impose high risk conditions on individual grants and individual grantees at time award is made or after an award is made. 24

25 Roadmap of Part 76 State-Administered Programs 25

The general principles to be used in")

26 Allowable Costs (page 55) The general principles to be used in determining costs applicable to grants is 2 CFR Part 200 Subpart E Prohibited: Use of funds for religion Real property and construction (unless authorized)

27 Cash Management Cash Advance Payment Process Obligation Liquidation Drawdown Payment This would be switched in a Reimbursement Payment Process. Obligation = Means orders placed for property and services, contracts and subawards made and similar transactions during a given period that require payment during the same or a future period

28 When Obligations Are Made (Page 66) Type of Obligation Acquisition of Property Personal Services by Employee Personal Services by Contractor Travel Approved Pre- Agreement Cost When Obligation Occurs Date of binding written commitment When services are performed Date of binding written commitment When travel is taken On the first day of the grant or subgrant performance period. 28

Grantees and subgrantees may begin to obligate funds when: When the awarding agency")

29 When May Begin to Obligate Formula Grants: (Page66) Grantees and subgrantees may begin to obligate funds when: When the awarding agency approves application; or Awarding agency determines application is substantially approvable Reimbursement subject to final approval. Discretionary Grants: When subgrant is made. However, pre-agreement costs are permissible (reference to 2 CFR Part 200) 29

30 Obligations During Carryover (Page 67) Funds may be obligated during the carryover period of one additional fiscal year. Tydings Amendment Allows extra year to obligate funds Does not apply to all grants Under Tydings, funds are available for months: months under the grant award (July 1, 2014 September 30, 2015) Plus 12 months (carryover period) (October 1, 2015 September 30, 2016) * Tydings is not applicable to Perkins subgrants. 30

31 The New 2 CFR Part 200 (Starts on Page 91) Subpart A Definitions Subpart B General Provisions Subpart C Pre Award Requirements Subpart D Post Award Requirements Subpart E Cost Principles Subpart F Audit Requirements 31

32 Financial Management Controls The Key Component to Federal Grants 32

33 The more attention paid to financial management controls, fewer headaches down the road!!! 33

34 WHY?? All oversight will examine financial management controls: 1) OIG Audit 2) Single Audit 3) Federal Program Monitoring 4) Pass Through Monitoring 34

35 Seven Key Elements of Financial Management 2 CFR (b) (Page 118) 1. Identification of Awards (NEW) 2. Financial Reporting 3. Accounting Records (Source Docs) 4. Internal Control 5. Budget Control 6. Written Cash Management Procedures (NEW) 7. Written Allowability Procedures (NEW) 35

36 1) Identification of Awards (New) All federal awards received and expended The name of the federal program Identification # of award CFDA Title and Number Federal Award I.D. # Fiscal Year of Award Federal Agency Pass-Through (If S/A) 36

37 2) Financial Reporting New shift to OMB approved performance metrics 37

38 2) Financial Reporting (cont.) Generally requires accurate, current, complete disclosure of financial results of each award NEW: (Page 134) Federal awarding agency can only collect OMB approved data elements, no less than annually, no more than quarterly NEW: (Page 134) Non federal entity must submit performance reports at intervals required by federal agency or pass through. Annual performance reports due 90 days after reporting period; Quarterly performance reports due 30 days after reporting period 38

39 2) Financial Reporting (cont.) NEW Performance Metrics: 1. Compare actual accomplishments to objectives. (quantify to extent possible) 2. Reasons goals were not met if appropriate 3. Additional pertinent information (e.g. analysis and explanation of cost overruns, high unit costs) (b)(2) 39

40 2) Financial Reporting (cont.) 4. Significant developments a. Problems, delays. Adverse conditions that would impair ability to meet objective of the award b. Favorable developments. Finishing sooner or at less cost (d) 40

41 3) Accounting Records (Source Documentation) Source Documentation Must Be Kept On: 1. Federal Awards 2. Authorizations 3. Obligations 4. Unobligated balances 5. Assets 6. Expenditures 7. Income 8. Interest (New) (Eliminated liabilities) 41

42 4) Internal Controls Effective control over and accountability for: 1. All funds 2. Property 3. Other assets Must adequately safeguard all assets Use assets solely for authorized purpose 42

43 5) Budget Control Comparison of expenditures with budget amounts for each award 43

44 6) Written Cash Management Procedures (6) NEW: Written Procedures to implement the requirements of

45 Payment (a) and (b) (Page 119) For states, payments are governed by Treasury State CMIA agreements 31 CFR Part 205 No Change For all other non federal entities, payments must minimize time elapsing between draw from G-5 and disbursement (not obligation) 45

46 Payment (cont.) (b)(1)-(4) (Page ) Written procedures must describe whether non-federal entity uses: 1) Advance Payments (preferred) Limited to minimum amounts needed to meet immediate cash needs 2) Reimbursement Pass through must make payment within 30 calendar days after receipt of the billing 3) Working Capital Advance The pass through determines that the nonfederal entity lacks sufficient working capital. Allows advance payment to cover estimated disbursement needs for initial period 46

47 Payment (cont.) (b)(7)-(8) (Page 121) NEW: Advances must be maintained in insured accounts NEW: Pass through cannot require separate depository accounts NEW: Accounts must be interest bearing unless: Aggregate federal awards under $120,000 Account not expected to earn in excess of $500 per year Bank require minimum balance so high, that such account not feasible A foreign gov t or banking system prohibits or precludes interest bearing accounts. 47

48 Payment (cont.) (b)(9) NEW: Interest amounts up to $500 may be retained by non federal entity for administrative purposes NEW: Interest earned must be remitted annually to HHS Payment Management System. 48

49 7) Written Allowability Procedures NEW: Written procedures for determining allowability of costs in accordance with Subpart E Cost Principles 49

50 7) Written Allowability Procedures (Cont.) Procedures can not simply restate the Uniform Guidance Subpart E Should explain the process used throughout the grant development and budget process Training tool and guide for employees 50

51 Program Income (Page 123) Non-Federal entities are encouraged to earn income to defray program costs where appropriate. Costs of generating program income may only be deducted if: Authorized by federal regulations or the Federal award; Costs are incidental and not charged to the Federal award. Property from the sale of real property or equipment is not program income apply post award property rules. Generally, IHEs MUST add program income to the federal award. 51

52 Subpart E Cost Principles 52

53 Cost Principles: Factors Affecting Allowability of Costs (Page 143) All Costs Must Be: 1. Necessary, Reasonable and Allocable 2. Conform with federal law & grant terms 3. Consistent with state and local policies 4. Consistently treated 5. In accordance with GAAP 6. Not included as match 7. Net of applicable credits (moved to ) 8. Adequately documented 53

54 Prior Written Approval (Page 144) NEW: In order to avoid subsequent disallowance: Non-Federal entity may seek prior written approval of cognizant agency (for indirect cost rate) or Federal awarding agency in advance of the incurrence of special or unusual costs 54

55 Direct v. Indirect Costs (Page 146) NEW: Salaries of administrative and clerical staff should be treated as indirect unless all of following are met: 1. Such services are integral to the activity 2. Individuals can be specifically identified with the activity 3. Such costs are explicitly included in the budget 4. Costs not also recovered as indirect 55

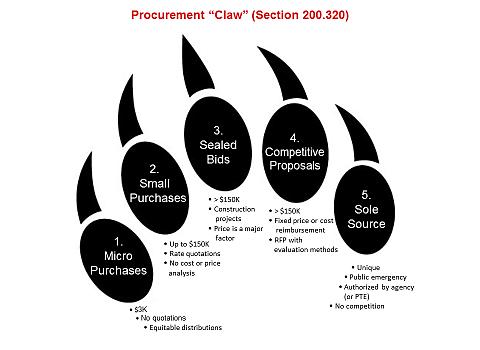

56 New: Required certifications (Page 148) NEW: Official authorized to legally bind the non-federal entity must certify on annual and final fiscal reports or vouchers requesting payment: By signing this report, I certify to the best of my knowledge and belief that the report is true, complete and accurate and the expenditures, disbursements and cash receipts are for the purposes and objectives set forth in the terms and conditions of the federal award. I am aware that any false, fictitious, or fraudulent information or the omission of any material fact, may subject me to criminal civil or administrative penalties for fraud, false statements, false claims, or otherwise. 56

57 Selected Items of Cost The UGG now has 55 specific items of cost! (Starting on Page 150) 57

58 Selected Items of Cost (cont.) Conferences (Page 158) (Changed) Prior Rule: Generally allowable Conference is meeting, seminar, workshop, event for the purpose of disseminating technical info beyond the nonfederal entity (?) Allowable conference costs include rental of facilities, speaker fees, meals and refreshments, and transportation, unless restricted by the federal award New: Costs related to identifying, but not providing, locally available dependent-care resources New: But travel allows costs for above and beyond regular dependent care Conference hosts must exercise discretion in ensuring costs are appropriate, necessary and managed in manner than minimizes costs to federal award ED Guidance re: Conferences and Meetings (Page 279) 58

59 Selected Items of Cost (cont.) Travel Costs (Page 176) (Changed) Prior rule: allowable with certain restrictions Travel costs may be charged on actual, per diem, or mileage basis Travel charges must be reasonable and consistent with entity s written travel reimbursement policies Grantee must retain documentation that participation of individual in conference is necessary for the project New: Dependent care costs above and beyond regular dependent care that directly result from travel to conferences may be allowable (consistent with written policy) 59

60 OMB Circulars Time and Effort Rule New Name: Time Distribution Records Standards for Documentation of Personnel Expenses If federal funds are used for salaries, then time distribution records are required. How staff demonstrate allocability Paid in whole or in part with federal funds (i)(1) Used to meet a match/cost share requirement (i)(4) 60

61 Cost Objectives (Page 98) What is a cost objective? (slightly changed) Program, function, activity, award, organizational subdivision, contract, or work unit for which cost data are desired and for which provision is made to accumulate and measure the cost of processes, products, jobs, capital projects, etc. 61

62 Standards for Documentation of Personnel Expenses (Page 152) NEW: Charges for salaries must be based on records that accurately reflect the work performed 1. Must be supported by a system of internal controls which provides reasonable assurance charges are accurate, allowable and properly allocated 2. Be incorporated into official records 3. Reasonably reflect total activity for which employee is compensated Not to exceed 100% 62

63 Standards for Documentation of Personnel Expenses (cont.) 4. Encompass all activities (federal and non-federal) 5. Comply with established accounting polices and practices 6. Support distribution among specific activities or cost objectives 63

64 Procurement 64

65 Procurement Standards (Page 129) NEW: All nonfederal entities must have documented procurement procedures which reflect applicable Federal, State, and local laws and regulations. Applies to grant and subgrant funds (passthrough funds). 65

66 Vendor Selection Process (Page 131) Method of procurement: NEW: Micro-purchase Small purchase procedures Competitive sealed bids Competitive proposals Noncompetitive proposals 66

67 67

68 Vendor Selection Process: Micro-Purchase (a) NEW: Acquisition of supplies and services under $3,000 or less. Threshold increases to $3,500 on October 1, May be awarded without soliciting competitive quotations if nonfederal entity considers the cost reasonable. To the extent practicable must distribute micro-purchases equitably among qualified suppliers. 68

69 Vendor Selection Process: Noncompetitive Proposals Appropriate only when: The good or services is available only from a single source (sole source) There is a public emergency The awarding agency authorizes NEW: awarding agency or pass-through must expressly authorize noncompetitive proposals in response to written requires from nonfederal entity (f)(3) After soliciting a number of sources, competition is deemed inadequate 69

70 Property Management 70

71 Inventory Management Must have adequate controls in place to account for: Location of equipment Custody of equipment Security of equipment 71

72 Equipment Defined (Page 99) Significant changes on use and dispositions ( ) (Page 127) Shared use allowed if use will not interfere Clarified: shared use priorities: (1) projects supported by same federal awarding agency; (2) projects funded by other federal agencies; (3) nonfederal programs New: may trade in when acquiring replacement equipment without recourse federal agency 72

73 Supplies (Page 106) Anything that is not equipment is considered supplies. Significant Technological Devices NEW: Computing devices Machines used to acquire, store, analyze, process, public data and other information electronically Includes accessories for printing, transmitting and receiving or storing electronic information Computing devices are supplies if less than $5,000 73

74 Internal Controls (b)(4) (Page 119) Regardless of cost, grantee must maintain effective control and safeguard all assets and assure that they are used solely for authorized purposes. 74

75 Disposition of Equipment (e) (Page 127) When property is no longer needed in any current or previously Federallyfunded supported activity, must follow disposition rules: NEW: Nonfederal entity must request disposition instructions from the federal awarding agency if required by the terms of the grant. Otherwise, may be retained, sold or otherwise disposed as follows: Over $5,000 pay federal share If equipment is sold: Federal awarding agency may permit non-federal entity to deduct and retain $500 or 10% of the proceeds for selling and handling instructions. Under $5,000 no accountability (still must formally dispose) 75

76 Disposition of Supplies (Page 128) If there is a residual inventory of unused supplies exceeding $5,000 in total aggregate value upon termination or completion of the project or program and the supplies are not needed for any other federal award, must compensate the federal government for its share. 76

77 Records and Reviews 77

78 Methods for collection, Transmission and storage of information (Page 138) o NEW: When original records are electronic and cannot be altered, there is no need to create and retain paper copies. o When original records are paper, electronic versions may be substituted through the use of duplication or other forms of electronic media provided they: o Are subject to periodic quality control reviews, o Provide reasonable safeguards against alteration; and o Remain readable. 78

79 Requirements of pass-through entities 79

80 Federal awarding agency review of risk posed by applicants NEW: Fed Agency and Pass-Through ( (b)) must have in place a framework for evaluating risks before applicant receives funding 1. Financial Stability 2. Quality of Management System 3. History of Performance 4. Audit Reports 5. Applicant s Ability to Effectively Implement Program 80

81 Specific Conditions (Page 116) Fed agency or Pass Through may impose additional Federal award conditions : Require reimbursement; Withhold funds until evidence of acceptable performance; More detailed reporting Additional monitoring; Require grantee to obtain technical or management assistance; or Establish additional prior approvals. 81

82 Requirements for pass-through Entities (Page 136) Pass-through must monitor its subrecipients to assure compliance and performance goals are achieved Monitoring must include: 1. Review financial and programmatic reports 2. Ensure corrective action 3. Issue a management decision on audit findings if the award is from the pass-through 82

83 Requirements for pass-through Entities NEW: Depending on assessment of risk, the following monitoring tools may be useful for the pass-through entity to ensure proper accountability and compliance with program requirements and achievement of performance goals: 1. Training + technical assistance on program-related matters 2. On-site reviews 3. Arranging for agreed-upon-procedures engagements (described in ) 83

84 Requirements for pass-through Entities Pass-through must consider taking enforcement action ( ) based on non compliance: 1. Temporarily withhold cash payments pending correction 2. Disallow all or part of the cost 3. Wholly or partly suspend the award 4. Recommend to federal awarding agency suspension / debarment 5. Withhold further federal awards 6. Other remedies that may be legally available 84

85 Audit Requirements 85

86 Audit requirements Current threshold $500,000. NEW: Threshold increased to $750,000 (Page 117) The federal agency, OIG, or GAO may arrange for audits in addition to single audit 86

87 QUESTIONS? 87

88 ~ Legal Disclaimer ~ This presentation is intended solely to provide general information and does not constitute legal advice. Attendance at the presentation or later review of these printed materials does not create an attorney-client relationship with Brustein & Manasevit. You should not take any action based upon any information in this presentation without first consulting legal counsel familiar with your particular circumstances. 88

Overview of the New EDGAR (formerly the Uniform Grants Guidance)

") Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Regulations Governing The Perkins CTE Program KBOR Summer Conference June 11, 2015

Regulations Governing The Perkins CTE Program KBOR Summer Conference June 11, 2015 MICHAEL BRUSTEIN, ESQ. MBRUSTEIN@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM AGENDA Comments on Reauthorization

Regulations Governing The Perkins CTE Program KBOR Summer Conference June 11, 2015 MICHAEL BRUSTEIN, ESQ. MBRUSTEIN@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM AGENDA Comments on Reauthorization

Uniform Grants Guidance. Colorado Charter School Institute Cassie Walgren, Controller

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

TEA Implementation of the New EDGAR

Implementation of the New EDGAR Office for Grants and Federal Fiscal Compliance Texas Education Agency ESC Cluster Site Implementation Training 2015 by the Texas Education Agency Agenda Introduction Written

Implementation of the New EDGAR Office for Grants and Federal Fiscal Compliance Texas Education Agency ESC Cluster Site Implementation Training 2015 by the Texas Education Agency Agenda Introduction Written

How to Draft New & Update Old Policies and Procedures. Agenda. Why?

How to Draft New & Update Old Policies and Procedures Brette Kaplan Wurzburg bwurzbrug@bruman.com Jennifer Segal jsegal@bruman.com Fall Forum 2014 Agenda Why policies and procedures are important? Logistics

How to Draft New & Update Old Policies and Procedures Brette Kaplan Wurzburg bwurzbrug@bruman.com Jennifer Segal jsegal@bruman.com Fall Forum 2014 Agenda Why policies and procedures are important? Logistics

AGENDA. Subrecipient Monitoring Under the New Uniform Guidance. What is a passthrough

Subrecipient Monitoring Under the New Uniform Guidance Steven A. Spillan, Esq. sspillan@bruman.com Spring Forum 2015 AGENDA What is a pass through entity? How a does a pass through entity s responsibilities

Subrecipient Monitoring Under the New Uniform Guidance Steven A. Spillan, Esq. sspillan@bruman.com Spring Forum 2015 AGENDA What is a pass through entity? How a does a pass through entity s responsibilities

Presenter. Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance

The New OMB Uniform Guidance") Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance Presenter Richard Cunningham Quality Assurance & Technical Specialist Center

Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance Presenter Richard Cunningham Quality Assurance & Technical Specialist Center

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

TIME AND EFFORT DOCUMENTATION 101 TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR EDGAR AND THE OMB CIRCULARS

TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR TIFFANY R. WINTERS, ESQ. TWINTERS@BRUMAN.COM @TRWINTERS BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NASTID 2014 1

TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR TIFFANY R. WINTERS, ESQ. TWINTERS@BRUMAN.COM @TRWINTERS BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NASTID 2014 1

Uniform Guidance Sponsored Projects Services

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Roadmap to the Uniform Grant Guidance for School Districts

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

Texas Education Agency. Division of Federal Fiscal Monitoring

Texas Education Agency Division of Federal Fiscal Monitoring The DO s and DON Ts of Administering Federal Grants Copyright 2016 by TEA DO s and DON'Ts of Administering Federal Grants Division of Federal

Texas Education Agency Division of Federal Fiscal Monitoring The DO s and DON Ts of Administering Federal Grants Copyright 2016 by TEA DO s and DON'Ts of Administering Federal Grants Division of Federal

Policies and Procedures Under the Uniform Grant Guidance. Florida School Finance Officers Association November 10, 2016

Policies and Procedures Under the Uniform Grant Guidance Florida School Finance Officers Association November 10, 2016 Why? Single Audits Monitoring Staff Changes and Transitions New EDGAR requirements

Policies and Procedures Under the Uniform Grant Guidance Florida School Finance Officers Association November 10, 2016 Why? Single Audits Monitoring Staff Changes and Transitions New EDGAR requirements

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews Denise Dusek, MPA Federal Funding Specialist ESC 20 Image obtained from google.com Education Service Center, Region 20 May 2018 2 1 Participants

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews Denise Dusek, MPA Federal Funding Specialist ESC 20 Image obtained from google.com Education Service Center, Region 20 May 2018 2 1 Participants

Uniform Guidance Subpart D Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Department of Contracts, Grants and Financial Administration, Texas Education Agency 1/26/18

Federal Grant Procurement Rules and Regulations and Federal Fiscal Monitoring Requirements Cory Green, Associate Commissioner Department of Contracts, Grants and Financial Administration Texas January

Federal Grant Procurement Rules and Regulations and Federal Fiscal Monitoring Requirements Cory Green, Associate Commissioner Department of Contracts, Grants and Financial Administration Texas January

Federal Rules for Sponsored Programs. Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

NEW EDGAR REGULATIONS

NEW EDGAR REGULATIONS FREQUENTLY ASKED QUESTIONS (FAQ): PRELIMINARY GUIDANCE APPLICABLE TO ALL FEDERALLY FUNDED GRANT PROGRAMS ADMINISTERED BY THE TEXAS EDUCATION AGENCY Blue text identifies changes, updates,

NEW EDGAR REGULATIONS FREQUENTLY ASKED QUESTIONS (FAQ): PRELIMINARY GUIDANCE APPLICABLE TO ALL FEDERALLY FUNDED GRANT PROGRAMS ADMINISTERED BY THE TEXAS EDUCATION AGENCY Blue text identifies changes, updates,

Uniform Guidance Subpart D Administrative Requirements. Why This Session Is Needed. Lesson Overview & Module Objectives

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN

TO 2 CFR 200 (UNIFORM ADMIN") Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

10 CFR 600: KNOW YOUR REQUIREMENTS

WEATHERIZATION ASSISTANCE PROGRAM 10 CFR 600: KNOW YOUR REQUIREMENTS Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and

WEATHERIZATION ASSISTANCE PROGRAM 10 CFR 600: KNOW YOUR REQUIREMENTS Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and

NEW EDGAR REGULATIONS

NEW EDGAR REGULATIONS FREQUENTLY ASKED QUESTIONS (FAQ): PRELIMINARY GUIDANCE APPLICABLE TO ALL FEDERALLY FUNDED GRANT PROGRAMS ADMINISTERED BY THE TEXAS EDUCATION AGENCY Blue text identifies changes, updates,

NEW EDGAR REGULATIONS FREQUENTLY ASKED QUESTIONS (FAQ): PRELIMINARY GUIDANCE APPLICABLE TO ALL FEDERALLY FUNDED GRANT PROGRAMS ADMINISTERED BY THE TEXAS EDUCATION AGENCY Blue text identifies changes, updates,

The OmniCircular - 2 CFR 200

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT INTRODUCTION BACKGROUND On December 26, 2013, the Office of

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT INTRODUCTION BACKGROUND On December 26, 2013, the Office of

Single Audit Entrance Conference Uniform Guidance Refresher

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

EDGAR and Procurement CHOICE PARTNERS OCTOBER 12, 2016

EDGAR and Procurement CHOICE PARTNERS OCTOBER 12, 2016 Agenda Uniform Guidance Summary (Note: EDGAR for educational entities) General Federal Procurement Laws Thresholds and Implications Sole Source Vendors

EDGAR and Procurement CHOICE PARTNERS OCTOBER 12, 2016 Agenda Uniform Guidance Summary (Note: EDGAR for educational entities) General Federal Procurement Laws Thresholds and Implications Sole Source Vendors

HAVA GRANTS AND MONITORING. Presented by: Dan Glotzer, Election Funds Manager and Venessa Miller, HAVA Grant Monitor

HAVA GRANTS AND MONITORING Presented by: Dan Glotzer, Election Funds Manager and Venessa Miller, HAVA Grant Monitor Overview of the Help America Vote Act (HAVA) Grants Types of Grants Benefit Periods Program

HAVA GRANTS AND MONITORING Presented by: Dan Glotzer, Election Funds Manager and Venessa Miller, HAVA Grant Monitor Overview of the Help America Vote Act (HAVA) Grants Types of Grants Benefit Periods Program

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS. National Historical Publications and Records Commission

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS Agenda Uniform Guidance Summary General Federal Procurement Laws Thresholds and Implications Sole Source Vendors Cooperative Purchasing

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS Agenda Uniform Guidance Summary General Federal Procurement Laws Thresholds and Implications Sole Source Vendors Cooperative Purchasing

What EDGAR Is and What ESSA Will Bring! Tiffany R. Winters, Esq. Brustein & Manasevit June 2016

What EDGAR Is and What ESSA Will Bring! Tiffany R. Winters, Esq. Brustein & Manasevit www.bruman.com June 2016 1 From April Sept 2016 the ED OIG has secured approx. $50 Million in settlements, fines, restitutions,

What EDGAR Is and What ESSA Will Bring! Tiffany R. Winters, Esq. Brustein & Manasevit www.bruman.com June 2016 1 From April Sept 2016 the ED OIG has secured approx. $50 Million in settlements, fines, restitutions,

PROCUREMENT POLICY FOR FEDERAL GRANTS

PROCUREMENT POLICY FOR FEDERAL GRANTS I. Introduction This Procurement Policy for Federal Grants applies to all expenditures of monies received through federal grants, whether those monies come directly

PROCUREMENT POLICY FOR FEDERAL GRANTS I. Introduction This Procurement Policy for Federal Grants applies to all expenditures of monies received through federal grants, whether those monies come directly

General Procurement Requirements

Effective Date: July 1, 2018 Applicability: Grant Purchasing and Procurement Policy Related Policies: Moravian College Purchasing Policy and Business Travel Policy Policy: This policy provides guidelines

Effective Date: July 1, 2018 Applicability: Grant Purchasing and Procurement Policy Related Policies: Moravian College Purchasing Policy and Business Travel Policy Policy: This policy provides guidelines

ATTACHMENTS A & B GRANT AGREEMENT TERMS AND CONDITIONS DEPARTMENT OF EDUCATION

ATTACHMENTS A & B GRANT AGREEMENT TERMS AND CONDITIONS DEPARTMENT OF EDUCATION I. COMPLIANCE WITH APPLICABLE LAWS The Grantee shall, at all times, comply with all federal, state and local laws, ordinances

ATTACHMENTS A & B GRANT AGREEMENT TERMS AND CONDITIONS DEPARTMENT OF EDUCATION I. COMPLIANCE WITH APPLICABLE LAWS The Grantee shall, at all times, comply with all federal, state and local laws, ordinances

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT. July 1, 2017 June 30, 2018

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT July 1, 2017 June 30, 2018 This Grant Agreement (the Agreement ) is entered into by and between the Family and Children First Administrative Agency

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT July 1, 2017 June 30, 2018 This Grant Agreement (the Agreement ) is entered into by and between the Family and Children First Administrative Agency

Grants to States for Low-Income Housing Projects in Lieu of Low-Income Housing Credits for 2009 GRANTEE TERMS AND CONDITIONS

Grants to States for Low-Income Housing Projects in Lieu of Low-Income Housing Credits for 2009 GRANTEE TERMS AND CONDITIONS 1. Authority a. Section 1602 of the American Recovery and Reinvestment Tax Act

Grants to States for Low-Income Housing Projects in Lieu of Low-Income Housing Credits for 2009 GRANTEE TERMS AND CONDITIONS 1. Authority a. Section 1602 of the American Recovery and Reinvestment Tax Act

Federal Grant Guidance Compliance

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

WHAT LAWS APPLY TO FEDERAL GRANTS: A HISTORICAL PERSPECTIVE

WHAT LAWS APPLY TO FEDERAL GRANTS: A HISTORICAL PERSPECTIVE LEIGH M. MANASEVIT, ESQ. LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM SPRING FORUM 2013 1 1960s: Congress began recognizing

WHAT LAWS APPLY TO FEDERAL GRANTS: A HISTORICAL PERSPECTIVE LEIGH M. MANASEVIT, ESQ. LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM SPRING FORUM 2013 1 1960s: Congress began recognizing

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT)

") GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

Administrative Regulation SANGER UNIFIED SCHOOL DISTRICT. Business and Noninstructional Operations FEDERAL GRANT FUNDS

Administrative Regulation SANGER UNIFIED SCHOOL DISTRICT AR 3230(a) Business and Noninstructional Operations FEDERAL GRANT FUNDS Allowable Costs Prior to obligating or spending any federal grant funds,

Administrative Regulation SANGER UNIFIED SCHOOL DISTRICT AR 3230(a) Business and Noninstructional Operations FEDERAL GRANT FUNDS Allowable Costs Prior to obligating or spending any federal grant funds,

Grants Management Scenarios

Grants Management Scenarios SCENARIO 1: Parker School District received a TIF grant in 2012. It followed the guidelines set forth in the application package and did not list specific vendors in its application.

Grants Management Scenarios SCENARIO 1: Parker School District received a TIF grant in 2012. It followed the guidelines set forth in the application package and did not list specific vendors in its application.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

CHAPTER 10 Grant Management

CHAPTER 10 Grant Management Table of Contents Page GRANT MANAGEMENT 1 Introduction... 1 Financial Management of Grants... 1 Planning and Budgeting... 1 Application and Implementation... 2 Monitoring...

CHAPTER 10 Grant Management Table of Contents Page GRANT MANAGEMENT 1 Introduction... 1 Financial Management of Grants... 1 Planning and Budgeting... 1 Application and Implementation... 2 Monitoring...

MONTGOMERY COUNTY INTERMEDIATE UNIT #23

No. 626 MONTGOMERY COUNTY INTERMEDIATE UNIT #23 SECTION: TITLE: FINANCES FEDERAL FISCAL COMPLIANCE ADOPTED: June 22, 2016 REVISED: 626. FEDERAL FISCAL COMPLIANCE 1. Authority Part 200 2. Delegation of

No. 626 MONTGOMERY COUNTY INTERMEDIATE UNIT #23 SECTION: TITLE: FINANCES FEDERAL FISCAL COMPLIANCE ADOPTED: June 22, 2016 REVISED: 626. FEDERAL FISCAL COMPLIANCE 1. Authority Part 200 2. Delegation of

Dollars & Sense: Federal Grant Financial

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

December 26, 2014 NEW ADDITIONAL December 26, 2014 beginning December 26, /31/15, 6/30/16 Contents Reference Origin Appendix

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES)

") TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES) The Texas General Land Office Community Development & Revitalization

TEXAS GENERAL LAND OFFICE COMMUNITY DEVELOPMENT & REVITALIZATION PROCUREMENT GUIDANCE FOR SUBRECIPIENTS UNDER 2 CFR PART 200 (UNIFORM RULES) The Texas General Land Office Community Development & Revitalization

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY. Office of Contracts and Grants December, 2014

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

Effective July 1, 2015 Revised (October 2016)

") Lyford CISD Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and

Lyford CISD Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and

Uniform Guidance vs. OMB Circulars

Program Income Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements governing cost Designed for DOL-ETA direct principles, administrative recipients and their requirements and

Program Income Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements governing cost Designed for DOL-ETA direct principles, administrative recipients and their requirements and

2016 Compliance Supplement. Joe Bergene, CPA Altman, Rogers & Co.

2016 Compliance Supplement Joe Bergene, CPA Altman, Rogers & Co. Overview! Topics to be discussed:! Compliance supplement, what is it and why is it important to be familiar with it.! Overview of the supplement.!

2016 Compliance Supplement Joe Bergene, CPA Altman, Rogers & Co. Overview! Topics to be discussed:! Compliance supplement, what is it and why is it important to be familiar with it.! Overview of the supplement.!

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance)

") Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Felipe Lopez, Vavrinek, Trine, Day & Co., LLP

San Luis Obispo County Community College District & San Luis Obispo County Office of Education 2012 F d l C li T i i 2012 Federal Compliance Training Felipe Lopez, Vavrinek, Trine, Day & Co., LLP Objectives

San Luis Obispo County Community College District & San Luis Obispo County Office of Education 2012 F d l C li T i i 2012 Federal Compliance Training Felipe Lopez, Vavrinek, Trine, Day & Co., LLP Objectives

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT. July 1, 2018 June 30, 2019

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT July 1, 2018 June 30, 2019 This Grant Agreement (the Agreement ) is entered into by and between the Family and Children First Administrative Agency

EARLY INTERVENTION SERVICE COORDINATION GRANT AGREEMENT July 1, 2018 June 30, 2019 This Grant Agreement (the Agreement ) is entered into by and between the Family and Children First Administrative Agency

2 CFR PART 215--UNIFORM ADMINISTRATIVE REQUIREMENTS

2 CFR PART 215--UNIFORM ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH INSTITUTIONS OF HIGHER EDUCATION, HOSPITALS, AND OTHER NON-PROFIT ORGANIZATIONS (OMB CIRCULAR A-110) May 11, 2004 OFFICE

2 CFR PART 215--UNIFORM ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH INSTITUTIONS OF HIGHER EDUCATION, HOSPITALS, AND OTHER NON-PROFIT ORGANIZATIONS (OMB CIRCULAR A-110) May 11, 2004 OFFICE

PART 34-ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH FOR-PROFIT ORGANIZATIONS. Subpart A-General

PART 34-ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH FOR-PROFIT ORGANIZATIONS 34.1 Purpose. Subpart A-General (a) This part prescribes administrative requirements for awards to for-profit

PART 34-ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH FOR-PROFIT ORGANIZATIONS 34.1 Purpose. Subpart A-General (a) This part prescribes administrative requirements for awards to for-profit

Department of Defense Education Activity (DoDEA) DIVISION I: AWARD COVER PAGES

DIVISION I: AWARD COVER PAGES") DIVISION I: AWARD COVER PAGES Grant Number: (to be completed at the time of award) Type of award & Award Action: Grant New Award Total Grant Amount: (to be completed at the time of award) Obligation and

DIVISION I: AWARD COVER PAGES Grant Number: (to be completed at the time of award) Type of award & Award Action: Grant New Award Total Grant Amount: (to be completed at the time of award) Obligation and

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida

Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida") Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

The State of Texas HELP AMERICA VOTE ACT PROVIDE THE SAME OPPORTUNITY FOR ACCESS AND PARTICIPATION TO INDIVIDUALS WITH DISABILITIES

The State of Texas Elections Division Phone: 512-463-5650 P.O. Box 12060 Fax: 512-475-2811 Austin, Texas 78711-2060 TTY: 7-1-1 www.sos.state.tx.us (800) 252-VOTE (8683) The Office of The Secretary of State

The State of Texas Elections Division Phone: 512-463-5650 P.O. Box 12060 Fax: 512-475-2811 Austin, Texas 78711-2060 TTY: 7-1-1 www.sos.state.tx.us (800) 252-VOTE (8683) The Office of The Secretary of State

Seminar on Financial Management. VOCA s National Conference

Seminar on Financial Management VOCA s National Conference Financial Management Systems In summary, a Financial Management System must be able to: Record and report on the -- Receipt; Obligation; and Expenditure

Seminar on Financial Management VOCA s National Conference Financial Management Systems In summary, a Financial Management System must be able to: Record and report on the -- Receipt; Obligation; and Expenditure

WIOA SEC Administrative Provisions. Subparts: A - H. Presented by: 11/ 16/2016. Office of Grants Management

1 WIOA SEC. 683 Administrative Provisions Subparts: A - H Presented by: Office of Grants Management 11/ 16/2016 2 Today's Presenters Deborah Galloway Fiscal Policy Manager Division of Policy, Review &

1 WIOA SEC. 683 Administrative Provisions Subparts: A - H Presented by: Office of Grants Management 11/ 16/2016 2 Today's Presenters Deborah Galloway Fiscal Policy Manager Division of Policy, Review &

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees SHERYL L. STEPHENS BURKE, CPA, MST Nashua Office 102 Perimeter Road

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees SHERYL L. STEPHENS BURKE, CPA, MST Nashua Office 102 Perimeter Road

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. AUSPAN Martha Taylor

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Cohort 9 Grant Closeout Procedures HEIDI SCHULTZ DEBRA APPLETON JUNE 6, 2017

Cohort 9 Grant Closeout Procedures HEIDI SCHULTZ DEBRA APPLETON JUNE 6, 2017 Objectives To Provide direction and clarification on protocols and procedures to close out a 5 th year 21 st CCLC grant. 1.

Cohort 9 Grant Closeout Procedures HEIDI SCHULTZ DEBRA APPLETON JUNE 6, 2017 Objectives To Provide direction and clarification on protocols and procedures to close out a 5 th year 21 st CCLC grant. 1.

Texas Equal Access to Justice Foundation IOLTA GENERAL GRANT PROVISIONS SEPTEMBER 1998

Texas Equal Access to Justice Foundation IOLTA GENERAL GRANT PROVISIONS SEPTEMBER 1998 AMENDED 2004 TABLE OF CONTENTS Page ARTICLE I GENERAL 1 1.01 INTRODUCTION 1 1.02 DEFINITIONS 1 ARTICLE II GRANT PAYMENT

Texas Equal Access to Justice Foundation IOLTA GENERAL GRANT PROVISIONS SEPTEMBER 1998 AMENDED 2004 TABLE OF CONTENTS Page ARTICLE I GENERAL 1 1.01 INTRODUCTION 1 1.02 DEFINITIONS 1 ARTICLE II GRANT PAYMENT

Presented by: Jennifer Carrougher, Director of Federal Fiscal Policy Toni Bernethy, Director of Audit Resolution Annual Conference, Spokane WA

Presented by: Jennifer Carrougher, Director of Federal Fiscal Policy Toni Bernethy, Director of Audit Resolution 2017 Annual Conference, Spokane WA Agenda Federal Budget/ESSA Procurement/Suspension & Debarment

Presented by: Jennifer Carrougher, Director of Federal Fiscal Policy Toni Bernethy, Director of Audit Resolution 2017 Annual Conference, Spokane WA Agenda Federal Budget/ESSA Procurement/Suspension & Debarment

Something for Everyone: Adjusting to the OMB s Super Circular May 25, :30 10:10 am 2 CPE

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist 1 Learning Objectives Participants will gain an understanding of the elements of preaward and how to think through required

Grant Review and Pre-Award Process Elisa Gleeson Senior Grants Management Specialist 1 Learning Objectives Participants will gain an understanding of the elements of preaward and how to think through required

GRANTS MANAGEMENT HANDBOOK

GRANTS MANAGEMENT HANDBOOK Business Office CHEC Cindy Cammuse, Manager, Grant Accounting (972) 758-3864 (972) 758-3841 Fax Laura Henry, Accountant III-Grants and Contracts (972) 758-3828 Angela Chapman,

GRANTS MANAGEMENT HANDBOOK Business Office CHEC Cindy Cammuse, Manager, Grant Accounting (972) 758-3864 (972) 758-3841 Fax Laura Henry, Accountant III-Grants and Contracts (972) 758-3828 Angela Chapman,

RESEARCH TERMS AND CONDITIONS June, 2011

RESEARCH TERMS AND CONDITIONS June, 2011 TABLE OF CONTENTS Administrative Requirements I. GENERAL Article 1. Purpose. 2. Definitions 3. Reserved 4. Deviations 5. Subawards II. PREAWARD REQUIREMENTS 10.

RESEARCH TERMS AND CONDITIONS June, 2011 TABLE OF CONTENTS Administrative Requirements I. GENERAL Article 1. Purpose. 2. Definitions 3. Reserved 4. Deviations 5. Subawards II. PREAWARD REQUIREMENTS 10.

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Overview of Procurement September

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Overview of Procurement September

What were the Changes from the OMB Circulars to the Uniform Guidance Bag Lunch Webinar June 21, 2016

What were the Changes from the OMB Circulars to the Uniform Guidance Bag Lunch Webinar June 21, 2016 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

What were the Changes from the OMB Circulars to the Uniform Guidance Bag Lunch Webinar June 21, 2016 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

Federal Grant Policies and

Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and Education Department

Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and Education Department

Discretionary Grants Overview. Why This Session Is Needed. Lesson Overview & Module Objectives. Modifications: when, why, and how

Oversight and Monitoring 1 Why This Session Is Needed Prior approval requirements Ability to incur costs Modifications: when, why, and how Application to subrecipients Formula authority 2 Lesson Overview

Oversight and Monitoring 1 Why This Session Is Needed Prior approval requirements Ability to incur costs Modifications: when, why, and how Application to subrecipients Formula authority 2 Lesson Overview

ADMINISTRATION OF FEDERAL GRANT FUNDS

ADMINISTRATION OF FEDERAL GRANT FUNDS The Board accepts federal funds, which are available, provided that there is a specific need for them and that the required matching funds are available. The Board

ADMINISTRATION OF FEDERAL GRANT FUNDS The Board accepts federal funds, which are available, provided that there is a specific need for them and that the required matching funds are available. The Board

Are You Ready for This? The New Uniform Guidance 2 CFR 200

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

N O N-PR O FI T O R G A NI Z A T I O NS

FIN A N C I A L M A N A G E M E N T G UID E F O R N O N-PR O FI T O R G A NI Z A T I O NS N A T I O N A L E ND O W M E N T F O R T H E A R TS O F F I C E O F INSP E C T O R G E N E R A L SEP T E M B E

FIN A N C I A L M A N A G E M E N T G UID E F O R N O N-PR O FI T O R G A NI Z A T I O NS N A T I O N A L E ND O W M E N T F O R T H E A R TS O F F I C E O F INSP E C T O R G E N E R A L SEP T E M B E

Performance and Financial Monitoring and Reporting

2 CFR 200 Uniform Guidance Performance & Financial Monitoring / Reporting and Subrecipient Monitoring Kris Rhodes, Director MAXIMUS Performance and Financial Monitoring and Reporting 1 Financial Reporting

2 CFR 200 Uniform Guidance Performance & Financial Monitoring / Reporting and Subrecipient Monitoring Kris Rhodes, Director MAXIMUS Performance and Financial Monitoring and Reporting 1 Financial Reporting

Effective July 1, 2015 Revised (Date)

") Brownsville Independent School District Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements

Brownsville Independent School District Federal Grant Policies and Procedures Manual Pursuant to Requirements in 2 CFR Part 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements

MAXIMUS Higher Education Practice

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director, MAXIMUS Jason Guilbeault, Senior Consultant, MAXIMUS 1 MAXIMUS Higher Education Practice Headquartered in Northbrook,

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director, MAXIMUS Jason Guilbeault, Senior Consultant, MAXIMUS 1 MAXIMUS Higher Education Practice Headquartered in Northbrook,

Understanding and Complying with Government Grants

Presents... Understanding and Complying with Objectives Obtain information to determine if applying for governmental grants is appropriate for your organization Obtain understanding of internal controls

Presents... Understanding and Complying with Objectives Obtain information to determine if applying for governmental grants is appropriate for your organization Obtain understanding of internal controls

FISCAL YEAR FAMILY SELF-SUFFICIENCY PROGRAM GRANT AGREEMENT (Attachment to Form HUD-1044) ARTICLE I: BASIC GRANT INFORMATION AND REQUIREMENTS

ARTICLE I: BASIC GRANT INFORMATION AND REQUIREMENTS") 1 1 1 1 1 1 1 1 0 1 0 1 0 1 0 1 FISCAL YEAR 01 FAMILY SELF-SUFFICIENCY PROGRAM GRANT AGREEMENT (Attachment to Form HUD-) ARTICLE I: BASIC GRANT INFORMATION AND REQUIREMENTS 1. This Agreement is between

1 1 1 1 1 1 1 1 0 1 0 1 0 1 0 1 FISCAL YEAR 01 FAMILY SELF-SUFFICIENCY PROGRAM GRANT AGREEMENT (Attachment to Form HUD-) ARTICLE I: BASIC GRANT INFORMATION AND REQUIREMENTS 1. This Agreement is between

APRIL 2009 COMMUNITY DEVELOPMENT BLOCK GRANTS/STATE S PROGRAM NORTH CAROLINA SMALL CITIES CDBG AND NEIGHBORHOOD STABILIZATION PROGRAM

APRIL 2009 14.228 State Project/Program: Federal Authorization: State Authorization: COMMUNITY DEVELOPMENT BLOCK GRANTS/STATE S PROGRAM NORTH CAROLINA SMALL CITIES CDBG AND NEIGHBORHOOD STABILIZATION PROGRAM

APRIL 2009 14.228 State Project/Program: Federal Authorization: State Authorization: COMMUNITY DEVELOPMENT BLOCK GRANTS/STATE S PROGRAM NORTH CAROLINA SMALL CITIES CDBG AND NEIGHBORHOOD STABILIZATION PROGRAM

The Uniform Guidance (2 CFR, Part 200)

") WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards Frances Hodge Public Health Analyst, Southern Services Branch Division of Metropolitan

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards Frances Hodge Public Health Analyst, Southern Services Branch Division of Metropolitan

Trinity Valley Community College. Grants Accounting Policy and Procedures 2012

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

ALABAMA WORKFORCE INVESTMENT SYSTEM. Office of Workforce Development 401 Adams Avenue Post Office Box 5690 Montgomery, Alabama

ALABAMA WORKFORCE INVESTMENT SYSTEM Office of Workforce Development 401 Adams Avenue Post Office Box 5690 Montgomery, Alabama 36103-5690 GOVERNOR'S WORKFORCE DEVELOPMENT DIRECTIVE NO. PY2004-14 SUBJECT:

ALABAMA WORKFORCE INVESTMENT SYSTEM Office of Workforce Development 401 Adams Avenue Post Office Box 5690 Montgomery, Alabama 36103-5690 GOVERNOR'S WORKFORCE DEVELOPMENT DIRECTIVE NO. PY2004-14 SUBJECT:

PART 32-ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH INSTITUTIONS OF HIGHER EDUCATION, HOSPITALS, AND OTHER NON-PROFIT ORGANIZATIONS

PART 32-ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH INSTITUTIONS OF HIGHER EDUCATION, HOSPITALS, AND OTHER NON-PROFIT ORGANIZATIONS 32.1 Purpose. Subpart A-General (a) General. This part

PART 32-ADMINISTRATIVE REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH INSTITUTIONS OF HIGHER EDUCATION, HOSPITALS, AND OTHER NON-PROFIT ORGANIZATIONS 32.1 Purpose. Subpart A-General (a) General. This part

Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager. Tel:

Federal Agencies Implementation of the Super Circular & the JIR Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

Federal Agencies Implementation of the Super Circular & the JIR Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

Match and Leveraged Resources

Match and Leveraged Resources Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, Designed requirements for DOL-ETA governing direct cost recipients principles, and administrative their subrecipients

Match and Leveraged Resources Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, Designed requirements for DOL-ETA governing direct cost recipients principles, and administrative their subrecipients

OMB Uniform Grant Guidance and NM Procurement

OMB Uniform Grant Guidance and NM Procurement 1 The material appearing in this presentation is for informational purposes only and should not be construed as advice of any kind, including, without limitation,

OMB Uniform Grant Guidance and NM Procurement 1 The material appearing in this presentation is for informational purposes only and should not be construed as advice of any kind, including, without limitation,

The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

2010 Mauldin & Jenkins Single Audits for for Auditees

2010 Mauldin & Jenkins Single Audits for Auditees SINGLE AUDITS FOR AUDITEES Mauldin & Jenkins July 22, 2010 Macon August 3, 2010 - Atlanta PRESENTER Hope Pendergrass Manager Macon Office hpendergrass@mjcpa.com

2010 Mauldin & Jenkins Single Audits for Auditees SINGLE AUDITS FOR AUDITEES Mauldin & Jenkins July 22, 2010 Macon August 3, 2010 - Atlanta PRESENTER Hope Pendergrass Manager Macon Office hpendergrass@mjcpa.com

Jason Galloway, Associate Controller HSC Contract and Grant Accounting

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC 20410-0050 Special Attention of: NOTICE: SD-2015-01 Issued: FEB 2 6 2015 HUO Regional Directors HUD Field

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC 20410-0050 Special Attention of: NOTICE: SD-2015-01 Issued: FEB 2 6 2015 HUO Regional Directors HUD Field

Texas Department of Transportation Page 1 of 19 Public Transportation. (a) Purpose. Title 49 U.S.C. 5329, authorizes the

Purpose. Title 49 U.S.C. 5329, authorizes the") Texas Department of Transportation Page of 0 SUBCHAPTER D. PROGRAM ADMINISTRATION.. Public Transit Safety Program. (a) Purpose. Title U.S.C., authorizes the Secretary of the U.S. DOT to create and implement

Texas Department of Transportation Page of 0 SUBCHAPTER D. PROGRAM ADMINISTRATION.. Public Transit Safety Program. (a) Purpose. Title U.S.C., authorizes the Secretary of the U.S. DOT to create and implement

Cultural Competency Initiative. Program Guidelines

New Jersey STOP Violence Against Women (VAWA) Grants Program Cultural Competency Initiative Cultural Competency Technical Assistance Project Program Guidelines State Office of Victim Witness Advocacy Division

New Jersey STOP Violence Against Women (VAWA) Grants Program Cultural Competency Initiative Cultural Competency Technical Assistance Project Program Guidelines State Office of Victim Witness Advocacy Division

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO Lealan Miller, CPA, CGFM, Partner lmiller@eidebailly.com 208.383.4756 Organization of the Super-Circular, 2 CFR Part 200 Uniform Guidance

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO Lealan Miller, CPA, CGFM, Partner lmiller@eidebailly.com 208.383.4756 Organization of the Super-Circular, 2 CFR Part 200 Uniform Guidance

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Updated. The Minimalist s Guide to the New Procurement Standards in 2 CFR Part 200 Uniform Guidance

Updated The Minimalist s Guide to the New Procurement Standards in 2 CFR Part 200 Uniform Guidance 1 Procurement Standards General Standards must use documented procurement procedures which

Updated The Minimalist s Guide to the New Procurement Standards in 2 CFR Part 200 Uniform Guidance 1 Procurement Standards General Standards must use documented procurement procedures which

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards Thursday, March 20, 2014, 12:30 p.m. 2:00 p.m. ET Venable LLP, Washington, DC Moderator: Jeffrey S. Tenenbaum,

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards Thursday, March 20, 2014, 12:30 p.m. 2:00 p.m. ET Venable LLP, Washington, DC Moderator: Jeffrey S. Tenenbaum,