Vanderbilt University. Direct Cost. Guidelines for Budgeting and Charging Direct Costs on Sponsored Projects

|

|

|

- Florence Charles

- 5 years ago

- Views:

Transcription

1 Vanderbilt University Direct Cost Guidelines for Budgeting and Charging Direct Costs on Sponsored Projects 1

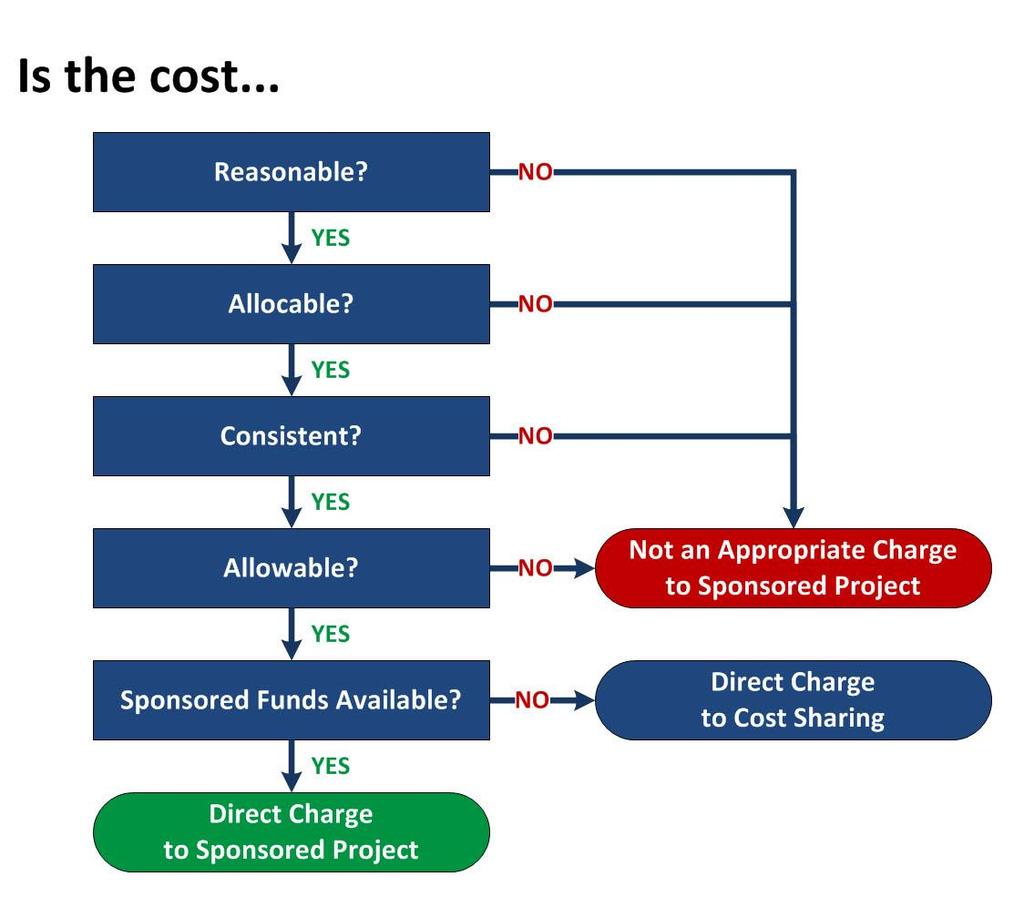

2 Table of Contents Flowchart Illustration Introduction Roles and Responsibilities Direct Costs: Definition and List of Criteria Direct Costs: Reasonableness Direct Costs: Allocability Direct Costs: Consistency o Government Regulation o Costs that are NOT Normally Considered as Direct Costs at Vanderbilt University o Costs that ARE Normally Considered as Direct Costs at Vanderbilt University o Costs Requiring Additional Justification Direct Costs: Allowability Availability of Sponsor Funds Expense Category Coding Appendix A: Examples of Inappropriate Practices Appendix B: Central Offices 2

3 3

4 Introduction In accepting government sponsored projects (grants, contracts, and other types of agreements) Vanderbilt University agrees to abide by government regulations regarding the use of those funds. Office of Management and Budget 2 CFR PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS sets forth general criteria for determining the allowability of direct costs on government sponsored projects. Many government agencies publish additional cost guidelines specific to those agencies, and familiarity with such regulations is also necessary. Although generally not as stringent as government requirements, non-governmental agencies may also have cost guidelines with which Vanderbilt faculty (principal investigators), departmental business officers, and/or grant administrators should be familiar. This Guide summarizes pertinent overall government regulations and Vanderbilt practices used to determine whether or not a particular cost item would be considered an allowable direct cost for budgeting and/or charging on a government sponsored project. Government auditors may use the same guidelines when conducting audits of government sponsored projects awarded to Vanderbilt. Appendix B contains a listing of central offices to contact for assistance in interpreting various circumstances. In addition, business officers / administrators within each department are a valuable resource in applying the principles to particular circumstances. 4

5 Roles and Responsibilities PRINCIPAL INVESTIGATOR Determines financial charges that are allocable to the sponsored project. Attests to the allowability and reasonableness of all expenditures when initiated. Initiates hiring/assignment of personnel working on the sponsored project. Responsible for the completion, accuracy and timeliness of all technical reports. Initiates and approves subcontract agreements and payments. Participates with the Departmental Financial Administrative Officer in the process of documenting cost sharing/matching costs. Initiates requests for re-budgeting of costs on the project. Initiates and proposes resolution of any cost overrun occurring on the project. Reviews and approves interim financial reports prepared by the post-award accounting office. Identifies and allocates any program income (such as revenue from sales and services of goods developed in conjunction with a sponsored project). Ensures compliance with all applicable financial regulations by project personnel and reports instances of non-compliance to the University Compliance Officer. DEPARTMENTAL FINANCIAL ADMINISTRATIVE OFFICER Reviews financial transactions on sponsored programs to ensure that the transaction occurs within the project period. The cost of the transaction is reasonable. The transaction represents a reasonable allocation of the cost. Funds are available in the sponsored program to support the transaction. The transaction is treated consistently with regard to direct/indirect cost purposes if the transaction occurs on a federal project. Prepares and/or approves financial, human resources and other documents for sponsored projects in the following areas: Cost sharing/matching. Provides or maintains databases or files to support sponsored project activities. Prepares documents and provides information for appointment of individuals to sponsored project(s). 5

6 Processes financial transactions and reviews and analyzes Financial Reports for sponsored project(s) Assigns correct expense category codes, provides information and processes purchase documents. Prepares and initiates processing of cost sharing/matching documents. Prepares documents and provides information for re-budgeting. Prepares requests for cost transfers and forwards to the post-award accounting office for review, preparation and processing. Provides information and prepares documents to resolve project cost overruns Processes documents to record program income. Prepares documents and provides information for compliance with the effort reporting policy. Provides information for interim and final financial reports. Provides information for closing documents. Assesses risk associated with financial transactions on sponsored projects and as needed, seeks the advice and approval of higher authority, such as the Dean's Office or the post-award accounting office. Reports instances of financial noncompliance with applicable regulations to the University Compliance Officer. DEPARTMENT CHAIR OR CENTER DIRECTOR Maintains local oversight for the allowability and reasonableness of all project expenditures. Oversees all re-budgeting activities on sponsored projects. Provides oversight on all aspects of program income. Provides oversight on the implementation of University and federal financial policies and regulations at the unit level. Ensures financial compliance with applicable regulations for sponsored projects within department/center and reports instances of noncompliance to the University Compliance Officer. DEAN'S OFFICE (OR DESIGNEE) Approves source of cost sharing/matching funds. Provides local oversight for federal costing regulations issues such as correct identification of costs as direct or indirect costs. Identifies funds to cover project cost overruns. Provides guidance in sponsored project matters that cannot be resolved at the department level. Promotes University Compliance Program regarding research grants management. Investigates instances of financial noncompliance and reports discovered instances of noncompliance to the University Compliance Officer. 6

7 COMPLIANCE OFFICER Informs the University community about the Standards of Conduct and ethical obligations under the Compliance Program. Monitors compliance activities, including policies and procedures, and training and education programs. Serves as a resource to the University on matters of compliance. Maintains a help line for compliance matters. EXECUTIVE ADMINISTRATION Promotes University Compliance Program. Oversees policy formulation in the following areas: Matters relating to direct and indirect charging on sponsored projects. Effort reporting on sponsored projects. Cost sharing. Re-budgeting on sponsored projects. Recording and disposing of program income. Cost transfers. Record retention. Works with others in instances of financial noncompliance to resolve. INTERNAL AUDIT Provide information, analyses, and counsel to assist management in ethically, effectively and efficiently fulfilling their management responsibilities. Examines, evaluates and reports on the adequacy and reliability of existing internal controls. Recommends, as necessary, actions to improve; automated and manual systems of processing revenues and expenses, financial reporting, compliance with laws, regulations and internally developed policies and procedures and the safeguarding of assets. PRE-AWARD OFFICE Shares responsibility with pre-award offices for formulation, implementation, and interpretation of policies regarding allowable costs and for training researchers and staff on proposing and expending allowable costs. POST-AWARD ACCOUNTING OFFICE Prepares invoices and letter of credit draws to sponsors on a timely basis. Prepares quarterly financial reports for federal agencies as required. Prepares interim and final financial reports in coordination with departments. Pre-audits certain financial transactions to ensure compliance with applicable regulations. 7

8 Performs risk analysis for certain categories of expenditures to ensure compliance with applicable regulations. Identifies reportability of program income. Monitors levels of program income. Provides institutional oversight on cost transfers. Processes payments of approved subcontractor invoices. Approves or recommends approval of, carry forward of unexpended funds. Resolves payment problems with sponsors, in conjunction with the the appropriate pre-award office. Prepares, negotiates and administers the institution's indirect cost and fringe benefit rates in conjunction with the post-award accounting office and other university departments. Assists departments in the proper development and administration of service center rates. Provides training as it pertains to the financial administration of sponsored projects to different constituencies. Provides oversight regarding financial compliance. Works with the University Compliance Officer and others to resolve instances of discovered financial noncompliance 8

9 Direct Costs: Definition and List of Criteria Government Definition of Direct Costs: Direct costs (see NOTE below) are those costs that can be identified specifically with a particular sponsored project, or that can be directly assigned to such activity relatively easily with a high degree of accuracy. [Office of Management and Budget Uniform Guidance 2 CFR ] Summary of Criteria for Determining Allowability of Direct Costs: For purposes of determining whether it would be appropriate to budget or charge a certain direct cost on a government sponsored project, principal investigators, departmental business officers and grant administrators should be familiar with the criteria used to define "allowable direct costs". They are: A. The cost must be reasonable, i.e., the cost is generally recognized as necessary for the performance of the project and is one that a prudent person would consider reasonable given the same set of circumstances; B. It must be allocable to the sponsored project, i.e., the cost is incurred for the benefit of only one project or the item can be easily assigned to multiple benefiting projects. A specific project may only be charged that portion of the cost which represents the direct benefit to that project; C. The cost must be treated consistently with other similar costs incurred in like circumstances in accordance with generally accepted accounting principles; and D. The cost must conform to any limitations or exclusions stated in generally accepted accounting principles or in the sponsored agreement, i.e., the cost must be "allowable" and not specifically designated as unallowable by regulation or grant/contract specific award conditions. E. If sponsor funds are available, appropriate direct cost items should be charged to sponsor funds. Guidance for using appropriate Vanderbilt expense category codes is included in the section of this Guide titled "Expense Category Coding". If sponsor funds are not available and it is determined that the scope of work of the project cannot be modified to eliminate the need for the item, then the direct cost item should be charged to an appropriate cost-share expense category [Note: internal approvals for cost sharing may be required] and reflected as a cost of the project, but one borne by Vanderbilt. NOTE: Direct Costs should be net of applicable credits. In accordance with Office of Management and Budget Uniform Guidance 2 CFR , the term "applicable credits" refers to those receipts or reduction-of-expenditure-type transactions that offset or reduce expense items allocable to the Federal award as direct or indirect (F&A) costs. Examples of such transactions are: purchase discounts, rebates or allowances, recoveries or indemnities on losses, insurance refunds or rebates, and adjustments of overpayments or erroneous charges. To the extent that such credits accruing to or received by the non-federal entity relate to allowable costs, they must be credited to the Federal award either as a cost reduction or cash refund, as appropriate. 9

10 Direct Costs: Reasonableness A. Reasonableness Government Regulation... A cost is reasonable if, in its nature and amount, it does not exceed that which would be incurred by a prudent person under the circumstances prevailing at the time the decision was made to incur the cost. The question of reasonableness is particularly important when the non-federal entity is predominantly federally-funded. In determining reasonableness of a given cost, consideration must be given to: (a) Whether the cost is of a type generally recognized as ordinary and necessary for the operation of the non-federal entity or the proper and efficient performance of the Federal award. (b) The restraints or requirements imposed by such factors as: sound business practices; arm's-length bargaining; Federal, state, local, tribal, and other laws and regulations; and terms and conditions of the Federal award. (c) Market prices for comparable goods or services for the geographic area. (d) Whether the individuals concerned acted with prudence in the circumstances considering their responsibilities to the non-federal entity, its employees, where applicable its students or membership, the public at large, and the Federal government. (e) Whether the non-federal entity significantly deviates from its established practices and policies regarding the incurrence of costs, which may unjustifiably increase the Federal award's cost. [Office of Management and Budget Uniform Guidance 2 CFR ] 10

11 Direct Costs: Allocability B. Allocability Government Regulation... Allocability: General Rule (a) A cost is allocable to a particular Federal award or other cost objective if the goods or services involved are chargeable or assignable to that Federal award or cost objective in accordance with relative benefits received. This standard is met if the cost: (1) Is incurred specifically for the Federal award; (2) Benefits both the Federal award and other work of the non-federal entity and can be distributed in proportions that may be approximated using reasonable methods; and (3) Is necessary to the overall operation of the non-federal entity and is assignable in part to the Federal award in accordance with the principles in this subpart. (b) All activities which benefit from the non-federal entity's indirect (F&A) cost, including unallowable activities and donated services by the non-federal entity or third parties, will receive an appropriate allocation of indirect costs. (c) Any cost allocable to a particular Federal award under the principles provided for in this part may not be charged to other Federal awards to overcome fund deficiencies, to avoid restrictions imposed by Federal statutes, regulations, or terms and conditions of the Federal awards, or for other reasons. However, this prohibition would not preclude the non-federal entity from shifting costs that are allowable under two or more Federal awards in accordance with existing Federal statutes, regulations, or the terms and conditions of the Federal awards. (d) Direct cost allocation principles. If a cost benefits two or more projects or activities in proportions that can be determined without undue effort or cost, the cost must be allocated to the projects based on the proportional benefit. If a cost benefits two or more projects or activities in proportions that cannot be determined because of the interrelationship of the work involved, then, notwithstanding paragraph (c) of this section, the costs may be allocated or transferred to benefitted projects on any reasonable documented basis. Where the purchase of equipment or other capital asset is specifically authorized under a Federal award, the costs are assignable to the Federal award regardless of the use that may be made of the equipment or other capital asset involved when no longer needed for the purpose for which it was originally required. See also Insurance coverage through Property trust relationship and Equipment and other capital expenditures. (e) If the contract is subject to CAS, costs must be allocated to the contract pursuant to the Cost Accounting Standards. To the extent that CAS is applicable, the allocation of costs in accordance with CAS takes precedence over the allocation provisions in this part. [Office of Management and Budget Uniform Guidance 2 CFR ] 11

12 Direct Costs: Consistency C. Consistency Government Regulation... Costs incurred for the same purpose in like circumstances must be treated consistently as either direct or indirect costs. Where an institution treats a particular type of cost as a direct cost of sponsored agreements, all costs incurred for the same purpose in like circumstances shall be treated as direct costs of all activities of the institution (see "Vanderbilt University's Treatment of Direct Costs" below). Identification with the Federal award rather than the nature of the goods and services involved is the determining factor in distinguishing direct from indirect (F&A) costs of Federal awards. Typical costs charged directly to a sponsored agreement are the compensation of employees for performance of work under the sponsored agreement, including related fringe benefit costs to the extent they are consistently treated, in like circumstances, by the institution as direct rather than indirect costs; the costs of materials consumed or expended in the performance of the work; and other items of expense incurred for the sponsored agreement, including extraordinary utility consumption. The cost of materials supplied from stock or services rendered by specialized facilities or other institutional service operations may be included as direct costs of sponsored agreements, provided such items are consistently treated, in like circumstances, by the institution as direct rather than indirect costs (see "Vanderbilt University's Treatment of Direct Costs" below), and are charged under a recognized method of computing actual costs, and conform to generally accepted cost accounting practices consistently followed by the institution. The salaries of administrative and clerical staff should normally be treated as indirect (F&A) costs. Direct charging of these costs may be appropriate only if all of the following conditions are met: 1) Administrative or clerical services are integral to a project or activity; 2) Individuals involved can be specifically identified with the project or activity; 3) Such costs are explicitly included in the budget or have the prior written approval of the Federal awarding agency; and 4) The costs are not also recovered as indirect costs. [Office of Management and Budget Uniform Guidance 2 CFR ] 12

13 Vanderbilt University's Treatment of Direct Costs... The government requires that the major research colleges and universities disclose in writing their general practices regarding classification of costs as direct costs as practices may vary between universities (e.g., University X may routinely budget and charge as direct costs long distance telephone expenses, while University Y does not). At Vanderbilt University, there are certain "like circumstances" where costs are consistently treated as direct costs of sponsored projects. Conversely, there are certain "like circumstances" where costs are not considered direct costs, and should NOT be budgeted or charged as direct costs on sponsored projects. However, in all cases, the following standard applies: Identification with the Federal award rather than the nature of the goods and services involved is the determining factor in distinguishing direct from indirect (F&A) costs of Federal awards. [Office of Management and Budget Uniform Guidance 2 CFR ] Examples of Costs that are NOT Normally Considered as Direct Costs at Vanderbilt University At Vanderbilt University, the following costs are NOT normally budgeted and charged as direct costs of sponsored projects: Salaries of individuals engaged in routine departmental or administrative work that benefits all activities of the department (instruction, research, training, public service, etc.), i.e., there is no direct relationship to a specific sponsored project's scope of work. Supplies and materials for routine departmental or administrative activities of the department that benefit all activities of the department (instruction, research, training, public service, etc.), i.e., there is no direct relationship to a specific sponsored project's scope of work. Other costs such as travel, repairs, fees and services, local and long distance telephone expenses, copying and postage that are for routine departmental or administrative use, and do not have a direct relationship to a specific sponsored project's scope of work. General office items with multi-functional use such as computers, fax machines, answering machines, staplers, hole punches, filing cabinets, chairs, desks, calculators, waste baskets, etc.), that do not have a direct relationship to a specific sponsored project's scope of work. Examples of Costs that ARE Normally Considered as Direct Costs at Vanderbilt University At Vanderbilt University, the following costs ARE normally budgeted and charged as direct costs. The common element is that the cost is necessary to perform the project's stated scope of work. Salaries and fringe benefits of faculty, technicians, post docs, graduate research assistants and other staff engaged in performing sponsored project's scope of work. Supplies and materials necessary for performing sponsored project's scope of work. 13

14 Other costs such as travel, subcontracts, repairs, maintenance, fees and services, telephone expenses, copying, postage, etc., necessary for performing sponsored project's scope of work. Capital equipment that is approved by the sponsor (or internally approved if allowed by the sponsor). Service/maintenance agreements on capital equipment approved by the sponsor (or internally approved if allowed by the sponsor). Identification with the Federal award rather than the nature of the goods and services involved is the determining factor in distinguishing direct from indirect (F&A) costs of Federal awards. [Office of Management and Budget Uniform Guidance 2 CFR ] 14

15 EXAMPLES Clerical Salaries Clerical salaries CAN be budgeted and charged as direct costs under certain circumstances. Simply knowing the "nature of the good or service", e.g., clerical salary, is not sufficient to determine whether the cost is an appropriate direct charge to a sponsored project. In order to make the determination, one must know the cost's relationship to the sponsored work. For example: Clerical salaries that are paid to individuals entering data from a survey that is part of the sponsored project's scope of work may be appropriately charged as direct costs. Clerical salaries that are paid to individuals for routine administrative work such as processing purchase requisitions, reviewing monthly ledgers, processing new proposals, etc., and that benefit all aspects of a department, including research, are normally NOT appropriate direct cost charges. Other Examples Following are other examples of costs and the circumstances under which they may be incurred. For each cost/circumstance, it is indicated whether the cost would be budgeted and charged as a direct cost under Vanderbilt direct charge guidelines. Direct Cost? Salaries expense incurred under the following circumstances YES NO 1. Processing purchase orders on a research grant (such as an R01 ) 2. Processing purchase orders on a center/program project grant (admin effort documented in proposal as part of scope of work) 3. Proposal development (writing, editing, copying and mailing proposals) 4. Principal Investigator effort to write annual project report (may include next budget year s proposal) 5. Data entry (data collected under project scope of work) 6. Data entry financial transactions for a research grant are entered into financial shadow system (Note: may be considered a direct cost if part of the administrative budget on a program/project or center grant AND approved by the sponsor.) 15

16 Direct Cost? Supplies and/or services expense incurred under the following circumstances YES NO 1. Copying costs for copying purchase orders, monthly ledgers 2. Copying costs for annual progress reports 3. Mailing costs for shipments of research materials and deliverables if necessary to perform the project s scope of work 4. Copying costs for copying forms to mail out to survey recipients (survey is part of project scope of work) 5. Manila folders for general office use 6. Manila folders for filing survey responses, lab results Identification with the Federal award rather than the nature of the goods and services involved is the determining factor in distinguishing direct from indirect (F&A) costs of Federal awards. [Office of Management and Budget Uniform Guidance 2 CFR ] Justification required in proposals that budget certain costs as direct costs: For the following cost items (and for any others that a layperson may consider routine and administrative in nature), specific written justification as to the relationship between the cost and the proposed project's scope of work should be completed and submitted to the appropriate preaward grants or contracts office as a part of the proposal to the sponsoring agency. The documentation should explain the direct benefit relationship between these cost items and the proposed scope of work. Clerical and administrative salaries Office Supplies Postage Local telephone charges Memberships Subscriptions Answering machine/beepers Items generally thought of as having multi-functional use (staplers, hole punches, filing cabinets, chairs, desks, computers, printers, fax machines, calculators, waste baskets, etc.) 16

17 Direct Costs: Allowability D. Allowability Government Regulation... The following costs have been specifically identified by the Government as unallowable on Government grants and contracts in Office of Management and Budget Uniform Guidance 2 CFR 200. However, individual agencies and programs have authority to approve certain of these costs. For example, it may be appropriate to budget "alcoholic beverages" as a direct cost of a sponsored project to study effects of alcohol on reflex movement. To budget or charge such a cost, one must fully disclose such items in the budget narrative or have written approval by the sponsoring agency grant/contract management officer (if approval was not obtained in the original proposal and award document). The list below is not all inclusive. Individual agency and program requirements may list other "unallowable" costs. 1. Advertising for general promotion of the University, including printed materials, promotional items, memorabilia, gifts, and souvenirs; 2. Advertising for recruitment purposes that includes color or is excessive in size; 3. Alcoholic beverages; 4. Alumni or fund-raising activities; 5. Antiques; 6. Bad debt write-offs; 7. Charitable contributions; 8. Commencement expenses; 9. Cost Overruns: Any costs allocable to a particular sponsored agreement may not be shifted to other sponsored agreements in order to meet deficiencies caused by overruns or other fund considerations, to avoid restrictions imposed by law or by terms of the sponsored agreement, or for other reasons of convenience; 10. Costs on Industry, Foreign Government or Other Non-Government Grants / Contracts: Any costs allocable to activities sponsored by industry, foreign governments or other sponsors may not be shifted to federally-sponsored agreements; 11. Decorative objects for private offices; 12. Entertainment; 13. Fine/original art; 14. Fines and penalties; 15. First-class/business-class air travel differentials; 16. Flowers; 17. Gifts, prizes, and awards; 18. Goods or services for personal use; 19. Lobbying; 20. Memberships in airline travel clubs; 21. Memberships in civic, social, community organizations or country clubs; 17

18 22. Faculty and exempt staff salary in excess of base rates paid by the institution. Other limitations may apply, such as the Public Health Service salary cap. [See below full text of government regulation concerning allowable rates of pay for faculty.] 23. Selling or marketing products or services of the University; and 24. Social events. Allowable Rates of Pay for Faculty, Office of Management and Budget Uniform Guidance 2 CFR : (h) Institutions of higher education (IHEs). (1) Certain conditions require special consideration and possible limitations in determining allowable personnel compensation costs under Federal awards. Among such conditions are the following: (i) Allowable activities. Charges to Federal awards may include reasonable amounts for activities contributing and directly related to work under an agreement, such as delivering special lectures about specific aspects of the ongoing activity, writing reports and articles, developing and maintaining protocols (human, animals, etc.), managing substances/chemicals, managing and securing project-specific data, coordinating research subjects, participating in appropriate seminars, consulting with colleagues and graduate students, and attending meetings and conferences. (ii) Incidental activities. Incidental activities for which supplemental compensation is allowable under written institutional policy (at a rate not to exceed institutional base salary) need not be included in the records described in paragraph (i) of this section to directly charge payments of incidental activities, such activities must either be specifically provided for in the Federal award budget or receive prior written approval by the Federal awarding agency. (2) Salary basis. Charges for work performed on Federal awards by faculty members during the academic year are allowable at the IBS rate. Except as noted in paragraph (h)(1)(ii) of this section, in no event will charges to Federal awards, irrespective of the basis of computation, exceed the proportionate share of the IBS for that period. This principle applies to all members of faculty at an institution. IBS is defined as the annual compensation paid by an IHE for an individual's appointment, whether that individual's time is spent on research, instruction, administration, or other activities. IBS excludes any income that an individual earns outside of duties performed for the IHE. Unless there is prior approval by the Federal awarding agency, charges of a faculty member's salary to a Federal award must not exceed the proportionate share of the IBS for the period during which the faculty member worked on the award. (3) Intra-Institution of Higher Education (IHE) consulting. Intra-IHE consulting by faculty is assumed to be undertaken as an IHE obligation requiring no compensation in addition to IBS. However, in unusual cases where consultation is across departmental lines or involves a separate or remote operation, and the work performed by the faculty member is in addition to his or her 18

19 regular responsibilities, any charges for such work representing additional compensation above IBS are allowable provided that such consulting arrangements are specifically provided for in the Federal award or approved in writing by the Federal awarding agency. (4) Extra Service Pay normally represents overload compensation, subject to institutional compensation policies for services above and beyond IBS. Where extra service pay is a result of Intra-IHE consulting, it is subject to the same requirements of paragraph (b) above. It is allowable if all of the following conditions are met: (i) The non-federal entity establishes consistent written policies which apply uniformly to all faculty members, not just those working on Federal awards. (ii) The non-federal entity establishes a consistent written definition of work covered by IBS which is specific enough to determine conclusively when work beyond that level has occurred. This may be described in appointment letters or other documentations. (iii) The supplementation amount paid is commensurate with the IBS rate of pay and the amount of additional work performed. See paragraph (h)(2) of this section. (iv) The salaries, as supplemented, fall within the salary structure and pay ranges established by and documented in writing or otherwise applicable to the non-federal entity. (v) The total salaries charged to Federal awards including extra service pay are subject to the Standards of Documentation as described in paragraph (i) of this section. (5) Periods outside the academic year. (i) Except as specified for teaching activity in paragraph (h)(5)(ii) of this section, charges for work performed by faculty members on Federal awards during periods not included in the base salary period will be at a rate not in excess of the IBS. (ii) Charges for teaching activities performed by faculty members on Federal awards during periods not included in IBS period will be based on the normal written policy of the IHE governing compensation to faculty members for teaching assignments during such periods. (6) Part-time faculty. Charges for work performed on Federal awards by faculty members having only part-time appointments will be determined at a rate not in excess of that regularly paid for part-time assignments. [Office of Management and Budget Circular Uniform Guidance 2 CFR ] NOTE: OMB Uniform Guidance 2 CFR as reprinted above discusses sponsoring agency approvals for payroll/consulting transactions. The appropriate Vanderbilt University internal approvals are also required. 19

20 E. Availability of Funds If sponsor funds are available, appropriate direct cost items should be charged to sponsor funds in accordance with the expense category coding instructions in the following section, "Expense Category Coding". If funds are NOT available and it is determined that the scope of work of the sponsored project cannot be modified to eliminate the need for the item, then the direct cost item should be charged to an appropriate cost share expense category [Note: internal approvals may be required] and reflected as a cost of the project, but one borne by Vanderbilt. Expense Category Coding What is an expense category? At Vanderbilt, budget line items and individual expense transactions are identified by expense category numbers. The expense category classifies the transaction as salaries, fringes, supplies, travel, etc. To select the correct expense category for sponsored project budget line items or expense transactions, the principal investigator and/or grant administrator should be familiar with Vanderbilt's expense category structure. A complete listing of Vanderbilt expense categories is maintained by the Office of Contract and Grant Accounting. Each grant administrator should be familiar with the expense categories available for use on sponsored projects and other centers.. Why the emphasis on proper expense category coding? One of the elements most critical to successful financial administration of sponsored projects is the assignment of appropriate expense categories to budget line items and expense transactions, for the following reasons. (1) Miscoded expenses can result in incorrect indirect cost charges. The expense category determines whether or not the cost will be included in "modified total direct cost" and therefore subject to indirect cost. (2) Failure to identify capital equipment purchases can result in noncompliance with internal and external property management regulations. Federal regulations require that all capital equipment purchases be added to the central inventory system. The expense category used on the capital equipment requisition is one method used by central equipment inventory offices to identify capital equipment purchases to be added to central inventories. (3) Errors in expense category coding can result in inappropriate conclusions by the principal investigator and/or sponsor regarding financial status. (4) Improperly coded expenses can result in inappropriate conclusions by auditors and can adversely impact Vanderbilt's ability to effectively monitor for compliance with federal regulations regarding allowability. In an internal or external review or audit, the expense 20

21 category determines the type of review or audit procedure to which the expense is subjected, and whether the expense is viewed initially as allowable or unallowable. (5) The expense category distinguishes between costs funded by the agency and those cost shared by Vanderbilt. Failure to use a cost sharing expense category on cost-shared expenditures will understate Vanderbilt's contribution to the project. Do all proposal budgets need to be detailed at the expense category level? No, not all proposal budgets need to be prepared at the expense category level. However, funded proposals must have budgets at the expense category level. What are some of the special circumstances related to expense category coding? In many situations, there are several expense categories that could appropriately be used, and it is up to the grant administrator, based on guidance from the appropriate Dean, Director, or Department Head, to choose the expense category that best describes the good or service being acquired. Following are general comments on selected expense areas. Personnel Costs: Salaries and wages and related fringe benefit expense categories, are used for individuals hired and paid through the Vanderbilt payroll system, and the expense categories used are determined by the job code assigned to the position. Payments for services outside the Vanderbilt payroll system should be charged to Professional Services, not salaries and wages. Human Resources will assist you in determining the appropriate job code for new positions or in reclassifying existing positions. Supplies: For allowability reasons discussed later, proper distinction between office supplies and lab/research supplies is critical, particularly on government funded projects. Expense categories "Spec Res Unrestricted", "Special Prog/Project", "Misc Expense", "Other Expenses", and "Unassigned Expenses" are not appropriate for use, as they do not specifically identify the type of cost being charged. Domestic vs. Foreign Travel: Foreign travel should be charged to expense category "Travel, Foreign". Any alcoholic beverages or entertainment costs to be reimbursed to a traveler must be charged to the appropriate entertainment expense category. Subject Participation: All subject payments (i.e. payments to research participants) should be charged to expense category "Subject Participation", primarily used for clinical trials. Participant Support Costs: Direct costs for items such as stipends or subsistence allowances, travel allowances, and registration fees paid to or on behalf of participants or trainees (but not employees) in connection 21

22 with conferences, or training projects. For NIH awards these costs are only allowable when identified in the funding opportunity announcement (FOA). For the purposes of Kirschstein- NRSA programs, this term does not apply. NIH will continue to use the terms trainees, traineerelated expenses, and trainee travel in accordance with NRSA Regulations. Subcontracts: The first $25,000 in payments to a subcontractor on a sponsored project should be charged to "Sub-Cont Under $25K". Payments in excess of $25,000 should be charged to "Sub-Cont over $25K". Capital Equipment: Capital equipment funded by the sponsor should be charged to appropriate Cap Equip expense categories. Cost-shared capital equipment should be charged to "Equipment Cost Share". Capital equipment is defined as "an article of nonexpendable tangible personal property having a useful life of more than one year, and an acquisition cost of $5,000* or more per unit." 22

23 Appendix A: Inappropriate Practices The following examples are not all-inclusive. They are intended to be illustrative of certain practices that can result in direct cost disallowance during audits of sponsored agreements. Inappropriate Practices: 1. Purchasing goods, supplies, or equipment at the end of the project simply to use up unspent funds. 2. Charging 100% of a direct cost item to a sponsored project if part of the item will be used by other projects or non-sponsored activities. 3. Replenishing departmental office supplies with grant funds. 4. "Rotating" charges among sponsored projects by month without establishing that the rotation schedule credibly reflects the relative benefit to each grant. 5. Assigning charges to the sponsored project with the largest remaining balance. 6. Identifying a cost as something other than what it actually is by using an incorrect expense category code. In order to be allowable, direct charges must be assignable to a sponsored project "in accordance with benefits received". If the sponsored project could not have reasonably benefited from the items purchased, then the cost would not be allocable to the sponsored project. Identification with the Federal award rather than the nature of the goods and services involved is the determining factor in distinguishing direct from indirect (F&A) costs of Federal awards. [Office of Management and Budget Uniform Guidance 2 CFR ] 23

24 Appendix B: Central Offices - Sponsored Awards Administration Vanderbilt University maintains central offices to coordinate overall activities related to sponsored projects and promote consistent practices among the various recipients of contracts and grants. These offices are available to assist principal investigators, department chairs and/or administrators, deans and/or deans' office administrators and directors and/or directors' office administrators in interpreting agency regulations and Vanderbilt policy and procedures relating to budgeting and charging direct costs on sponsored projects. PRE-AWARD OFFICE Sponsored Programs Administration Responsible for submission of grant proposals for external support of research, creative, instructional, and service activities; review and approval of proposals that will result in contracts, negotiation and acceptance of research and research-related contracts and supports investigators who have or plan to apply for external funding and departmental administrators who assist these investigators with proposal preparation and award administration. POST-AWARD OFFICE Office of Contract and Grant Accounting, Responsible for coordinating compliance activities related to post award management including reviewing selected transactions, reporting financial results to sponsoring agencies, and coordinating agency audits of University contracts and grants. 24

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT)

") GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

Office of Sponsored Programs Budgetary and Cost Accounting Procedures

Office of Sponsored Programs Budgetary and Cost Accounting Procedures Table of Contents 1. Purpose and Services 2. Definitions of Terms 3. Budget Items 4. Travel 5. Effort Certification Reporting 6. Costing

Office of Sponsored Programs Budgetary and Cost Accounting Procedures Table of Contents 1. Purpose and Services 2. Definitions of Terms 3. Budget Items 4. Travel 5. Effort Certification Reporting 6. Costing

RESEARCH ADMINISTRATION FORUM Allowable Costs. Uniform Guide

RESEARCH ADMINISTRATION FORUM Allowable Costs Uniform Guide Objectives Understand what are allowable and unallowable costs to Federal grants Understand the importance of properly budgeting for costs on

RESEARCH ADMINISTRATION FORUM Allowable Costs Uniform Guide Objectives Understand what are allowable and unallowable costs to Federal grants Understand the importance of properly budgeting for costs on

Financial Oversight of Sponsored Projects Principal Investigator and Department Administrator Responsibilities

Principal Investigator and Department Administrator Responsibilities Boston College Office for Sponsored Programs Office for Research Compliance and Intellectual Property March 2004 Introduction This guide

Principal Investigator and Department Administrator Responsibilities Boston College Office for Sponsored Programs Office for Research Compliance and Intellectual Property March 2004 Introduction This guide

Policy on Cost Allocation, Cost Recovery, and Cost Sharing

President Page 1 of 11 PURPOSE: Provide guidance and structure when allocating and documenting costs (direct and indirect) for extramurally funded awards. Serves to provide direction for budgeting, allocating

President Page 1 of 11 PURPOSE: Provide guidance and structure when allocating and documenting costs (direct and indirect) for extramurally funded awards. Serves to provide direction for budgeting, allocating

Federal Rules for Sponsored Programs. Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

FY2016 Grant Application Workshop. Basics of Financial Management for Grant Applicants

FY2016 Grant Application Workshop Basics of Financial Management for Grant Applicants Jerron M. Johnson Chief Field Program Officer Missouri Community Service Commission November 19, 2015 Session Overview

FY2016 Grant Application Workshop Basics of Financial Management for Grant Applicants Jerron M. Johnson Chief Field Program Officer Missouri Community Service Commission November 19, 2015 Session Overview

Grant and Contract Accounting

University of Washington Faculty Grants Management Program Grant and Contract Accounting Sue Camber, Assistant Vice President Research Accounting and Analysis Grant and Contract Accounting University of

University of Washington Faculty Grants Management Program Grant and Contract Accounting Sue Camber, Assistant Vice President Research Accounting and Analysis Grant and Contract Accounting University of

Policy on Principal Investigators Duties and Responsibilities on Sponsored Projects

Office of Research and Sponsored Programs Foundation Administration Policy on Principal Investigators Duties and Responsibilities on Sponsored Projects Policy Index I. Introduction II. Policy Statement

Office of Research and Sponsored Programs Foundation Administration Policy on Principal Investigators Duties and Responsibilities on Sponsored Projects Policy Index I. Introduction II. Policy Statement

RACE TO THE TOP EARLY LEARNING CHALLENGE

APRIL 2015 84.412 RACE TO THE TOP EARLY LEARNING CHALLENGE State Project/Program: Federal Authorization: State Authorization: RACE TO THE TOP EARLY LEARNING CHALLENGE U. S. DEPARTMENT OF EDUCATION PL 111-5

APRIL 2015 84.412 RACE TO THE TOP EARLY LEARNING CHALLENGE State Project/Program: Federal Authorization: State Authorization: RACE TO THE TOP EARLY LEARNING CHALLENGE U. S. DEPARTMENT OF EDUCATION PL 111-5

Sponsored Programs Roles & Responsibilities

The University of Florida is committed to acting with integrity in the management of sponsored programs. The goals of this document are to provide descriptions of key individuals or units and their responsibilities

The University of Florida is committed to acting with integrity in the management of sponsored programs. The goals of this document are to provide descriptions of key individuals or units and their responsibilities

Sponsored Programs Roles & Responsibilities

The University of Florida is committed to acting with integrity in the management of sponsored programs. The goals of this document are to provide descriptions of key individuals or units and their responsibilities

The University of Florida is committed to acting with integrity in the management of sponsored programs. The goals of this document are to provide descriptions of key individuals or units and their responsibilities

University of Pittsburgh

I. Scope This guideline establishes the requirements for recording direct and indirect costs on the financial accounting records of the University in accordance with Federal regulations and generally accepted

I. Scope This guideline establishes the requirements for recording direct and indirect costs on the financial accounting records of the University in accordance with Federal regulations and generally accepted

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY. Office of Contracts and Grants December, 2014

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

Office of Management and Budget (OMB) Uniform Guidance Policies & Procedures

Uniform Guidance Policies & Procedures") Office of Management and Budget (OMB) Uniform Guidance Policies & Procedures Revised March 2018 Contents Uniform Guidance Basics... 1 Timeline... 1 PCC Policies & Procedures... 2 The Grant Team: Grant

Office of Management and Budget (OMB) Uniform Guidance Policies & Procedures Revised March 2018 Contents Uniform Guidance Basics... 1 Timeline... 1 PCC Policies & Procedures... 2 The Grant Team: Grant

UNIVERSITY RESEARCH ADMINISTRATION FINANCIAL ROLES AND RESPONSIBILITIES MATRIX - WORK IN PROGRESS 10/03/2013 Roles.

UNIVERSITY RESEARCH ADMINISTRATION Roles Business Internal Controller's Clinical Responsibilities PI Office Chair Dean Audit Office OCR GCFA GCA PROVOST Trials Office I. GENERAL RESEARCH ADMINISTRATION

UNIVERSITY RESEARCH ADMINISTRATION Roles Business Internal Controller's Clinical Responsibilities PI Office Chair Dean Audit Office OCR GCFA GCA PROVOST Trials Office I. GENERAL RESEARCH ADMINISTRATION

CHAPTER 10 Grant Management

CHAPTER 10 Grant Management Table of Contents Page GRANT MANAGEMENT 1 Introduction... 1 Financial Management of Grants... 1 Planning and Budgeting... 1 Application and Implementation... 2 Monitoring...

CHAPTER 10 Grant Management Table of Contents Page GRANT MANAGEMENT 1 Introduction... 1 Financial Management of Grants... 1 Planning and Budgeting... 1 Application and Implementation... 2 Monitoring...

OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN

TO 2 CFR 200 (UNIFORM ADMIN") Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Diane Dean, Director Kathy Hancock, Assistant Grants Compliance Officer Joel Snyderman, Assistant Grants Compliance Officer

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar San Diego, CA October 2015 Diane Dean,

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar San Diego, CA October 2015 Diane Dean,

Financial Oversight of Sponsored Projects

Financial Oversight of Sponsored Projects Today s Agenda Introduction Reasons for Principal Investigator Oversight Sponsor and University Policies General Considerations Unallowable Costs Re-Budgeting

Financial Oversight of Sponsored Projects Today s Agenda Introduction Reasons for Principal Investigator Oversight Sponsor and University Policies General Considerations Unallowable Costs Re-Budgeting

10 CFR 600: KNOW YOUR REQUIREMENTS

WEATHERIZATION ASSISTANCE PROGRAM 10 CFR 600: KNOW YOUR REQUIREMENTS Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and

WEATHERIZATION ASSISTANCE PROGRAM 10 CFR 600: KNOW YOUR REQUIREMENTS Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and

Grant Administration Glossary of Commonly-Used Terms in Sponsored Programs

Page 1 of 6 Grant Administration Allowability: The determination of whether or not costs can be charged to a sponsored project as a direct or indirect cost. Allocability: A cost is allocable to a particular

Page 1 of 6 Grant Administration Allowability: The determination of whether or not costs can be charged to a sponsored project as a direct or indirect cost. Allocability: A cost is allocable to a particular

Uniform Grants Guidance. Colorado Charter School Institute Cassie Walgren, Controller

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

GEORGE MASON UNIVERSITY OFFICE SPONSORED PROGRAMS. Matt Kluger, Vice President for Research & Economic Development

GEORGE MASON UNIVERSITY OFFICE SPONSORED PROGRAMS Memo to: From: Subject: Principal Investigators on Federal Sponsored Projects Unit Research Administrators Research Associate Deans Deans and Directors

GEORGE MASON UNIVERSITY OFFICE SPONSORED PROGRAMS Memo to: From: Subject: Principal Investigators on Federal Sponsored Projects Unit Research Administrators Research Associate Deans Deans and Directors

WELCOME. Pre-Award Phase Training

WELCOME Pre-Award Phase Training Morning Session Welcome GATA and New Federal Guidance Overview Cost Principles - Basic Considerations 10:00 10:15 BREAK Cost Principles Basic Consideration Cost Principles

WELCOME Pre-Award Phase Training Morning Session Welcome GATA and New Federal Guidance Overview Cost Principles - Basic Considerations 10:00 10:15 BREAK Cost Principles Basic Consideration Cost Principles

SPONSORED PROGRAMS AWARDS, EXPENDITURES, AND ALLOWABILTY APRIL 2015 Policy

SPONSORED PROGRAMS AWARDS, EXPENDITURES, AND ALLOWABILTY APRIL 2015 Policy 2.2.01 Purpose: This policy was developed to ensure consistent compliance with 2 CFR part 200 Uniform Guidance and the Cost Accounting

SPONSORED PROGRAMS AWARDS, EXPENDITURES, AND ALLOWABILTY APRIL 2015 Policy 2.2.01 Purpose: This policy was developed to ensure consistent compliance with 2 CFR part 200 Uniform Guidance and the Cost Accounting

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS. National Historical Publications and Records Commission

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

Understanding F&A THE RESEARCH ADMINISTRATION IMPROVEMENT NETWORK. Presented by. TRAIN at the University of South Florida

Understanding F&A Presented by THE RESEARCH ADMINISTRATION IMPROVEMENT NETWORK Facilities & Administrative (F&A) Costs F&A (or Indirect Costs) are costs that are incurred for common or joint objectives

Understanding F&A Presented by THE RESEARCH ADMINISTRATION IMPROVEMENT NETWORK Facilities & Administrative (F&A) Costs F&A (or Indirect Costs) are costs that are incurred for common or joint objectives

4.12 Effort Certification

4.112 Grants and Cooperative Agreements 4.1121 The Public Health Service ("PHS") and the National Science Foundation ("NSF") have regulations promoting objectivity in research by requiring that a university

4.112 Grants and Cooperative Agreements 4.1121 The Public Health Service ("PHS") and the National Science Foundation ("NSF") have regulations promoting objectivity in research by requiring that a university

Post Award Manual. A. Chart of Accounts Overview

Post Award Manual Introduction: Award Management Section I. Section II. Sponsored Award Set up A. Chart of Accounts Overview Sponsored Expenditures Guidelines A. Introduction Purpose Who Should Use This

Post Award Manual Introduction: Award Management Section I. Section II. Sponsored Award Set up A. Chart of Accounts Overview Sponsored Expenditures Guidelines A. Introduction Purpose Who Should Use This

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar Chicago, IL October 2016 Diane Dean, Director

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar Chicago, IL October 2016 Diane Dean, Director

POLICY STATEMENT EFFECTIVE DATE

Policy Section: Office of Research and Project Administration & Sponsored Research Accounting Policy Number and Title: Charging of Administrative or Clerical Salaries and General Expenses to Federal Sponsored

Policy Section: Office of Research and Project Administration & Sponsored Research Accounting Policy Number and Title: Charging of Administrative or Clerical Salaries and General Expenses to Federal Sponsored

University of San Francisco Office of Contracts and Grants Subaward Policy and Procedures

Summary 1. Subaward Definitions A. Subaward B. Subrecipient University of San Francisco Office of Contracts and Grants Subaward Policy and Procedures C. Office of Contracts and Grants (OCG) 2. Distinguishing

Summary 1. Subaward Definitions A. Subaward B. Subrecipient University of San Francisco Office of Contracts and Grants Subaward Policy and Procedures C. Office of Contracts and Grants (OCG) 2. Distinguishing

Jason Galloway, Associate Controller HSC Contract and Grant Accounting

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

Uniform Guidance Sponsored Projects Services

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Guidelines for the Acceptance and Use of Externally Funded Grants and Contracts

Guidelines for the Acceptance and Use of Externally Funded Grants and Contracts http://www.una.edu/sponsored-programs/ Tanja F. Blackstone, PhD Director, Sponsored Programs tfblackstone@una.edu University

Guidelines for the Acceptance and Use of Externally Funded Grants and Contracts http://www.una.edu/sponsored-programs/ Tanja F. Blackstone, PhD Director, Sponsored Programs tfblackstone@una.edu University

Understanding F&A THE RESEARCH ADMINISTRATION IMPROVEMENT NETWORK. Presented by. TRAIN at the University of South Florida

Understanding F&A Presented by THE RESEARCH ADMINISTRATION IMPROVEMENT NETWORK Facilities & Administrative (F&A) Costs F&A (or Indirect Costs) are costs that are incurred for common or joint objectives

Understanding F&A Presented by THE RESEARCH ADMINISTRATION IMPROVEMENT NETWORK Facilities & Administrative (F&A) Costs F&A (or Indirect Costs) are costs that are incurred for common or joint objectives

University of Pittsburgh

I. Guideline Background University sponsors are increasingly relying on institutions for the development of adequate compliance programs for the financial administration of grants and contracts. An adequate

I. Guideline Background University sponsors are increasingly relying on institutions for the development of adequate compliance programs for the financial administration of grants and contracts. An adequate

Base. Base Determination and Cost Sharing. Bases represent the direct cost activities of an institution. Generally they consist of: 2/10/2014

Determination and Cost Sharing s represent the direct cost activities of an institution. Generally they consist of:» Instruction & departmental research» Organized research» Other sponsored activity (public

Determination and Cost Sharing s represent the direct cost activities of an institution. Generally they consist of:» Instruction & departmental research» Organized research» Other sponsored activity (public

An Exercise in Effort

3 rd Annual Symposium for Research Administrators An Exercise in Effort Brian Bertlshofer, Director, Cost Analysis and Compliance bertlsbj@email.unc.edu Aja Saylor, Central Effort Coordinator ajasaylor@unc.edu

3 rd Annual Symposium for Research Administrators An Exercise in Effort Brian Bertlshofer, Director, Cost Analysis and Compliance bertlsbj@email.unc.edu Aja Saylor, Central Effort Coordinator ajasaylor@unc.edu

Johns Hopkins University Finance Document Library. Sponsored Projects - Effort Reporting Policies & Procedures. Table of Contents

Johns Hopkins University Finance Document Library Sponsored Projects - Effort Reporting Policies & Procedures Table of Contents I. Policy Section SP-EFF-PL-01--Effort Reporting II. Procedure Section SP-EFF-PR-01--Effort

Johns Hopkins University Finance Document Library Sponsored Projects - Effort Reporting Policies & Procedures Table of Contents I. Policy Section SP-EFF-PL-01--Effort Reporting II. Procedure Section SP-EFF-PR-01--Effort

Trinity Valley Community College. Grants Accounting Policy and Procedures 2012

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

Guidance on Effort Reporting and Certification Policies

1. Title 2. Policy Guidance on Effort Reporting and Certification Policies Sec. 1 Sec. 2 Sec. 3 Sec. 4 Purpose. The purpose of this Policy is to identify the fundamentals of The University of Texas System

1. Title 2. Policy Guidance on Effort Reporting and Certification Policies Sec. 1 Sec. 2 Sec. 3 Sec. 4 Purpose. The purpose of this Policy is to identify the fundamentals of The University of Texas System

INDIRECT COST POLICY

UNIVERSITY OF LOUISIANA AT LAFAYETTE OFFICE OF THE VICE PRESIDENT FOR RESEARCH INDIRECT COST POLICY Revision Date: 8/11/2014 Original Effective Date: 11/08/2006 Responsible Office: Reference: Vice President

UNIVERSITY OF LOUISIANA AT LAFAYETTE OFFICE OF THE VICE PRESIDENT FOR RESEARCH INDIRECT COST POLICY Revision Date: 8/11/2014 Original Effective Date: 11/08/2006 Responsible Office: Reference: Vice President

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS. AOA Conference Sacramento, CA January 12, 2014

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS AOA Conference Sacramento, CA January 12, 2014 Agenda 1. Introduction 2. History 3. Learning Objectives 4.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS AOA Conference Sacramento, CA January 12, 2014 Agenda 1. Introduction 2. History 3. Learning Objectives 4.

Joint Statement of Policies & Procedures for Administering Grants and Contracts

Joint Statement of Policies & Procedures for Administering Grants and Contracts The University Corporation and The Office of Research & Sponsored Programs June 02, 2004 Table of Contents I. MISSION 1 II.

Joint Statement of Policies & Procedures for Administering Grants and Contracts The University Corporation and The Office of Research & Sponsored Programs June 02, 2004 Table of Contents I. MISSION 1 II.

Fiscal Compliance Training Series: Charging Salaries Travel Expenses

Fiscal Compliance Training Series: Charging Salaries Travel Expenses Wed., April 26, 2017, 2:00 pm to 3:00 pm Curry Student Center, Room No. 318-320-322 Fiscal Management Lifecycle 2 Conduct Research and

Fiscal Compliance Training Series: Charging Salaries Travel Expenses Wed., April 26, 2017, 2:00 pm to 3:00 pm Curry Student Center, Room No. 318-320-322 Fiscal Management Lifecycle 2 Conduct Research and

Match and Leveraged Resources

Match and Leveraged Resources Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, Designed requirements for DOL-ETA governing direct cost recipients principles, and administrative their subrecipients

Match and Leveraged Resources Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, Designed requirements for DOL-ETA governing direct cost recipients principles, and administrative their subrecipients

Fiscal Compliance Requirements for Sponsored Programs Allowable Costs per A 21. University of Missouri System Published 2009

Fiscal Compliance Requirements for Sponsored Programs Allowable Costs per A 21 University of Missouri System Published 2009 Learning Objectives To understand: Allowable cost compliance requirements Responsibilities

Fiscal Compliance Requirements for Sponsored Programs Allowable Costs per A 21 University of Missouri System Published 2009 Learning Objectives To understand: Allowable cost compliance requirements Responsibilities

Cultural Competency Initiative. Program Guidelines

New Jersey STOP Violence Against Women (VAWA) Grants Program Cultural Competency Initiative Cultural Competency Technical Assistance Project Program Guidelines State Office of Victim Witness Advocacy Division

New Jersey STOP Violence Against Women (VAWA) Grants Program Cultural Competency Initiative Cultural Competency Technical Assistance Project Program Guidelines State Office of Victim Witness Advocacy Division

HENDERSHOT, BURKHARDT & ASSOCIATES CERTIFIED PUBLIC ACCOUNTANTS

Young Marines of the Marine Corps League Financial Statements for the Year Ended September 30, 2016 and Independent Auditors Report Dated March 8, 2017 HENDERSHOT, BURKHARDT & ASSOCIATES CERTIFIED PUBLIC

Young Marines of the Marine Corps League Financial Statements for the Year Ended September 30, 2016 and Independent Auditors Report Dated March 8, 2017 HENDERSHOT, BURKHARDT & ASSOCIATES CERTIFIED PUBLIC

University of Colorado Denver

University of Colorado Denver Campus Guidelines Title:, 4-13 Source: Prepared by: Approved by: Office of Grants and Contracts Director, Office of Grants and Contracts Vice Chancellor for Research Effective

University of Colorado Denver Campus Guidelines Title:, 4-13 Source: Prepared by: Approved by: Office of Grants and Contracts Director, Office of Grants and Contracts Vice Chancellor for Research Effective

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews Denise Dusek, MPA Federal Funding Specialist ESC 20 Image obtained from google.com Education Service Center, Region 20 May 2018 2 1 Participants

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews Denise Dusek, MPA Federal Funding Specialist ESC 20 Image obtained from google.com Education Service Center, Region 20 May 2018 2 1 Participants

University of North Carolina Finance Improvement & Transformation Contracts and Grants Standards. January 2015 Version 8

University of North Carolina Finance Improvement & Transformation Contracts and Grants Standards January 2015 Version 8 Table of Contents Introduction.......3 Account Setup.....10 Time and Effort Reporting......14

University of North Carolina Finance Improvement & Transformation Contracts and Grants Standards January 2015 Version 8 Table of Contents Introduction.......3 Account Setup.....10 Time and Effort Reporting......14

The State of Texas HELP AMERICA VOTE ACT PROVIDE THE SAME OPPORTUNITY FOR ACCESS AND PARTICIPATION TO INDIVIDUALS WITH DISABILITIES

The State of Texas Elections Division Phone: 512-463-5650 P.O. Box 12060 Fax: 512-475-2811 Austin, Texas 78711-2060 TTY: 7-1-1 www.sos.state.tx.us (800) 252-VOTE (8683) The Office of The Secretary of State

The State of Texas Elections Division Phone: 512-463-5650 P.O. Box 12060 Fax: 512-475-2811 Austin, Texas 78711-2060 TTY: 7-1-1 www.sos.state.tx.us (800) 252-VOTE (8683) The Office of The Secretary of State

SJSU Research Foundation Cost Share Policy

SJSU Research Foundation Cost Share Policy Office of Sponsored Programs Policy No.: Effective Date: Supersedes: n/a Publication Date: OSP. 03-04-001 Rev. A 05/01/2017 6/29/2017 1.0 Purpose The Cost Share

SJSU Research Foundation Cost Share Policy Office of Sponsored Programs Policy No.: Effective Date: Supersedes: n/a Publication Date: OSP. 03-04-001 Rev. A 05/01/2017 6/29/2017 1.0 Purpose The Cost Share

University of Pittsburgh SPONSORED PROJECT FINANCIAL GUIDELINE Subject: SUBRECIPIENT MONITORING

I. Scope Subrecipient monitoring is the process by which the University selects, monitors, controls, and accounts for University subcontractors or subrecipients utilized on sponsored projects in accordance

I. Scope Subrecipient monitoring is the process by which the University selects, monitors, controls, and accounts for University subcontractors or subrecipients utilized on sponsored projects in accordance

TEXAS TECH UNIVERSITY HEALTH SCIENCES CENTER EL PASO

TEXAS TECH UNIVERSITY HEALTH SCIENCES CENTER EL PASO Operating Policy and Procedure HSCEP OP: PURPOSE: REVIEW: 65.07, Effort Reporting: Certifying Time and Effort on Sponsored Projects The purpose of this

TEXAS TECH UNIVERSITY HEALTH SCIENCES CENTER EL PASO Operating Policy and Procedure HSCEP OP: PURPOSE: REVIEW: 65.07, Effort Reporting: Certifying Time and Effort on Sponsored Projects The purpose of this

EASTERN MICHIGAN UNIVERSITY. Sponsored Research Accounting Cost Share Guidelines

EASTERN MICHIGAN UNIVERSITY Sponsored Research Accounting Cost Share Guidelines PURPOSE: The purpose for the Cost Share Guidelines is to articulate the roles and responsibilities of the various parties

EASTERN MICHIGAN UNIVERSITY Sponsored Research Accounting Cost Share Guidelines PURPOSE: The purpose for the Cost Share Guidelines is to articulate the roles and responsibilities of the various parties

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

Auburn University. Contracts and Grants Accounting

Auburn University Contracts and Grants Accounting Introduction to Contracts and Grants Accounting Contracts and grants are important to Auburn University. Much of the research that Auburn faculty, staff,

Auburn University Contracts and Grants Accounting Introduction to Contracts and Grants Accounting Contracts and grants are important to Auburn University. Much of the research that Auburn faculty, staff,

Felipe Lopez, Vavrinek, Trine, Day & Co., LLP

San Luis Obispo County Community College District & San Luis Obispo County Office of Education 2012 F d l C li T i i 2012 Federal Compliance Training Felipe Lopez, Vavrinek, Trine, Day & Co., LLP Objectives

San Luis Obispo County Community College District & San Luis Obispo County Office of Education 2012 F d l C li T i i 2012 Federal Compliance Training Felipe Lopez, Vavrinek, Trine, Day & Co., LLP Objectives

IL Talent Pipeline Management. Highlighted Grant Requirements 7/30/15 & 8/3/15

IL Talent Pipeline Management Highlighted Grant Requirements 7/30/15 & 8/3/15 State Budget Impact on Grants The DCEO Accounting Office has confirmed that grantees will be able to incur costs per the terms

IL Talent Pipeline Management Highlighted Grant Requirements 7/30/15 & 8/3/15 State Budget Impact on Grants The DCEO Accounting Office has confirmed that grantees will be able to incur costs per the terms

Understanding and Complying with Government Grants

Presents... Understanding and Complying with Objectives Obtain information to determine if applying for governmental grants is appropriate for your organization Obtain understanding of internal controls

Presents... Understanding and Complying with Objectives Obtain information to determine if applying for governmental grants is appropriate for your organization Obtain understanding of internal controls

If a 20% Match Is Required:

NON-FEDERAL SHARE: A Programmatic & Fiscal Approach If a 20% Match Is Required: (a) Divide the total Federal funds by 80% to determine total project costs; (b) Subtract the Federal portion from the total

NON-FEDERAL SHARE: A Programmatic & Fiscal Approach If a 20% Match Is Required: (a) Divide the total Federal funds by 80% to determine total project costs; (b) Subtract the Federal portion from the total

UNIFORM GUIDANCE OVERVIEW. Budget Officers Meeting January 28, 2015

UNIFORM GUIDANCE OVERVIEW Budget Officers Meeting January 28, 2015 OMB Circulars Before and After Eight circulars condensed to one new comprehensive set of requirements for recipients of federal awards

UNIFORM GUIDANCE OVERVIEW Budget Officers Meeting January 28, 2015 OMB Circulars Before and After Eight circulars condensed to one new comprehensive set of requirements for recipients of federal awards

EXHIBIT A SPECIAL PROVISIONS

EXHIBIT A SPECIAL PROVISIONS The following provisions supplement or modify the provisions of Items 1 through 9 of the Integrated Standard Contract, as provided herein: A-1. ENGAGEMENT, TERM AND CONTRACT

EXHIBIT A SPECIAL PROVISIONS The following provisions supplement or modify the provisions of Items 1 through 9 of the Integrated Standard Contract, as provided herein: A-1. ENGAGEMENT, TERM AND CONTRACT

NOVA SOUTHEASTERN UNIVERSITY

NOVA SOUTHEASTERN UNIVERSITY DIVISION OF RESPONSIBILITIES FOR RESEARCH AND SPONSORED PROGRAMS Vice President of Research & Technology Transfer: The responsibilities of the Vice President of Research &

NOVA SOUTHEASTERN UNIVERSITY DIVISION OF RESPONSIBILITIES FOR RESEARCH AND SPONSORED PROGRAMS Vice President of Research & Technology Transfer: The responsibilities of the Vice President of Research &

Vanderbilt University Policy for Cost Sharing on Sponsored Projects

Vanderbilt University Policy for Cost Sharing on Sponsored Projects Effective January 1, 2002 (Updated December 2009) and approved by: Jeff Balser, Vice Chancellor for Health Affairs, Dean of the School

Vanderbilt University Policy for Cost Sharing on Sponsored Projects Effective January 1, 2002 (Updated December 2009) and approved by: Jeff Balser, Vice Chancellor for Health Affairs, Dean of the School

PROGRAM INSTRUCTION. Texas Department of Aging and Disability Services (DADS) Access and Intake Division

Access and Intake Division") PROGRAM INSTRUCTION Texas Department of Aging and Disability Services (DADS) Access and Intake Division TITLE: Administering Program Income NUMBER: AAA-PI 304 SECTION: Area Agencies on Aging APPROVAL:

PROGRAM INSTRUCTION Texas Department of Aging and Disability Services (DADS) Access and Intake Division TITLE: Administering Program Income NUMBER: AAA-PI 304 SECTION: Area Agencies on Aging APPROVAL:

Effective: April 1, 2016

Office of Sponsored Projects Policy on Cost Sharing on Sponsored Projects Effective: April 1, 2016 Authored by: Jerry Fife Associate Vice President for Sponsored Projects Purpose This policy has been developed

Office of Sponsored Projects Policy on Cost Sharing on Sponsored Projects Effective: April 1, 2016 Authored by: Jerry Fife Associate Vice President for Sponsored Projects Purpose This policy has been developed

HUMBOLDT STATE UNIVERSITY SPONSORED PROGRAMS FOUNDATION

HUMBOLDT STATE UNIVERSITY SPONSORED PROGRAMS FOUNDATION BASIC FINANCIAL STATEMENTS, SUPPLEMENTARY INFORMATION, AND SINGLE AUDIT REPORTS Including Schedules Prepared for Inclusion in the Financial Statements

HUMBOLDT STATE UNIVERSITY SPONSORED PROGRAMS FOUNDATION BASIC FINANCIAL STATEMENTS, SUPPLEMENTARY INFORMATION, AND SINGLE AUDIT REPORTS Including Schedules Prepared for Inclusion in the Financial Statements