Jason Galloway, Associate Controller HSC Contract and Grant Accounting

|

|

|

- Ezra Burns

- 6 years ago

- Views:

Transcription

1 Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting

2

3 New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable to Grants, Contracts and Other Agreements with Educational Institutions A-110 Uniform Administrative Requirements for Grants and Agreements with Institutions of Higher Education, Hospitals, and Other Non-Profit Organizations A-133 Audits of States, Local Governments, and Non-Profit Organizations 2 CFR 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Effective December 26, 2014

4 Why Uniform Guidance? Goals and Objectives To reform and streamline guidance for all Federal Awards To ease administrative burden To strengthen oversight To reduce fraud, waste and abuse To eliminate duplicative and conflicting guidance To provide for consistent and transparent treatment of costs

5 Uniform Guidance Electronic Code of Federal Regulation Code of Federal Regulations Title 2, Subtitle A, Chapter II, Part 200 Supersedes and streamlines requirements from eight different grant circulars into one set of regulations Made up of six subparts A through F ecfr - Code of Federal Regulation

6 Uniform Guidance Made up of six subparts: Subpart A Acronyms and Definitions Subpart B General Provisions Subpart C Pre-Federal Award Requirements and Contents of Federal Awards Subpart D Post Federal Award Requirements Subpart E Cost Principles Subpart F Audit Requirements

7 A-21 vs. 2 CFR 200 Which do I follow? New awards and supplements should be using the new guidance now Review your award terms and conditions! (HHS) If your award was dated after December 26, 2014 it will most likely be under the new guidance Old regulations = 45 CFR Part 74 or Part 92 New regulations = 45 CFR Part 75

8 Uniform Guidance Changes Definitions Should vs Must Must = REQUIRED Should = Best practices or recommended approach

9 Subrecipient Monitoring This section provides detailed monitoring procedures such as reviewing financial and programmatic reports, performing on-site reviews, and engaging external auditor to perform agreed-uponprocedures for Subrecipient monitoring. Risk Assessment and documentation of subrecipient Reviewing financial and programmatic reports as required by UNM. It is the responsibility of the PI to ensure the programmatic requirements are met prior to approving invoices. Subrecipient invoice payments must be made with 30 days.

10 Can I Charge that to my Grant? Answer: It Depends!!

11 OMB Circular A-21 & 2 CFR 200 Subpart E The Cost Principles Define criteria for charging costs Define direct costs and indirect costs Discuss selected items of costs Determine calculation of indirect cost rate

12 COST ACCOUNTING STANDARDS BOARD (CASB) 501 Consistency in Reporting Costs 502 Consistency in Allocating Costs 505 Accounting for Unallowable Costs 506 Consistency in Cost Accounting Period A-21 Appendix A & 2 CFR

13 Factors Affecting Charging of Costs or The Golden Rules Must be reasonable Prudent person test what would a reasonable person do in a similar situation? Necessary to the project Adhere to all applicable laws and regulations Adheres to terms and conditions of sponsor and award Consistent with policies and practices applied uniformly to Federal and University funds A-21 C.3 & 2 CFR ,

14 Newspaper Test Contemplating any business act, an employee should ask himself whether he would be willing to see it immediately described by an informed and critical reporter on the front page of his local paper, there to be read by his spouse, children and friends. -Warren E. Buffett

15 Factors Affecting Charging of Costs Must be allowable Costs must conform to any limitations or exclusions set forth in the cost principles or in the sponsored agreement as to types or amounts of cost. See A-21 C.2(d) & 2 CFR The award s terms and conditions General Provisions for Selected Items of Cost - A-21 Sec. J.1 J.54 & 2 CFR

16 Factors Affecting Charging of Costs Must be allocable Goods or services involved are chargeable or assignable in accordance with relative benefits received or other equitable relationship Cost is incurred solely to advance the work, or Cost benefits both sponsored agreement & other work in proportions that can be approximated by reasonable methods, or Cost is necessary to the overall operation of institution & is deemed to be assignable in part to sponsored projects, and No shifting of costs from one fund to another to cover cost overruns, avoid restrictions on agreement or for reasons of convenience A-21 C.4 & 2 CFR

17 Factors Affecting Charging of Costs Must be consistently treated -Consistency in proposing, charging and reporting costs -Consistently charged in similar circumstances as a direct cost or an indirect cost A-21 C.2(c), D.1, Appendix A & 2 CFR , , (a)

18 Consistent Treatment (d) states: "A cost may not be assigned to a Federal award as a direct cost if any other cost incurred for the same purpose in like circumstances has been allocated to the Federal award as an indirect cost."

19 Cost Share (f) states: "Not be included as a cost or used to meet cost sharing or matching requirements of any other federally-financed program in either the current or a prior period. See also Cost sharing or matching paragraph (b)."

20 What does Allowable mean?? The fact that a cost requested in a budget is awarded, as requested, does not ensure a determination of allowability. The organization is responsible for presenting costs consistently and must not include costs associated with their F&A rate as direct costs. - NIH Grants Policy Statement

21 Can this be charged to the Grant? If a cost cannot meet the criteria of reasonableness, allowability, allocability, and consistency, it is unallowable. Remember, if it is not allowable on a sponsored fund, then it is not allowable on a cost share account.

22 Direct Cost Definition 2 CFR Direct costs are those costs that can be identified specifically with a particular final cost objective, such as a Federal award, or other internally or externally funded activity, or that can be directly assigned to such activities relatively easily with a high degree of accuracy. Costs incurred for the same purpose in like circumstances must be treated consistently as either direct or indirect (F&A) costs. See also Allocable costs.

23 Examples of Direct Costs Salaries of researchers/project directors (including benefit costs) Laboratory/project supplies Travel Technicians Animal housing/care

24 Special Circumstances-Old Extensive data accumulation, analysis, entry Large amounts of travel/meeting arrangements Large, complex programs Remote field projects that cannot access normal departmental services Major projects, e.g. General Clinical Research Centers, center grants, program project grants... Training grants Sponsored projects not supported, in whole or in part, by federal funds

25 Special Circumstances-New If special circumstances exist, an F&A cost may be budgeted as a direct cost provided that the cost is: Allowable Identified specifically with a proposed project and will advance the proposed work Cost can be attributed to the proposed project with relative ease and a high degree of accuracy

26 A Special Note About Clerical Support A-21, Exhibit C Examples of "major projects" where direct charging admin or clerical staff salaries may be appropriate. 2 CFR Staff should normally be treated as indirect (F&A) costs. Direct charging may be appropriate if: (1) Integral to the project; (2) Specifically identified with project; and (3) Explicitly included in budget or with agency s prior written approval

27 A Special Note About Computing Devices 2 CFR (c) Materials and supplies used for the performance of a Federal award may be charged as direct costs. In the specific case of computing devices, charging as direct costs is allowable for devices that are essential and allocable, but not solely dedicated, to the performance of a Federal award.

28 Document! Document! Document! Document!

29 Why the need for documentation? Auditors will expect documentation on all transactions. Especially those considered under exceptional circumstances or for major projects. Receipts with enough detail to support the charge Written explanation of how the expense benefited the project(s) If you leave the university or department is there sufficient detail that the documentation can speak for itself?

30 Where do you go for answers? 2 CFR 200 Subpart E of the Uniform Guidance OMB Circular A-21 Agency Rules/Guidelines Program Specific Guidelines Award Document Special Conditions Institutional Policy Consult with your Fiscal Monitor and C&G Accounting

http://sarm.")

31 Helpful Hint See University s Standard Accounting Resource Manual (SARM)

32 Allowable or Unallowable You Decide

33 Case Study 1 Your PI has a U-54 grant that requires a great deal of support in arranging travel for the project leaders from several universities, and internal research projects to attend semi-annual progress meetings. The PI also is coordinating the preparation and submission of several publications and the planning of four separate seminars related to the grant. Do you think he can charge for administrative/clerical services on the grant?

34 Case Study 2 A PI invited his co-investigator on his Grant, (an expert in the field you are working in and is from another university), to give a talk to your university staff/faculty about the unique discovery they have made on their project. After the seminar the PI and several other faculty members have dinner with the speaker at a local restaurant before their flight home. What, if any, expenses incurred can be charged to the Grant?

35 UNACCEPTABLE PRACTICES Purchasing items to exhaust unobligated balances. Rotating charges among projects. Assigning charges on the basis of the remaining balance to resolve availability of funding issues or to avoid loss of carry-forward balances.

36 UNACCEPTABLE PRACTICES Assigning charges to an award before the cost is incurred. Charging an expense exclusively to a single award when the expense clearly has supported other activities. Applying a unit "tax" to projects to distribute clerical and administrative expenses. Transferring an overdraft from one sponsored project to another, without express sponsor approval.

37 False Claims Act Under the U.S. False Claims Act, persons working with federal funds are prohibited from knowingly presenting, or causing to be presented, to an officer or employee of the U.S. Government or a member of the Armed Forces of the U.S. a false or fraudulent claim for payment or approval. (VII.J.)

38 What s the worst that can happen?

39 Non-Compliance can lead to: Disallowed Costs Reduction in Funding Award Termination Additional Compliance Requirements/Oversight Sanctions Suspension Debarment Criminal Penalties

40 Non-Compliance can lead to:

41 Non-Compliance can lead to:

42 Non-Compliance can lead to:

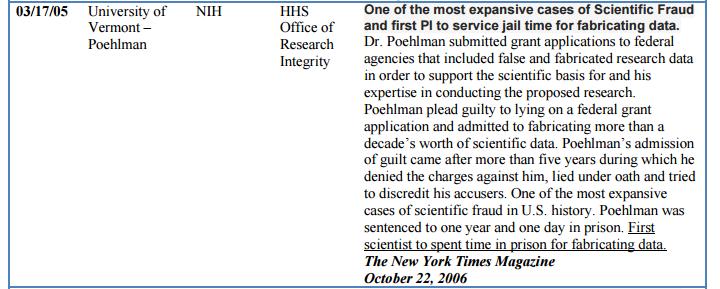

43 References 2 CFR 200 Subpart E OMB Circular A-21 False Claims Act New York Times Magazine October 22, An Unwelcome Discovery Summary of University Audits, Settlements & Investigations Related to Federal Programs Published audit findings NSF External Reports NIH Office of Audit Service oig.hhs.gov/reports-and-publications/oas/nih.asp NCURA 16 th Annual Meeting for FRAs Can I Charge this item to a Grant? Glenda A. Bullock

44 Questions?

Federal Rules for Sponsored Programs. Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY. Office of Contracts and Grants December, 2014

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014 2 CFR 200 - OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial

Uniform Guidance Sponsored Projects Services

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance)

") Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

University of Pittsburgh

I. Guideline Background University sponsors are increasingly relying on institutions for the development of adequate compliance programs for the financial administration of grants and contracts. An adequate

I. Guideline Background University sponsors are increasingly relying on institutions for the development of adequate compliance programs for the financial administration of grants and contracts. An adequate

Diane Dean, Director Kathy Hancock, Assistant Grants Compliance Officer Joel Snyderman, Assistant Grants Compliance Officer

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar San Diego, CA October 2015 Diane Dean,

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar San Diego, CA October 2015 Diane Dean,

Uniform Guidance Update. Ruth Boardman, Associate Director Office of Grants and Contracts March 2015

Uniform Guidance Update Ruth Boardman, Associate Director Office of Grants and Contracts March 2015 Objectives Latest Updates Internal Controls Procurement Status of Policies and Procedures Research Terms

Uniform Guidance Update Ruth Boardman, Associate Director Office of Grants and Contracts March 2015 Objectives Latest Updates Internal Controls Procurement Status of Policies and Procedures Research Terms

OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN

TO 2 CFR 200 (UNIFORM ADMIN") Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Uniform Guidance and Compliance

Uniform Guidance and Compliance Office of Research Author: Mariel Diaz Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Uniform Guidance Award Management

Uniform Guidance and Compliance Office of Research Author: Mariel Diaz Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Uniform Guidance Award Management

University of Pittsburgh

I. Scope This guideline establishes the requirements for recording direct and indirect costs on the financial accounting records of the University in accordance with Federal regulations and generally accepted

I. Scope This guideline establishes the requirements for recording direct and indirect costs on the financial accounting records of the University in accordance with Federal regulations and generally accepted

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. AUSPAN Martha Taylor

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar Chicago, IL October 2016 Diane Dean, Director

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar Chicago, IL October 2016 Diane Dean, Director

The Uniform Guidance (2 CFR, Part 200)

") WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

Policy on Cost Allocation, Cost Recovery, and Cost Sharing

President Page 1 of 11 PURPOSE: Provide guidance and structure when allocating and documenting costs (direct and indirect) for extramurally funded awards. Serves to provide direction for budgeting, allocating

President Page 1 of 11 PURPOSE: Provide guidance and structure when allocating and documenting costs (direct and indirect) for extramurally funded awards. Serves to provide direction for budgeting, allocating

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT)

") GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

Office of Sponsored Programs Budgetary and Cost Accounting Procedures

Office of Sponsored Programs Budgetary and Cost Accounting Procedures Table of Contents 1. Purpose and Services 2. Definitions of Terms 3. Budget Items 4. Travel 5. Effort Certification Reporting 6. Costing

Office of Sponsored Programs Budgetary and Cost Accounting Procedures Table of Contents 1. Purpose and Services 2. Definitions of Terms 3. Budget Items 4. Travel 5. Effort Certification Reporting 6. Costing

Overview of the New EDGAR (formerly the Uniform Grants Guidance)

") Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Fiscal Compliance Requirements for Sponsored Programs Allowable Costs per A 21. University of Missouri System Published 2009

Fiscal Compliance Requirements for Sponsored Programs Allowable Costs per A 21 University of Missouri System Published 2009 Learning Objectives To understand: Allowable cost compliance requirements Responsibilities

Fiscal Compliance Requirements for Sponsored Programs Allowable Costs per A 21 University of Missouri System Published 2009 Learning Objectives To understand: Allowable cost compliance requirements Responsibilities

3 rd Annual Symposium for Research Administrators

3 rd Annual Symposium for Research Administrators Cost Transfer Policy Martha Martin, CRA, Grants Administration, School of Information and Library Science Sarah Van Heusen, MHA, Director of Research Administration,

3 rd Annual Symposium for Research Administrators Cost Transfer Policy Martha Martin, CRA, Grants Administration, School of Information and Library Science Sarah Van Heusen, MHA, Director of Research Administration,

GEORGE MASON UNIVERSITY OFFICE SPONSORED PROGRAMS. Matt Kluger, Vice President for Research & Economic Development

GEORGE MASON UNIVERSITY OFFICE SPONSORED PROGRAMS Memo to: From: Subject: Principal Investigators on Federal Sponsored Projects Unit Research Administrators Research Associate Deans Deans and Directors

GEORGE MASON UNIVERSITY OFFICE SPONSORED PROGRAMS Memo to: From: Subject: Principal Investigators on Federal Sponsored Projects Unit Research Administrators Research Associate Deans Deans and Directors

Uniform Guidance. Overview and Implementation Plan. November 21, 2014

Uniform Guidance Overview and Implementation Plan November 21, 2014 Uniform Guidance. Change is coming! College or Department name here 1 Overarching goal of the reform is to: streamline the rules and

Uniform Guidance Overview and Implementation Plan November 21, 2014 Uniform Guidance. Change is coming! College or Department name here 1 Overarching goal of the reform is to: streamline the rules and

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. AU SPAN Martha Taylor Larry Hankins

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AU SPAN 6 23 2014 Martha Taylor Larry Hankins Grants Reform February 2011 President directed OMB to reduce

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AU SPAN 6 23 2014 Martha Taylor Larry Hankins Grants Reform February 2011 President directed OMB to reduce

Roadmap to the Uniform Grant Guidance for School Districts

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

UNIFORM GUIDANCE IMPLEMENTATION

UNIFORM GUIDANCE IMPLEMENTATION Presented by Sara Judd, OSR Consultant October 2014 Uniform Guidance Implementation what we know and what we re guessing Ready, Set, Go 2014 Fred Hutchinson Cancer Research

UNIFORM GUIDANCE IMPLEMENTATION Presented by Sara Judd, OSR Consultant October 2014 Uniform Guidance Implementation what we know and what we re guessing Ready, Set, Go 2014 Fred Hutchinson Cancer Research

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs

3/15/14 Draft Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs Prepared for the Council of Chief State School Officers Federal

3/15/14 Draft Summary of the Office of Management and Budget s Uniform Guidance for Federal Grants and its Impact on Federal Education Programs Prepared for the Council of Chief State School Officers Federal

Are You Ready for This? The New Uniform Guidance 2 CFR 200

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

The OmniCircular - 2 CFR 200

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Preparing campus for what is changing and what is not What is Grants Reform and when is it effective? What

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Preparing campus for what is changing and what is not What is Grants Reform and when is it effective? What

FY2016 Grant Application Workshop. Basics of Financial Management for Grant Applicants

FY2016 Grant Application Workshop Basics of Financial Management for Grant Applicants Jerron M. Johnson Chief Field Program Officer Missouri Community Service Commission November 19, 2015 Session Overview

FY2016 Grant Application Workshop Basics of Financial Management for Grant Applicants Jerron M. Johnson Chief Field Program Officer Missouri Community Service Commission November 19, 2015 Session Overview

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS. AOA Conference Sacramento, CA January 12, 2014

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS AOA Conference Sacramento, CA January 12, 2014 Agenda 1. Introduction 2. History 3. Learning Objectives 4.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS AOA Conference Sacramento, CA January 12, 2014 Agenda 1. Introduction 2. History 3. Learning Objectives 4.

Federal Grants Compliance Training

Federal Grants Compliance Training Agenda Overview of cost principles Allocating expenses between grants Timely reimbursement of expenses Participant support costs Summer salary calculations Fly America

Federal Grants Compliance Training Agenda Overview of cost principles Allocating expenses between grants Timely reimbursement of expenses Participant support costs Summer salary calculations Fly America

Subcontract Monitoring

Subcontract Monitoring Subcontract definition Uniform Guidance (UG) 200.330-332 Subrecipient means a non-federal entity that expends Federal awards received from a passthrough entity to carry out a Federal

Subcontract Monitoring Subcontract definition Uniform Guidance (UG) 200.330-332 Subrecipient means a non-federal entity that expends Federal awards received from a passthrough entity to carry out a Federal

RACE TO THE TOP EARLY LEARNING CHALLENGE

APRIL 2015 84.412 RACE TO THE TOP EARLY LEARNING CHALLENGE State Project/Program: Federal Authorization: State Authorization: RACE TO THE TOP EARLY LEARNING CHALLENGE U. S. DEPARTMENT OF EDUCATION PL 111-5

APRIL 2015 84.412 RACE TO THE TOP EARLY LEARNING CHALLENGE State Project/Program: Federal Authorization: State Authorization: RACE TO THE TOP EARLY LEARNING CHALLENGE U. S. DEPARTMENT OF EDUCATION PL 111-5

OMB Uniform Guidance ( UG ) Briefing. ASRSP & OSR Brown Bag Tuesday, January 27 th

Briefing. ASRSP & OSR Brown Bag Tuesday, January 27 th") OMB Uniform Guidance ( UG ) Briefing ASRSP & OSR Brown Bag Tuesday, January 27 th Background The UG is the single biggest regulatory change in the last fifty years in research administration Interesting

OMB Uniform Guidance ( UG ) Briefing ASRSP & OSR Brown Bag Tuesday, January 27 th Background The UG is the single biggest regulatory change in the last fifty years in research administration Interesting

SUMMARY. Extramural Funds Accounting effectively conducts post award financial management:

SUMMARY Extramural Funds Accounting assists campus faculty and staff in meeting their teaching, research, and operational needs by providing quality financial services for externally funded projects. Protecting

SUMMARY Extramural Funds Accounting assists campus faculty and staff in meeting their teaching, research, and operational needs by providing quality financial services for externally funded projects. Protecting

Here Come the Feds! What a Sponsor Audit is Looking for and How to Prepare Your Institution

Here Come the Feds! What a Sponsor Audit is Looking for and How to Prepare Your Institution Presented by: Richard Cordova, University of Washington Kevin Robinson, Auburn University Kim Ginn, Baker Tilly

Here Come the Feds! What a Sponsor Audit is Looking for and How to Prepare Your Institution Presented by: Richard Cordova, University of Washington Kevin Robinson, Auburn University Kim Ginn, Baker Tilly

The Metis Foundation Office of Grant and Contract Administration SUBRECIPIENT INFORMATION AND COMPLIANCE FORM

The Metis Foundation Office of Grant and Contract Administration SUBRECIPIENT INFORMATION AND COMPLIANCE FORM All subrecipients must complete this form when submitting a proposal to the Metis Foundation

The Metis Foundation Office of Grant and Contract Administration SUBRECIPIENT INFORMATION AND COMPLIANCE FORM All subrecipients must complete this form when submitting a proposal to the Metis Foundation

Vanderbilt University. Direct Cost. Guidelines for Budgeting and Charging Direct Costs on Sponsored Projects

Vanderbilt University Direct Cost Guidelines for Budgeting and Charging Direct Costs on Sponsored Projects 1 Table of Contents Flowchart Illustration Introduction Roles and Responsibilities Direct Costs:

Vanderbilt University Direct Cost Guidelines for Budgeting and Charging Direct Costs on Sponsored Projects 1 Table of Contents Flowchart Illustration Introduction Roles and Responsibilities Direct Costs:

Financial Oversight of Sponsored Projects

Financial Oversight of Sponsored Projects Today s Agenda Introduction Reasons for Principal Investigator Oversight Sponsor and University Policies General Considerations Unallowable Costs Re-Budgeting

Financial Oversight of Sponsored Projects Today s Agenda Introduction Reasons for Principal Investigator Oversight Sponsor and University Policies General Considerations Unallowable Costs Re-Budgeting

Guidance on Effort Reporting and Certification Policies

1. Title 2. Policy Guidance on Effort Reporting and Certification Policies Sec. 1 Sec. 2 Sec. 3 Sec. 4 Purpose. The purpose of this Policy is to identify the fundamentals of The University of Texas System

1. Title 2. Policy Guidance on Effort Reporting and Certification Policies Sec. 1 Sec. 2 Sec. 3 Sec. 4 Purpose. The purpose of this Policy is to identify the fundamentals of The University of Texas System

University of Pittsburgh SPONSORED PROJECT FINANCIAL GUIDELINE Subject: SUBRECIPIENT MONITORING

I. Scope Subrecipient monitoring is the process by which the University selects, monitors, controls, and accounts for University subcontractors or subrecipients utilized on sponsored projects in accordance

I. Scope Subrecipient monitoring is the process by which the University selects, monitors, controls, and accounts for University subcontractors or subrecipients utilized on sponsored projects in accordance

POLICY STATEMENT EFFECTIVE DATE

Policy Section: Office of Research and Project Administration & Sponsored Research Accounting Policy Number and Title: Charging of Administrative or Clerical Salaries and General Expenses to Federal Sponsored

Policy Section: Office of Research and Project Administration & Sponsored Research Accounting Policy Number and Title: Charging of Administrative or Clerical Salaries and General Expenses to Federal Sponsored

FAQ S FOR UNIFORM GUIDANCE

FAQ S FOR UNIFORM GUIDANCE As Uniform Guidance (UG) and its implications continue to be defined, the Fred Hutch UG Team will release a series of Frequently Asked Questions (FAQs) to clarify current standings.

FAQ S FOR UNIFORM GUIDANCE As Uniform Guidance (UG) and its implications continue to be defined, the Fred Hutch UG Team will release a series of Frequently Asked Questions (FAQs) to clarify current standings.

The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

RESEARCH ADMINISTRATION FORUM Allowable Costs. Uniform Guide

RESEARCH ADMINISTRATION FORUM Allowable Costs Uniform Guide Objectives Understand what are allowable and unallowable costs to Federal grants Understand the importance of properly budgeting for costs on

RESEARCH ADMINISTRATION FORUM Allowable Costs Uniform Guide Objectives Understand what are allowable and unallowable costs to Federal grants Understand the importance of properly budgeting for costs on

Federal Grant Guidance Compliance

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

Dollars & Sense: Federal Grant Financial

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

Building Your Foundation: Administrative Requirements Boot Camp (Modules 1-8: Administrative Requirements for Non-Federal Entities)

") Course #400 Syllabus Grant Management Boot Camp (Covers 12 Grant Management Modules) This Boot Camp bundle includes 12 Grants Management training courses including 8 modules on the Administrative Requirements

Course #400 Syllabus Grant Management Boot Camp (Covers 12 Grant Management Modules) This Boot Camp bundle includes 12 Grants Management training courses including 8 modules on the Administrative Requirements

ADMINISTRATIVE PRACTICE LETTER

Page(s) 1 of 6 Index Purpose of Guidelines Policy Who is Responsible Definitions and Terms Responsibilities and Procedures o University of Maine System Administration o Sponsored Programs Office o Employee,

Page(s) 1 of 6 Index Purpose of Guidelines Policy Who is Responsible Definitions and Terms Responsibilities and Procedures o University of Maine System Administration o Sponsored Programs Office o Employee,

FINANCE-315 7/1/2017 SUBRECIPIENT COMMITMENT FORM

SUBRECIPIENT COMMITMENT FORM All subrecipients should complete this form when submitting a proposal to UACES. It provides a checklist of documents and certifications required by sponsors, as well as an

SUBRECIPIENT COMMITMENT FORM All subrecipients should complete this form when submitting a proposal to UACES. It provides a checklist of documents and certifications required by sponsors, as well as an

Federal Grants Compliance 101

Federal Grants Compliance 101 June 4, 2014 YOUR MISSION OUR SOLUTIONS Huron Consulting Group Inc. All Rights Reserved. Huron is a management consulting firm and not a CPA firm, and does not provide attest

Federal Grants Compliance 101 June 4, 2014 YOUR MISSION OUR SOLUTIONS Huron Consulting Group Inc. All Rights Reserved. Huron is a management consulting firm and not a CPA firm, and does not provide attest

Navigating the New Uniform Grant Guidance. Jack Reagan, Audit Partner Grant Thornton LLP. Grant Thornton. All rights reserved.

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

Uniform Grants Guidance. Colorado Charter School Institute Cassie Walgren, Controller

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

Cost Sharing. Policy Statement and Purpose

Cost Sharing Policy Type: Administrative Responsible Office: Office of Sponsored Programs (proposal and award), Office of Research and Innovation, and Grants and Contracts Accounting (fiscal and accounting),

Cost Sharing Policy Type: Administrative Responsible Office: Office of Sponsored Programs (proposal and award), Office of Research and Innovation, and Grants and Contracts Accounting (fiscal and accounting),

Sponsored Programs and Research Compliance SUBRECIPIENT COMMITMENT FORM

SUBRECIPIENT COMMITMENT FORM All subrecipients should complete this form when submitting a subaward proposal to University of North Carolina Wilmington (UNCW). Please complete this form and send all required

SUBRECIPIENT COMMITMENT FORM All subrecipients should complete this form when submitting a subaward proposal to University of North Carolina Wilmington (UNCW). Please complete this form and send all required

Department of Contracts, Grants and Financial Administration, Texas Education Agency 1/26/18

Federal Grant Procurement Rules and Regulations and Federal Fiscal Monitoring Requirements Cory Green, Associate Commissioner Department of Contracts, Grants and Financial Administration Texas January

Federal Grant Procurement Rules and Regulations and Federal Fiscal Monitoring Requirements Cory Green, Associate Commissioner Department of Contracts, Grants and Financial Administration Texas January

Understanding the Adult Education State Director s Fiscal Responsibilities

Understanding the Adult Education State Director s Fiscal Responsibilities Office of Vocational and Adult Education Training for New State Staff November 5, 2013 Jay LeMaster OVERVIEW Sections of statute

Understanding the Adult Education State Director s Fiscal Responsibilities Office of Vocational and Adult Education Training for New State Staff November 5, 2013 Jay LeMaster OVERVIEW Sections of statute

How to Draft New & Update Old Policies and Procedures. Agenda. Why?

How to Draft New & Update Old Policies and Procedures Brette Kaplan Wurzburg bwurzbrug@bruman.com Jennifer Segal jsegal@bruman.com Fall Forum 2014 Agenda Why policies and procedures are important? Logistics

How to Draft New & Update Old Policies and Procedures Brette Kaplan Wurzburg bwurzbrug@bruman.com Jennifer Segal jsegal@bruman.com Fall Forum 2014 Agenda Why policies and procedures are important? Logistics

Subrecipient Risk Assessment and Monitoring of Northeastern University Issued Subawards

Subrecipient Risk Assessment and Monitoring of Northeastern University Issued Subawards What is a Subaward? A Subaward is a contractual agreement between Northeastern University and a third party organization

Subrecipient Risk Assessment and Monitoring of Northeastern University Issued Subawards What is a Subaward? A Subaward is a contractual agreement between Northeastern University and a third party organization

Financial Research Compliance. April 2013

Financial Research Compliance April 2013 Overview I. What is a Sponsored Award? II. Sponsored Awards at WFU III. Compliance IV. Hot Topics V. Audits VI. WFU Updates VII. Questions VIII. Contacts What is

Financial Research Compliance April 2013 Overview I. What is a Sponsored Award? II. Sponsored Awards at WFU III. Compliance IV. Hot Topics V. Audits VI. WFU Updates VII. Questions VIII. Contacts What is

University of San Francisco Office of Contracts and Grants Subaward Policy and Procedures

Summary 1. Subaward Definitions A. Subaward B. Subrecipient University of San Francisco Office of Contracts and Grants Subaward Policy and Procedures C. Office of Contracts and Grants (OCG) 2. Distinguishing

Summary 1. Subaward Definitions A. Subaward B. Subrecipient University of San Francisco Office of Contracts and Grants Subaward Policy and Procedures C. Office of Contracts and Grants (OCG) 2. Distinguishing

SJSU Research Foundation Cost Share Policy

SJSU Research Foundation Cost Share Policy Office of Sponsored Programs Policy No.: Effective Date: Supersedes: n/a Publication Date: OSP. 03-04-001 Rev. A 05/01/2017 6/29/2017 1.0 Purpose The Cost Share

SJSU Research Foundation Cost Share Policy Office of Sponsored Programs Policy No.: Effective Date: Supersedes: n/a Publication Date: OSP. 03-04-001 Rev. A 05/01/2017 6/29/2017 1.0 Purpose The Cost Share

Single Audit Entrance Conference Uniform Guidance Refresher

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

Cost Sharing Policy. Background, Scope and Purpose. Policy. Federal Guidance on Cost Sharing

Cost Sharing Policy Background, Scope and Purpose This policy and procedure was developed to: (1) provide guidance on the circumstances in which the University may approve cost sharing commitments and

Cost Sharing Policy Background, Scope and Purpose This policy and procedure was developed to: (1) provide guidance on the circumstances in which the University may approve cost sharing commitments and

SUBRECIPIENT COMMITMENT FORM

SUBRECIPIENT COMMITMENT FORM All subrecipients must complete this form when submitting a proposal to KSU, along with documents and certifications required by sponsors. This form must be endorsed by the

SUBRECIPIENT COMMITMENT FORM All subrecipients must complete this form when submitting a proposal to KSU, along with documents and certifications required by sponsors. This form must be endorsed by the

Financial Oversight of Sponsored Projects Principal Investigator and Department Administrator Responsibilities

Principal Investigator and Department Administrator Responsibilities Boston College Office for Sponsored Programs Office for Research Compliance and Intellectual Property March 2004 Introduction This guide

Principal Investigator and Department Administrator Responsibilities Boston College Office for Sponsored Programs Office for Research Compliance and Intellectual Property March 2004 Introduction This guide

Guidance on Direct Charging of Administrative and Clerical Salaries

Guidance on Direct Charging of Administrative and Clerical Salaries Updated: August 10, 2015 For proposals submitted and awards made on or after 12/26/14 that are subject to the Uniform Guidance. Key Notes

Guidance on Direct Charging of Administrative and Clerical Salaries Updated: August 10, 2015 For proposals submitted and awards made on or after 12/26/14 that are subject to the Uniform Guidance. Key Notes

An Exercise in Effort

3 rd Annual Symposium for Research Administrators An Exercise in Effort Brian Bertlshofer, Director, Cost Analysis and Compliance bertlsbj@email.unc.edu Aja Saylor, Central Effort Coordinator ajasaylor@unc.edu

3 rd Annual Symposium for Research Administrators An Exercise in Effort Brian Bertlshofer, Director, Cost Analysis and Compliance bertlsbj@email.unc.edu Aja Saylor, Central Effort Coordinator ajasaylor@unc.edu

UC San Diego Policy & Procedure Manual

UC San Diego Policy & Procedure Manual Search A Z Index Numerical Index Classification Guide What s New CONTRACTS AND GRANTS (RESEARCH) Section: 150-45 Effective: 08/01/2001 Supersedes: 05/26/1999 Review

UC San Diego Policy & Procedure Manual Search A Z Index Numerical Index Classification Guide What s New CONTRACTS AND GRANTS (RESEARCH) Section: 150-45 Effective: 08/01/2001 Supersedes: 05/26/1999 Review

Fiscal Compliance Requirements for Sponsored Programs Cost Sharing. Published 2010

Fiscal Compliance Requirements for Sponsored Programs Cost Sharing Published 2010 Learning Objectives Fiscal compliance requirements related to cost sharing Responsibility of Research Administrator and

Fiscal Compliance Requirements for Sponsored Programs Cost Sharing Published 2010 Learning Objectives Fiscal compliance requirements related to cost sharing Responsibility of Research Administrator and

Base. Base Determination and Cost Sharing. Bases represent the direct cost activities of an institution. Generally they consist of: 2/10/2014

Determination and Cost Sharing s represent the direct cost activities of an institution. Generally they consist of:» Instruction & departmental research» Organized research» Other sponsored activity (public

Determination and Cost Sharing s represent the direct cost activities of an institution. Generally they consist of:» Instruction & departmental research» Organized research» Other sponsored activity (public

Kathy Hancock, Assistant Grants Compliance Officer, DGCO, OPERA, Office of Extramural Research, NIH, HHS

Division of Grants Compliance and Oversight (DGCO) Office of Policy for Extramural Research Administration (OPERA), OER National Institutes of Health (NIH), DHHS 19 th Annual SBIR/STTR Conference Milwaukee,

Division of Grants Compliance and Oversight (DGCO) Office of Policy for Extramural Research Administration (OPERA), OER National Institutes of Health (NIH), DHHS 19 th Annual SBIR/STTR Conference Milwaukee,

WIOA SEC Administrative Provisions. Subparts: A - H. Presented by: 11/ 16/2016. Office of Grants Management

1 WIOA SEC. 683 Administrative Provisions Subparts: A - H Presented by: Office of Grants Management 11/ 16/2016 2 Today's Presenters Deborah Galloway Fiscal Policy Manager Division of Policy, Review &

1 WIOA SEC. 683 Administrative Provisions Subparts: A - H Presented by: Office of Grants Management 11/ 16/2016 2 Today's Presenters Deborah Galloway Fiscal Policy Manager Division of Policy, Review &

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees SHERYL L. STEPHENS BURKE, CPA, MST Nashua Office 102 Perimeter Road

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees SHERYL L. STEPHENS BURKE, CPA, MST Nashua Office 102 Perimeter Road

TIME AND EFFORT DOCUMENTATION 101 TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR EDGAR AND THE OMB CIRCULARS

TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR TIFFANY R. WINTERS, ESQ. TWINTERS@BRUMAN.COM @TRWINTERS BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NASTID 2014 1

TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR TIFFANY R. WINTERS, ESQ. TWINTERS@BRUMAN.COM @TRWINTERS BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NASTID 2014 1

SPONSORED PROGRAMS AWARDS, EXPENDITURES, AND ALLOWABILTY APRIL 2015 Policy

SPONSORED PROGRAMS AWARDS, EXPENDITURES, AND ALLOWABILTY APRIL 2015 Policy 2.2.01 Purpose: This policy was developed to ensure consistent compliance with 2 CFR part 200 Uniform Guidance and the Cost Accounting

SPONSORED PROGRAMS AWARDS, EXPENDITURES, AND ALLOWABILTY APRIL 2015 Policy 2.2.01 Purpose: This policy was developed to ensure consistent compliance with 2 CFR part 200 Uniform Guidance and the Cost Accounting

Uniform Guidance Subpart D Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Grant Administration Glossary of Commonly-Used Terms in Sponsored Programs

Page 1 of 6 Grant Administration Allowability: The determination of whether or not costs can be charged to a sponsored project as a direct or indirect cost. Allocability: A cost is allocable to a particular

Page 1 of 6 Grant Administration Allowability: The determination of whether or not costs can be charged to a sponsored project as a direct or indirect cost. Allocability: A cost is allocable to a particular

Policy and Compliance: Working Together Like Hand in Glove

Policy and Compliance: Working Together Like Hand in Glove Samuel Ashe, Director, Division of Grants Policy, OPERA, OER Diane W. Dean, Director, Division of Grants Compliance and Oversight, OPERA, OER

Policy and Compliance: Working Together Like Hand in Glove Samuel Ashe, Director, Division of Grants Policy, OPERA, OER Diane W. Dean, Director, Division of Grants Compliance and Oversight, OPERA, OER

Sponsored Projects Manual

Sponsored Projects Manual University Policies and Procedures for Requesting, Accepting, and Administering Grants, Contracts, and Cooperative Agreements February 2, 2005 CONTENTS 1. Overview... 4 1.1. Purpose

Sponsored Projects Manual University Policies and Procedures for Requesting, Accepting, and Administering Grants, Contracts, and Cooperative Agreements February 2, 2005 CONTENTS 1. Overview... 4 1.1. Purpose

Trinity Valley Community College. Grants Accounting Policy and Procedures 2012

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

Office of Sponsored Programs and Contracts

Office of Sponsored Programs and Contracts Proposal Process (Part A) Charles E. Patterson, Ph.D. Assistant Director Baylor University Office of Sponsored Programs 4 th Floor, Pat Neff Hall (254) 710-3817

Office of Sponsored Programs and Contracts Proposal Process (Part A) Charles E. Patterson, Ph.D. Assistant Director Baylor University Office of Sponsored Programs 4 th Floor, Pat Neff Hall (254) 710-3817

New Uniform Consolidated Grants Guidance

New Uniform Consolidated Grants Guidance From Accountability for Compliance to Accountability for Results The Honorable Jim Taylor and Robert Shea December 2014 Agenda Background Former circulars Consolidated

New Uniform Consolidated Grants Guidance From Accountability for Compliance to Accountability for Results The Honorable Jim Taylor and Robert Shea December 2014 Agenda Background Former circulars Consolidated

PIRATE. Principal Investigator Research Administration Training and Education: TESTS & ANSWERS. Office of the Vice President for Research

PIRATE Principal Investigator Research Administration Training and Education: TESTS & ANSWERS Office of the Vice President for Research Severna Park MD 21146 443 517 7074 WWW.FOSTERKNOWLEDGE.COM 1. Introduction

PIRATE Principal Investigator Research Administration Training and Education: TESTS & ANSWERS Office of the Vice President for Research Severna Park MD 21146 443 517 7074 WWW.FOSTERKNOWLEDGE.COM 1. Introduction

Federal Grants Administration Updates. Erin Auerbach Esq. Brustein & Manasevit, PLLC

Federal Grants Administration Updates Erin Auerbach Esq. eauerbach@bruman.com Brustein & Manasevit, PLLC 1 Agenda Perkins Reauthorization Workforce Investment Opportunity Act (WIOA) Navigating the New

Federal Grants Administration Updates Erin Auerbach Esq. eauerbach@bruman.com Brustein & Manasevit, PLLC 1 Agenda Perkins Reauthorization Workforce Investment Opportunity Act (WIOA) Navigating the New

University of North Carolina Finance Improvement & Transformation Contracts and Grants Standards. January 2015 Version 8

University of North Carolina Finance Improvement & Transformation Contracts and Grants Standards January 2015 Version 8 Table of Contents Introduction.......3 Account Setup.....10 Time and Effort Reporting......14

University of North Carolina Finance Improvement & Transformation Contracts and Grants Standards January 2015 Version 8 Table of Contents Introduction.......3 Account Setup.....10 Time and Effort Reporting......14

SUBRECIPIENT COMMITMENT FORM

SECTION A SUBRECIPIENT INFORMATION SUBRECIPIENT COMMITMENT FORM Phone: Email: SUBRECIPIENT: CU PI: PROPOSAL TITLE: TOTAL FUNDING REQUESTED: ORIGINATING SPONSOR, IF A PASS THRU APPLICATION: PRIME SPONSOR:

SECTION A SUBRECIPIENT INFORMATION SUBRECIPIENT COMMITMENT FORM Phone: Email: SUBRECIPIENT: CU PI: PROPOSAL TITLE: TOTAL FUNDING REQUESTED: ORIGINATING SPONSOR, IF A PASS THRU APPLICATION: PRIME SPONSOR:

Texas Association of County Auditors

Presentation to Texas Association of County Auditors New Uniform Grant Guidance and Update on 2014 OMB Circular A-133 Compliance Supplement by www.padgett-cpa.com Presenters Joel Perez, Jr., Partner Leader

Presentation to Texas Association of County Auditors New Uniform Grant Guidance and Update on 2014 OMB Circular A-133 Compliance Supplement by www.padgett-cpa.com Presenters Joel Perez, Jr., Partner Leader

Grant and Contract Accounting

University of Washington Faculty Grants Management Program Grant and Contract Accounting Sue Camber, Assistant Vice President Research Accounting and Analysis Grant and Contract Accounting University of

University of Washington Faculty Grants Management Program Grant and Contract Accounting Sue Camber, Assistant Vice President Research Accounting and Analysis Grant and Contract Accounting University of

Policies Superseded: ACAD 301 (portion) Revised: January 2016: March 2016

Revised: January 2016: March 2016") Policy Title: Indirect Cost Recovery and Allocation Policy Number: ACAD-RSCH 130 Created: September 2011 Policies Superseded: ACAD 301 (portion) Revised: January 2016: March 2016 Responsible Office: Office

Policy Title: Indirect Cost Recovery and Allocation Policy Number: ACAD-RSCH 130 Created: September 2011 Policies Superseded: ACAD 301 (portion) Revised: January 2016: March 2016 Responsible Office: Office

4.12 Effort Certification

4.112 Grants and Cooperative Agreements 4.1121 The Public Health Service ("PHS") and the National Science Foundation ("NSF") have regulations promoting objectivity in research by requiring that a university

4.112 Grants and Cooperative Agreements 4.1121 The Public Health Service ("PHS") and the National Science Foundation ("NSF") have regulations promoting objectivity in research by requiring that a university

Sponsored Programs Reference Manual

Sponsored Programs Reference Manual This document produced by the Research Administration Improvement Initiative in collaboration with the Office of Sponsored Programs 2006 Massachusetts Institute of Technology

Sponsored Programs Reference Manual This document produced by the Research Administration Improvement Initiative in collaboration with the Office of Sponsored Programs 2006 Massachusetts Institute of Technology

Sponsored Programs Roles & Responsibilities

The University of Florida is committed to acting with integrity in the management of sponsored programs. The goals of this document are to provide descriptions of key individuals or units and their responsibilities

The University of Florida is committed to acting with integrity in the management of sponsored programs. The goals of this document are to provide descriptions of key individuals or units and their responsibilities

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS Agenda Uniform Guidance Summary General Federal Procurement Laws Thresholds and Implications Sole Source Vendors Cooperative Purchasing

The Uniform Guidance and Procurement TEXAS ASSOCIATION OF COUNTY AUDITORS Agenda Uniform Guidance Summary General Federal Procurement Laws Thresholds and Implications Sole Source Vendors Cooperative Purchasing

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews Denise Dusek, MPA Federal Funding Specialist ESC 20 Image obtained from google.com Education Service Center, Region 20 May 2018 2 1 Participants

Fiscal Compliance: Desk Audit and Fiscal Monitoring Reviews Denise Dusek, MPA Federal Funding Specialist ESC 20 Image obtained from google.com Education Service Center, Region 20 May 2018 2 1 Participants

December 26, 2014 NEW ADDITIONAL December 26, 2014 beginning December 26, /31/15, 6/30/16 Contents Reference Origin Appendix

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

Fiscal Compliance Training Series: Charging Salaries Travel Expenses

Fiscal Compliance Training Series: Charging Salaries Travel Expenses Wed., April 26, 2017, 2:00 pm to 3:00 pm Curry Student Center, Room No. 318-320-322 Fiscal Management Lifecycle 2 Conduct Research and

Fiscal Compliance Training Series: Charging Salaries Travel Expenses Wed., April 26, 2017, 2:00 pm to 3:00 pm Curry Student Center, Room No. 318-320-322 Fiscal Management Lifecycle 2 Conduct Research and