UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY. Office of Contracts and Grants December, 2014

|

|

|

- Shannon Marshall

- 6 years ago

- Views:

Transcription

1 UNIFORM GUIDANCE - IMPLEMENTATION 2 CFR 200 SUMMARY Office of Contracts and Grants December, 2014

Combines/revises 8")

A-21 (Cost")

2 2 CFR OVERVIEW Published in Federal Register 12/26/2013 Joint effort between OMB and Council On Financial Assistance Reform (COFAR) Combines/revises 8 circulars in 1, including: A-110 (Administrative Requirements) A-21 (Cost Principles) A-133 (Audits)

3 2 CFR 200 WHY? Streamline guidance for Federal awards Reduce administrative burden Increase transparency & strengthen oversight of federal spending to reduce risk, fraud, waste, and abuse More focus on project performance and internal controls

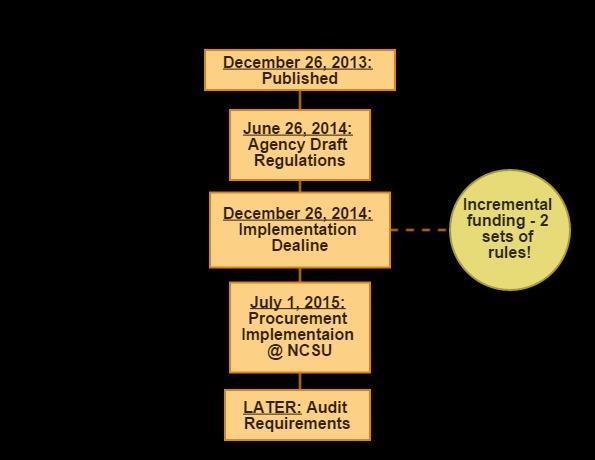

4 WHEN?

")

5 WHEN? (CONT.) CNG/SPARCS:

6 UNIFORM GUIDANCE SECTIONS Preamble: Pages , Supplemental information and discussion of issues Subpart A: Pages , Acronyms and Definitions, 200.X Subpart B: Pages , General Provisions, 200.1XX Subpart C: Pages , Pre Federal Award Requirements and Contents of Federal Awards, 200.2XX Subpart D: Pages , Post Federal Award Requirements Standards for Financial and Program Management, 200.3XX Subpart E: Pages , Cost Principles, 200.4XX Subpart F: Pages , Audit Requirements, 200.5XX

7 UNIFORM GUIDANCE SECTIONS Appendix I: Pages , Full Text of Notice of Funding Opportunity Appendix II: Pages , Contract Provisions for Non-Federal Entity Contracts Under Federal Awards Appendix III: Pages , Indirect (F&A) Costs Identification and Assignment, and Rate Determination for Institutions of Higher Education (IHEs) Appendix IV: Pages , Indirect (F&A) Costs Identification and Assignment, and Rate Determination for Nonprofit Organizations Appendix V: Pages , State/Local Government and Indian Tribe-Wide Central Service Cost Allocation Plans

8 UNIFORM GUIDANCE SECTIONS Appendix VI: Pages , Public Assistance Cost Allocation Plans Appendix VII: Pages , States and Local Government and Indian Tribe Indirect Cost Proposals Appendix VIII: Page 78691, Nonprofit Organizations Exempted From Subpart E-Cost Principles Appendix IX: Page 78691, Hospital Cost Principles Appendix X: Page 78691, Data Collection Form Appendix XI: Page 78691, Compliance Supplement

9 EFFECTIVE DATE ISSUES UG applies to Federal awards or funding increments after that date, in cases where the Federal agency considers funding increments to be an opportunity to modify the terms and conditions of the Federal award. It will not retroactively change the terms and conditions for funds a non- Federal entity has already received.

10 KEY ISSUES/CHANGES Issues Limited Implementation Guidance Agency Draft Regulations Technical Corrections Internal Controls Changes Admin & Clerical Salaries Computing Devices Participant Support Costs Publication Costs Subrecipient Indirect Rate Visa Charges Certification Statement Closeouts Cost Sharing Faculty Disengagement Procurement Subrecipient Monitoring & Management Residual Inventory

11 CERTIFICATION STATEMENT (A) Financial reports and invoices must be signed by an authorized official: By signing this report, I certify to the best of my knowledge and belief that the report is true, complete, and accurate, and the expenditures, disbursements and cash receipts are for the purposes and objectives set forth in the terms and conditions of the Federal award. I am aware that any false, fictitious, or fraudulent information, or the omission of any material fact, may subject me to criminal, civil or administrative penalties for fraud, false statements, false claims or otherwise.

12 UNLIKE CIRCUMSTANCES CLERICAL AND ADMINISTRATIVE SALARIES (C) Salaries of administrative and clerical staff NORMALLY indirect (F&A) cost. (no change) Direct charging may be appropriate if ALL of the following conditions are met: Services are integral to project or activity Individuals can be specifically identified with project Costs are explicitly included in budget or have prior written approval from agency Costs are not also recovered as F&A costs (in the development of the F&A Cost Proposal)

13 UNLIKE CIRCUMSTANCES CLERICAL AND ADMINISTRATIVE SALARIES Direct Charge Considerations Financial complexities are part of the award. Research Experiences for Undergraduates (REU) tracking travel, housing, stipends the department will not get participants if these pieces are not handled. Lablets that have numerous subtasks that have to be tracked as part of the award reporting. Administratively integral to the project. Documentation is not an administrative burden determined through a cost/benefit analysis.

14 UNLIKE CIRCUMSTANCES CLERICAL AND ADMINISTRATIVE SALARIES Documentation Requirements Clerical and Administrative Salaries that will be charged direct must be disclosed and justified in the proposal budget and budget narrative or through a prior approval request to the sponsor. Documentation supporting direct charge of these costs must be prepared before the expense is charged, not after the fact. Must be signed and dated. Documentation must indicate the essential nature or degree of support. Job titles should also be accurate and clearly convey the work being performed by that individual. Easy and quick retrieval of the support (unlike circumstance) is expected when requested.

15 UNLIKE CIRCUMSTANCES CLERICAL AND ADMINISTRATIVE SALARIES If Questioned by the Sponsor: Be prepared to explain individual s activity and why unlike/unusual Be prepared to explain why individual s activity on THIS grant is different than on another grant, if such individual s time is NOT directly charged on another grant.

16 UNLIKE CIRCUMSTANCES CLERICAL AND ADMINISTRATIVE SALARIES Unallowable as a Direct Charge A standard or departmental average % added to each award to cover one or more administrative positions. Activity that is essentially required in all sponsored awards, such as assembling and copying a technical report. Grant proposal writing and preparation work can never be charged to a grant. Same need in multiple projects

17 UNLIKE CIRCUMSTANCES CLERICAL AND ADMINISTRATIVE SALARIES Strategies to Manage Risk Mandatory Training Periodic Reviews of documentation. C&G removes charges. Use of Project Attribute for Unlike Circumstances Use of PMR System to process request

NOT considered a depreciable asset by NCSU may be charged as supplies Item(s) must be essential and allocable NOT required to be solely dedicated to single project Definition: Computing devices")

18 COMPUTING DEVICES (UNDER MATERIALS AND SUPPLIES) Computing devices (laptops, desktops, software, etc.) NOT considered a depreciable asset by NCSU may be charged as supplies Item(s) must be essential and allocable NOT required to be solely dedicated to single project Definition: Computing devices means machines used to acquire, store, analyze, process, and publish data and other information electronically, including accessories (or peripherals ) for printing, transmitting and receiving, or storing electronic information.

19 CONFERENCES Very similar to A-21 with these additions: As needed, the costs of identifying, but not providing, locally available dependent-care resources are allowable. (NCSU could only charge if we were allowed to charge this to all funding sources) Conference hosts/sponsors must exercise discretion and judgment in ensuring that conference costs are appropriate, necessary and managed in a manner that minimizes costs to the Federal award.

20 COST ACCOUNTING STANDARDS Required to submit revisions 6 months in advance of a change in disclosed practice. May proceed with implementing change only if Cognizant Federal Agency does not respond within 6 months or request more time to review.

21 ENTERTAINMENT COSTS Costs of entertainment, including amusement, diversion, and social activities and any associated costs are unallowable. UG Provides exception. If entertainment costs have a programmatic purpose and are authorized either in the approved budget for the Federal award or with prior written approval of the Federal awarding agency, the costs are allowable

22 FEDERAL AGENCY RECOGNITION OF FULL NEGOTIATED INDIRECT COST RATES (C)(1) The negotiated rates must be accepted by all Federal awarding agencies unless a different rate is required by Federal statue or regulation, or when approved by a Federal awarding agency head or delegate based on a justification. Federal agency head or delegate must notify OMB of any approved deviations from negotiated rates. Agency must include in the notice of funding opportunity the policies relating to indirect cost rate reimbursement, matching, or cost share as approved.

23 LOSSES ON AWARDS Any excess of costs over authorized funding levels transferred from any award or contract to another award or contract is unallowable as direct or indirect costs.

24 MTDC DEFINITION Participant Support Costs are specifically excluded from MTDC

25 PARTICIPANT SUPPORT COSTS Allowable with prior approval of the Federal Awarding Agency Definition: Participant support costs means direct costs for items such as stipends or subsistence allowances, travel allowances, and registration fees paid to or on behalf of participants or trainees (but not employees) in connection with conferences, or training projects.

26 PUBLICATION COSTS ( ) The costs of publication (page charges) or sharing of research results may be charged to the project after the period of performance as long as the costs are incurred prior to closeout.

27 SUBRECIPIENT INDIRECT COST RATE (F) Any non-federal entity (state, local government, Indian tribe, institution of higher education or nonprofit organization) that has never had a negotiated indirect cost rate may use a de minimis rate of 10% of modified total direct costs (MTDC) indefinitely. The only exception is a governmental department or agency unit that receives more than $35 million in direct Federal funding must submit an indirect cost proposal. This will allow very small entities to recover 10% of MTDC from the federal government to share in the cost of operations.

28 TRAVEL Commercial airfare, least expensive unrestricted accommodations is allowed (However, we are limited by University travel regulations Transportation by commercial airlines is limited to actual coach fare, substantiated by receipt.)

29 VISA CHARGES (UNDER RECRUITING COSTS) Short-term, travel visa costs (as opposed to longer-term, immigration visas) are generally allowable expenses that may be proposed as a direct cost. Since short-term visas are issued for a specific period and purpose, they can be clearly identified as directly connected to work performed on a Federal award. For these costs to be directly charged to a Federal award, they must: (1) Be critical and necessary for the conduct of the project; (2) Be allowable under the applicable cost principles; (3) Be consistent with the non-federal entity s cost accounting practices and non-federal entity policy; and (4) Meet the definition of direct cost as described in the applicable cost principles.

30 MYTHS Effort Reporting has been eliminated-false Non prescriptive after the fact certification still required

31 QUESTIONS? Ann Grigg / ann_grigg@ncsu.edu Caroline Pennington / cewilli3@ncsu.edu

Uniform Guidance Sponsored Projects Services

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Arizona s First University. Uniform Guidance Sponsored Projects Services 520-626-6000 sponsor@email.arizona.edu Agenda What is Uniform Guidance (UG)? Effective dates Structure of the Uniform Guidance Significant

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance)

") Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (New Uniform Guidance) Spring Research Administrators Series March 19, 2015 1 Agenda Background UW-Madison

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. AUSPAN Martha Taylor

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AUSPAN 2 16 2015 Martha Taylor Grants Reform February 2011 President directed OMB to reduce unnecessary regulatory

Federal Rules for Sponsored Programs. Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

Federal Rules for Sponsored Programs Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards 2 CFR 200 Uniform Guidance (UG) The Basics Presented by Dan Evon Director

UNIFORM GUIDANCE OVERVIEW. Budget Officers Meeting January 28, 2015

UNIFORM GUIDANCE OVERVIEW Budget Officers Meeting January 28, 2015 OMB Circulars Before and After Eight circulars condensed to one new comprehensive set of requirements for recipients of federal awards

UNIFORM GUIDANCE OVERVIEW Budget Officers Meeting January 28, 2015 OMB Circulars Before and After Eight circulars condensed to one new comprehensive set of requirements for recipients of federal awards

OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN

TO 2 CFR 200 (UNIFORM ADMIN") Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

Table of Contents OVERVIEW OF OMB SUPERCIRCULAR... 1 OBJECTIVES OF THE REFORM... 1 OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements for Federal Awards Chad Person May 1, 2013 Presented By: Devesh Kamal, CPA Shareholder deveshk@cshco.com Jesse Young, CPA Principal

Presenter. Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance

The New OMB Uniform Guidance") Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance Presenter Richard Cunningham Quality Assurance & Technical Specialist Center

Changes to Federal Programs & Single Audits (A-87, A-21, A-122, A-102, A-110, A-89, A-133 & A-50) The New OMB Uniform Guidance Presenter Richard Cunningham Quality Assurance & Technical Specialist Center

Overview of the New EDGAR (formerly the Uniform Grants Guidance)

") Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Overview of the New EDGAR (formerly the Uniform Grants Guidance) LEIGH MANASEVIT LMANASEVIT@BRUMAN.COM BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NATIONAL TITLE I CONFERENCE FEBRUARY 2015 AGENDA Importance

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. AU SPAN Martha Taylor Larry Hankins

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AU SPAN 6 23 2014 Martha Taylor Larry Hankins Grants Reform February 2011 President directed OMB to reduce

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AU SPAN 6 23 2014 Martha Taylor Larry Hankins Grants Reform February 2011 President directed OMB to reduce

Are You Ready for This? The New Uniform Guidance 2 CFR 200

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

Are You Ready for This? The New Uniform Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B $91B

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Are You Ready for This? The New Uniform Grant Guidance 2 CFR 200 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B $24B

Federal Grant Guidance Compliance

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

Federal Grant Guidance Compliance SPEAKER Melisa F. Galasso, CPA mgalasso@cbh.com Cherry Bekaert LLP Learning Objectives Describe the changes in the Uniform Grant Guidance List ways to implement changes

UNIFORM GUIDANCE IMPLEMENTATION

UNIFORM GUIDANCE IMPLEMENTATION Presented by Sara Judd, OSR Consultant October 2014 Uniform Guidance Implementation what we know and what we re guessing Ready, Set, Go 2014 Fred Hutchinson Cancer Research

UNIFORM GUIDANCE IMPLEMENTATION Presented by Sara Judd, OSR Consultant October 2014 Uniform Guidance Implementation what we know and what we re guessing Ready, Set, Go 2014 Fred Hutchinson Cancer Research

The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

This image cannot currently be displayed. The Uniform Guidance 2 CFR 200 A Guide to Risk-Based Grants Management 2015 This image cannot currently be displayed. Increase in Federal Grants Activity The Catalog

The OmniCircular - 2 CFR 200

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

The OmniCircular - 2 CFR 200 Mary Karen Wills 202-480-2773 mkwills@brg-expert.com Tina Reynolds 703.760.7701 Treynolds@mofo.com September 16, 2014 OMB Final Rule and Applicability Office of Management

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS - UPDATE FEBRUARY 2015 AOA Conference Pasadena, CA February 9, 2015 Agenda 1. Introduction / Disclaimer 2.

PART 3 COMPLIANCE REQUIREMENTS

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION Overview The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribes, institutions of higher

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION Overview The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribes, institutions of higher

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS. AOA Conference Sacramento, CA January 12, 2014

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS AOA Conference Sacramento, CA January 12, 2014 Agenda 1. Introduction 2. History 3. Learning Objectives 4.

UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS AOA Conference Sacramento, CA January 12, 2014 Agenda 1. Introduction 2. History 3. Learning Objectives 4.

OMB Uniform Guidance ( UG ) Briefing. ASRSP & OSR Brown Bag Tuesday, January 27 th

Briefing. ASRSP & OSR Brown Bag Tuesday, January 27 th") OMB Uniform Guidance ( UG ) Briefing ASRSP & OSR Brown Bag Tuesday, January 27 th Background The UG is the single biggest regulatory change in the last fifty years in research administration Interesting

OMB Uniform Guidance ( UG ) Briefing ASRSP & OSR Brown Bag Tuesday, January 27 th Background The UG is the single biggest regulatory change in the last fifty years in research administration Interesting

Jason Galloway, Associate Controller HSC Contract and Grant Accounting

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

Uniform Guidance How does this affect my Grant? Jason Galloway, Associate Controller HSC Contract and Grant Accounting New Guidance Replaces OMB Circulars: A-21, Principles for Determining Costs Applicable

NECA Update The New Uniform Guidance 2 CFR 200

NECA Update The New Uniform Guidance 2 CFR 200 September 23, 2014 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B

NECA Update The New Uniform Guidance 2 CFR 200 September 23, 2014 Increase in Federal Grants Activity The Catalog of Federal Domestic Assistance lists over 2,000 Federal grant programs $600B $200B $7B

Uniform Guidance Update. Ruth Boardman, Associate Director Office of Grants and Contracts March 2015

Uniform Guidance Update Ruth Boardman, Associate Director Office of Grants and Contracts March 2015 Objectives Latest Updates Internal Controls Procurement Status of Policies and Procedures Research Terms

Uniform Guidance Update Ruth Boardman, Associate Director Office of Grants and Contracts March 2015 Objectives Latest Updates Internal Controls Procurement Status of Policies and Procedures Research Terms

FAQ S FOR UNIFORM GUIDANCE

FAQ S FOR UNIFORM GUIDANCE As Uniform Guidance (UG) and its implications continue to be defined, the Fred Hutch UG Team will release a series of Frequently Asked Questions (FAQs) to clarify current standings.

FAQ S FOR UNIFORM GUIDANCE As Uniform Guidance (UG) and its implications continue to be defined, the Fred Hutch UG Team will release a series of Frequently Asked Questions (FAQs) to clarify current standings.

Post Award Manual. A. Chart of Accounts Overview

Post Award Manual Introduction: Award Management Section I. Section II. Sponsored Award Set up A. Chart of Accounts Overview Sponsored Expenditures Guidelines A. Introduction Purpose Who Should Use This

Post Award Manual Introduction: Award Management Section I. Section II. Sponsored Award Set up A. Chart of Accounts Overview Sponsored Expenditures Guidelines A. Introduction Purpose Who Should Use This

Uniform Grants Guidance. Colorado Charter School Institute Cassie Walgren, Controller

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

Uniform Guidance. Overview and Implementation Plan. November 21, 2014

Uniform Guidance Overview and Implementation Plan November 21, 2014 Uniform Guidance. Change is coming! College or Department name here 1 Overarching goal of the reform is to: streamline the rules and

Uniform Guidance Overview and Implementation Plan November 21, 2014 Uniform Guidance. Change is coming! College or Department name here 1 Overarching goal of the reform is to: streamline the rules and

OMB Uniform Guidance 2 CFR Part 200

OMB Uniform Guidance 2 CFR Part 200 What has changed - What hasn t What works What doesn t March 24, 2015 This session will focus on Brief outline of changes under the new OMB Uniform Guidance 2 CFR Part

OMB Uniform Guidance 2 CFR Part 200 What has changed - What hasn t What works What doesn t March 24, 2015 This session will focus on Brief outline of changes under the new OMB Uniform Guidance 2 CFR Part

Post Uniform Grant Guidance implementation from an auditor perspective

Post Uniform Grant Guidance implementation from an auditor perspective Jeff Zeichner Patrick Smith Agenda Uniform Grant Guidance review Challenges with UGG implementation SEFA Internal controls and compliance

Post Uniform Grant Guidance implementation from an auditor perspective Jeff Zeichner Patrick Smith Agenda Uniform Grant Guidance review Challenges with UGG implementation SEFA Internal controls and compliance

Roadmap to the Uniform Grant Guidance for School Districts

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

Roadmap to the Uniform Grant Guidance for School Districts Lily McManus, Editor lmcmanus@thompson.com Thompson Information Services, Inc. www.thompson.com Learning Objectives Explore issues of transparency

The Rollout of OMB A-81 and its Effect on UH

The Rollout of OMB A-81 and its Effect on UH Cris Milligan, Interim Assistant Vice President for Research Administration Beverly Rymer, Executive Director, Office of Contracts and GrantsOffice of Contracts

The Rollout of OMB A-81 and its Effect on UH Cris Milligan, Interim Assistant Vice President for Research Administration Beverly Rymer, Executive Director, Office of Contracts and GrantsOffice of Contracts

RESEARCH ADMINISTRATION FORUM Allowable Costs. Uniform Guide

RESEARCH ADMINISTRATION FORUM Allowable Costs Uniform Guide Objectives Understand what are allowable and unallowable costs to Federal grants Understand the importance of properly budgeting for costs on

RESEARCH ADMINISTRATION FORUM Allowable Costs Uniform Guide Objectives Understand what are allowable and unallowable costs to Federal grants Understand the importance of properly budgeting for costs on

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC 20410-0050 Special Attention of: NOTICE: SD-2015-01 Issued: FEB 2 6 2015 HUO Regional Directors HUD Field

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF THE DEPUTY SECRETARY WASHINGTON, DC 20410-0050 Special Attention of: NOTICE: SD-2015-01 Issued: FEB 2 6 2015 HUO Regional Directors HUD Field

SPONSORED PROGRAMS AWARDS, EXPENDITURES, AND ALLOWABILTY APRIL 2015 Policy

SPONSORED PROGRAMS AWARDS, EXPENDITURES, AND ALLOWABILTY APRIL 2015 Policy 2.2.01 Purpose: This policy was developed to ensure consistent compliance with 2 CFR part 200 Uniform Guidance and the Cost Accounting

SPONSORED PROGRAMS AWARDS, EXPENDITURES, AND ALLOWABILTY APRIL 2015 Policy 2.2.01 Purpose: This policy was developed to ensure consistent compliance with 2 CFR part 200 Uniform Guidance and the Cost Accounting

TIME AND EFFORT DOCUMENTATION 101 TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR EDGAR AND THE OMB CIRCULARS

TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR TIFFANY R. WINTERS, ESQ. TWINTERS@BRUMAN.COM @TRWINTERS BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NASTID 2014 1

TIME AND EFFORT DOCUMENTATION REQUIREMENTS AND CHANGES IN LIGHT OF THE OMB SUPERCIRCULAR TIFFANY R. WINTERS, ESQ. TWINTERS@BRUMAN.COM @TRWINTERS BRUSTEIN & MANASEVIT, PLLC WWW.BRUMAN.COM NASTID 2014 1

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO Lealan Miller, CPA, CGFM, Partner lmiller@eidebailly.com 208.383.4756 Organization of the Super-Circular, 2 CFR Part 200 Uniform Guidance

Uniform Guidance Year Two of the Audit Requirements Now What? CACUBO Lealan Miller, CPA, CGFM, Partner lmiller@eidebailly.com 208.383.4756 Organization of the Super-Circular, 2 CFR Part 200 Uniform Guidance

December 26, 2014 NEW ADDITIONAL December 26, 2014 beginning December 26, /31/15, 6/30/16 Contents Reference Origin Appendix

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

New Uniform Guidance September 11, 2014 Information from GAQC, NPO Conference, COFAR and a prior presentation by Diane Edelstein OMB Grant Reform December 26, 2013 OMB issued Final Grant Reform Rules -

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards Frances Hodge Public Health Analyst, Southern Services Branch Division of Metropolitan

45 CFR 75 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Health and Human Services Awards Frances Hodge Public Health Analyst, Southern Services Branch Division of Metropolitan

Policy on Cost Allocation, Cost Recovery, and Cost Sharing

President Page 1 of 11 PURPOSE: Provide guidance and structure when allocating and documenting costs (direct and indirect) for extramurally funded awards. Serves to provide direction for budgeting, allocating

President Page 1 of 11 PURPOSE: Provide guidance and structure when allocating and documenting costs (direct and indirect) for extramurally funded awards. Serves to provide direction for budgeting, allocating

What were the Changes from the OMB Circulars to the Uniform Guidance Bag Lunch Webinar June 21, 2016

What were the Changes from the OMB Circulars to the Uniform Guidance Bag Lunch Webinar June 21, 2016 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

What were the Changes from the OMB Circulars to the Uniform Guidance Bag Lunch Webinar June 21, 2016 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees SHERYL L. STEPHENS BURKE, CPA, MST Nashua Office 102 Perimeter Road

2 CFR Chapter II, Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards For Auditees SHERYL L. STEPHENS BURKE, CPA, MST Nashua Office 102 Perimeter Road

Diane Dean, Director Kathy Hancock, Assistant Grants Compliance Officer Joel Snyderman, Assistant Grants Compliance Officer

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar San Diego, CA October 2015 Diane Dean,

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar San Diego, CA October 2015 Diane Dean,

Base. Base Determination and Cost Sharing. Bases represent the direct cost activities of an institution. Generally they consist of: 2/10/2014

Determination and Cost Sharing s represent the direct cost activities of an institution. Generally they consist of:» Instruction & departmental research» Organized research» Other sponsored activity (public

Determination and Cost Sharing s represent the direct cost activities of an institution. Generally they consist of:» Instruction & departmental research» Organized research» Other sponsored activity (public

FDP Subaward Forms Frequently Asked Questions Check back frequently for updates!

FDP Subaward Forms Frequently Asked Questions Check back frequently for updates! Categories of Questions (click hyperlink below): Invoicing & Final Statement of Cumulative Costs Uniform Guidance (UG) data

FDP Subaward Forms Frequently Asked Questions Check back frequently for updates! Categories of Questions (click hyperlink below): Invoicing & Final Statement of Cumulative Costs Uniform Guidance (UG) data

Federal Grants and Financial Assistance 2017 Training Catalog

1 P a g e Who are we? Meet Colleague Consulting Colleague Consulting LLC is a 19-year-old small business specializing in training, human resource development, and organizational development services for

1 P a g e Who are we? Meet Colleague Consulting Colleague Consulting LLC is a 19-year-old small business specializing in training, human resource development, and organizational development services for

Single Audit Entrance Conference Uniform Guidance Refresher

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

Single Audit Entrance Conference Uniform Guidance Refresher MGO Audit Partner Annie Louie 31 Uniform Guidance Effective Date Federal Agencies Implement policies and procedures by promulgating regulations

Wake Forest University Financial Services: Grants Accounting and Compliance

Wake Forest University Financial Services: Grants Accounting and Compliance 1 WFU Policies and Procedures a Policies b Fiscal Administration i Award Notification 1 The Office of Research and Sponsored

Wake Forest University Financial Services: Grants Accounting and Compliance 1 WFU Policies and Procedures a Policies b Fiscal Administration i Award Notification 1 The Office of Research and Sponsored

Department of Defense Education Activity (DoDEA) DIVISION I: AWARD COVER PAGES

DIVISION I: AWARD COVER PAGES") DIVISION I: AWARD COVER PAGES Grant Number: (to be completed at the time of award) Type of award & Award Action: Grant New Award Total Grant Amount: (to be completed at the time of award) Obligation and

DIVISION I: AWARD COVER PAGES Grant Number: (to be completed at the time of award) Type of award & Award Action: Grant New Award Total Grant Amount: (to be completed at the time of award) Obligation and

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar Chicago, IL October 2016 Diane Dean, Director

Division of Grants Compliance and Oversight Office of Policy for Extramural Research Administration, OER National Institutes of Health, DHHS NIH Regional Seminar Chicago, IL October 2016 Diane Dean, Director

WELCOME. Pre-Award Phase Training

WELCOME Pre-Award Phase Training Morning Session Welcome GATA and New Federal Guidance Overview Cost Principles - Basic Considerations 10:00 10:15 BREAK Cost Principles Basic Consideration Cost Principles

WELCOME Pre-Award Phase Training Morning Session Welcome GATA and New Federal Guidance Overview Cost Principles - Basic Considerations 10:00 10:15 BREAK Cost Principles Basic Consideration Cost Principles

Subject: Financial Management Policy for Workforce Investment Act Funds

NORTH CAROLINA DEPARTMENT OF COMMERCE DIVISION OF WORKFORCE SOLUTIONS DWS POLICY STATEMENT NUMBER: PS 19-2013 Date: October 14, 2013 Subject: Financial Management Policy for Workforce Investment Act Funds

NORTH CAROLINA DEPARTMENT OF COMMERCE DIVISION OF WORKFORCE SOLUTIONS DWS POLICY STATEMENT NUMBER: PS 19-2013 Date: October 14, 2013 Subject: Financial Management Policy for Workforce Investment Act Funds

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT INTRODUCTION BACKGROUND On December 26, 2013, the Office of

UNDERSTANDING PHA OBLIGATIONS UNDER THE NEW UNIFORM RULE ON ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES AND AUDITS: WHAT S NEW AND WHAT S NOT INTRODUCTION BACKGROUND On December 26, 2013, the Office of

NSF Proposal and Award Policies & Procedures Guide (PAPPG) Update. Office of Grants and Contracts Administration December 23, 2014

Update. Office of Grants and Contracts Administration December 23, 2014") NSF Proposal and Award Policies & Procedures Guide (PAPPG) Update Office of Grants and Contracts Administration December 23, 2014 New PAPPG (NSF 15-1) Takes effect for proposals submitted or due on or

NSF Proposal and Award Policies & Procedures Guide (PAPPG) Update Office of Grants and Contracts Administration December 23, 2014 New PAPPG (NSF 15-1) Takes effect for proposals submitted or due on or

Office of Sponsored Programs Budgetary and Cost Accounting Procedures

Office of Sponsored Programs Budgetary and Cost Accounting Procedures Table of Contents 1. Purpose and Services 2. Definitions of Terms 3. Budget Items 4. Travel 5. Effort Certification Reporting 6. Costing

Office of Sponsored Programs Budgetary and Cost Accounting Procedures Table of Contents 1. Purpose and Services 2. Definitions of Terms 3. Budget Items 4. Travel 5. Effort Certification Reporting 6. Costing

Uniform Guidance Subpart D Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

Uniform Guidance Subpart D Administrative Requirements Purpose and Introduction Understanding the Uniform Guidance is essential to increase accountability of managing grant funds. The Administrative Requirements

COST PRINCIPLES AND PROCEDURAL STATEMENTS FAQs

COST PRINCIPLES AND PROCEDURAL STATEMENTS FAQs Cost Principles Policy FAQs Question: What is required for a cost to be adequately documented? Answer: Receipts or copies of receipts for all purchases (electronic

COST PRINCIPLES AND PROCEDURAL STATEMENTS FAQs Cost Principles Policy FAQs Question: What is required for a cost to be adequately documented? Answer: Receipts or copies of receipts for all purchases (electronic

Policies Superseded: ACAD 301 (portion) Revised: January 2016: March 2016

Revised: January 2016: March 2016") Policy Title: Indirect Cost Recovery and Allocation Policy Number: ACAD-RSCH 130 Created: September 2011 Policies Superseded: ACAD 301 (portion) Revised: January 2016: March 2016 Responsible Office: Office

Policy Title: Indirect Cost Recovery and Allocation Policy Number: ACAD-RSCH 130 Created: September 2011 Policies Superseded: ACAD 301 (portion) Revised: January 2016: March 2016 Responsible Office: Office

TEA Implementation of the New EDGAR

Implementation of the New EDGAR Office for Grants and Federal Fiscal Compliance Texas Education Agency ESC Cluster Site Implementation Training 2015 by the Texas Education Agency Agenda Introduction Written

Implementation of the New EDGAR Office for Grants and Federal Fiscal Compliance Texas Education Agency ESC Cluster Site Implementation Training 2015 by the Texas Education Agency Agenda Introduction Written

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida

Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida") Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

Implementing the OMB s Super Circular (aka UGG) Presented by: Anne Fritz, Finance Director, City of St. Petersburg, Florida Acknowledgement to Heather Acker, Partner, Baker Tilly, Virchow Krause, LLP for

University of Colorado Denver

University of Colorado Denver Campus Guidelines Title:, 4-13 Source: Prepared by: Approved by: Office of Grants and Contracts Director, Office of Grants and Contracts Vice Chancellor for Research Effective

University of Colorado Denver Campus Guidelines Title:, 4-13 Source: Prepared by: Approved by: Office of Grants and Contracts Director, Office of Grants and Contracts Vice Chancellor for Research Effective

INDIRECT COST POLICY

UNIVERSITY OF LOUISIANA AT LAFAYETTE OFFICE OF THE VICE PRESIDENT FOR RESEARCH INDIRECT COST POLICY Revision Date: 8/11/2014 Original Effective Date: 11/08/2006 Responsible Office: Reference: Vice President

UNIVERSITY OF LOUISIANA AT LAFAYETTE OFFICE OF THE VICE PRESIDENT FOR RESEARCH INDIRECT COST POLICY Revision Date: 8/11/2014 Original Effective Date: 11/08/2006 Responsible Office: Reference: Vice President

Vanderbilt University. Direct Cost. Guidelines for Budgeting and Charging Direct Costs on Sponsored Projects

Vanderbilt University Direct Cost Guidelines for Budgeting and Charging Direct Costs on Sponsored Projects 1 Table of Contents Flowchart Illustration Introduction Roles and Responsibilities Direct Costs:

Vanderbilt University Direct Cost Guidelines for Budgeting and Charging Direct Costs on Sponsored Projects 1 Table of Contents Flowchart Illustration Introduction Roles and Responsibilities Direct Costs:

OUTGOING SUBAWARD GUIDE: INFORMATION FOR UWM PRINCIPAL INVESTIGATORS VERSION 1, JULY 2015

OUTGOING SUBAWARD GUIDE: INFORMATION FOR UWM PRINCIPAL INVESTIGATORS VERSION 1, JULY 2015 INTRODUCTION The University of Wisconsin-Milwaukee (UWM) is the prime recipient on a wide range of sponsored awards

OUTGOING SUBAWARD GUIDE: INFORMATION FOR UWM PRINCIPAL INVESTIGATORS VERSION 1, JULY 2015 INTRODUCTION The University of Wisconsin-Milwaukee (UWM) is the prime recipient on a wide range of sponsored awards

Objectives for Financial Control over Grant Programs

Objectives for Financial Control over Grant Programs I. Cash management of grant funds is monitored for appropriate timing of receipts and disbursements of grant funds. (Cash Management) II. Procedures

Objectives for Financial Control over Grant Programs I. Cash management of grant funds is monitored for appropriate timing of receipts and disbursements of grant funds. (Cash Management) II. Procedures

UNIFORM GUIDANCE UPDATE

UNIFORM GUIDANCE UPDATE CINDY KIEL Executive Associate Vice Chancellor Office of Research Michael Allred Associate Vice Chancellor for Finance/Controller What is the Uniform Guidance? Uniform Administrative

UNIFORM GUIDANCE UPDATE CINDY KIEL Executive Associate Vice Chancellor Office of Research Michael Allred Associate Vice Chancellor for Finance/Controller What is the Uniform Guidance? Uniform Administrative

Policy(ies) Superseded: ACAD 301 (portion) Revised: January 2016, March 2016, March 2017

Superseded: ACAD 301 (portion) Revised: January 2016, March 2016, March 2017") Policy Title: Indirect Cost Recovery and Allocation Policy Number: ACAD-RSCH 134 Created: September 2011 Policy(ies) Superseded: ACAD 301 (portion) Revised: January 2016, March 2016, March 2017 Responsible

Policy Title: Indirect Cost Recovery and Allocation Policy Number: ACAD-RSCH 134 Created: September 2011 Policy(ies) Superseded: ACAD 301 (portion) Revised: January 2016, March 2016, March 2017 Responsible

Federal Grants Administration Updates. Erin Auerbach Esq. Brustein & Manasevit, PLLC

Federal Grants Administration Updates Erin Auerbach Esq. eauerbach@bruman.com Brustein & Manasevit, PLLC 1 Agenda Perkins Reauthorization Workforce Investment Opportunity Act (WIOA) Navigating the New

Federal Grants Administration Updates Erin Auerbach Esq. eauerbach@bruman.com Brustein & Manasevit, PLLC 1 Agenda Perkins Reauthorization Workforce Investment Opportunity Act (WIOA) Navigating the New

Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager. Tel:

Federal Agencies Implementation of the Super Circular & the JIR Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

Federal Agencies Implementation of the Super Circular & the JIR Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

Dollars & Sense: Federal Grant Financial

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

Dollars & Sense: Federal Grant Financial Management Rules Webinar Two April 12, 2016 Allison Ma luf, Esq. and Christopher Logue, Esq. Webinar Series APRIL 5, 2016 APRIL 7, 2016 APRIL 12, 2016 APRIL 14,

Something for Everyone: Adjusting to the OMB s Super Circular May 25, :30 10:10 am 2 CPE

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

Something for Everyone: Adjusting to the OMB s Super Circular May 25, 2016 8:30 10:10 am 2 CPE Heather Acker, Partner, Baker Tilly Virchow Krause, LLP Anne Fritz, Finance Director, City of St. Petersburg,

Texas Association of County Auditors

Presentation to Texas Association of County Auditors New Uniform Grant Guidance and Update on 2014 OMB Circular A-133 Compliance Supplement by www.padgett-cpa.com Presenters Joel Perez, Jr., Partner Leader

Presentation to Texas Association of County Auditors New Uniform Grant Guidance and Update on 2014 OMB Circular A-133 Compliance Supplement by www.padgett-cpa.com Presenters Joel Perez, Jr., Partner Leader

MONTGOMERY COUNTY INTERMEDIATE UNIT #23

No. 626 MONTGOMERY COUNTY INTERMEDIATE UNIT #23 SECTION: TITLE: FINANCES FEDERAL FISCAL COMPLIANCE ADOPTED: June 22, 2016 REVISED: 626. FEDERAL FISCAL COMPLIANCE 1. Authority Part 200 2. Delegation of

No. 626 MONTGOMERY COUNTY INTERMEDIATE UNIT #23 SECTION: TITLE: FINANCES FEDERAL FISCAL COMPLIANCE ADOPTED: June 22, 2016 REVISED: 626. FEDERAL FISCAL COMPLIANCE 1. Authority Part 200 2. Delegation of

MASSACHUSETTS INSTITUTE OF TECHNOLOGY. Policy for Cost Sharing and Matching Funds on Sponsored Projects Effective July 1, 1998

INTRODUCTION This policy rescinds and supersedes the MIT Guidelines for Cost Sharing and Matching Funds on Sponsored Projects dated June 25, 1997. PURPOSE AND SCOPE The Institute must ensure that cost

INTRODUCTION This policy rescinds and supersedes the MIT Guidelines for Cost Sharing and Matching Funds on Sponsored Projects dated June 25, 1997. PURPOSE AND SCOPE The Institute must ensure that cost

Marcia Smith Associate Vice Chancellor for Research

12-11-2014 Marcia Smith Associate Vice Chancellor for Research Agenda Research Administrator Forum December 11, 2014 Welcome and Announcements - Marcia Smith UCLA Implementation of: Uniform Administrative

12-11-2014 Marcia Smith Associate Vice Chancellor for Research Agenda Research Administrator Forum December 11, 2014 Welcome and Announcements - Marcia Smith UCLA Implementation of: Uniform Administrative

Grant and Contract Accounting

University of Washington Faculty Grants Management Program Grant and Contract Accounting Sue Camber, Assistant Vice President Research Accounting and Analysis Grant and Contract Accounting University of

University of Washington Faculty Grants Management Program Grant and Contract Accounting Sue Camber, Assistant Vice President Research Accounting and Analysis Grant and Contract Accounting University of

The Association of Universities for Research in Astronomy. Award Management Policies Manual

The Association of Universities for Research in Astronomy Award Management Policies Manual May 1, 2014 The Association of Universities for Research in Astronomy Award Management Policies Manual Table of

The Association of Universities for Research in Astronomy Award Management Policies Manual May 1, 2014 The Association of Universities for Research in Astronomy Award Management Policies Manual Table of

Accounting and Administrative Manual Section 100: Accounting and Finance

No.: D-01 Page: 1 of 5 Background: Cost sharing or matching represents the portion of the allowable project costs not borne by a sponsoring agency and is sometimes a required condition of receiving an

No.: D-01 Page: 1 of 5 Background: Cost sharing or matching represents the portion of the allowable project costs not borne by a sponsoring agency and is sometimes a required condition of receiving an

NASA Hubble Fellowship Program (NHFP) Policy and Budget Information 2018

Policy and Budget Information 2018") NASA Hubble Fellowship Program (NHFP) Policy and Budget Information 2018 1 P age Table of Contents INTRODUCTION... 3 NASA HUBBLE FELLOWSHIP PROGRAM CONTACTS... 3 SECTION 1: STGMS... 4 SECTION 2: ROLE DESCRIPTIONS...

NASA Hubble Fellowship Program (NHFP) Policy and Budget Information 2018 1 P age Table of Contents INTRODUCTION... 3 NASA HUBBLE FELLOWSHIP PROGRAM CONTACTS... 3 SECTION 1: STGMS... 4 SECTION 2: ROLE DESCRIPTIONS...

Federal Grants Compliance 101

Federal Grants Compliance 101 June 4, 2014 YOUR MISSION OUR SOLUTIONS Huron Consulting Group Inc. All Rights Reserved. Huron is a management consulting firm and not a CPA firm, and does not provide attest

Federal Grants Compliance 101 June 4, 2014 YOUR MISSION OUR SOLUTIONS Huron Consulting Group Inc. All Rights Reserved. Huron is a management consulting firm and not a CPA firm, and does not provide attest

Table of Contents. Introduction 2 How to Use This Guide 2 Best Practices for Budget Preparation 2

Prepared by Kathy Thatcher, Liberal Arts Grants Services Revised: May 15, 2015 Table of Contents Introduction 2 How to Use This Guide 2 Best Practices for Budget Preparation 2 Direct Costs 3 Salaries 4

Prepared by Kathy Thatcher, Liberal Arts Grants Services Revised: May 15, 2015 Table of Contents Introduction 2 How to Use This Guide 2 Best Practices for Budget Preparation 2 Direct Costs 3 Salaries 4

OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards

OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Research Advisory Board What PIs Need to Know January 2015 1 Background o When and Why? o Overview Important

OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Research Advisory Board What PIs Need to Know January 2015 1 Background o When and Why? o Overview Important

OMB New Uniform Guidance

ICCCFO Spring 2015 Conference April 8 10, 2015 Oglesby, IL Starved Rock Lodge and Convention Center OMB New Uniform Guidance Wednesday, April 8, 2015 4:15 pm 4:45 pm Presented by: Katherine Eilers, CPA,

ICCCFO Spring 2015 Conference April 8 10, 2015 Oglesby, IL Starved Rock Lodge and Convention Center OMB New Uniform Guidance Wednesday, April 8, 2015 4:15 pm 4:45 pm Presented by: Katherine Eilers, CPA,

Discretionary Grants Overview. Why This Session Is Needed. Lesson Overview & Module Objectives. Modifications: when, why, and how

Oversight and Monitoring 1 Why This Session Is Needed Prior approval requirements Ability to incur costs Modifications: when, why, and how Application to subrecipients Formula authority 2 Lesson Overview

Oversight and Monitoring 1 Why This Session Is Needed Prior approval requirements Ability to incur costs Modifications: when, why, and how Application to subrecipients Formula authority 2 Lesson Overview

Subcontract Monitoring

Subcontract Monitoring Subcontract definition Uniform Guidance (UG) 200.330-332 Subrecipient means a non-federal entity that expends Federal awards received from a passthrough entity to carry out a Federal

Subcontract Monitoring Subcontract definition Uniform Guidance (UG) 200.330-332 Subrecipient means a non-federal entity that expends Federal awards received from a passthrough entity to carry out a Federal

Trinity Valley Community College. Grants Accounting Policy and Procedures 2012

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

GATA GRANT ACCOUNTABILITY AND TRANSPARENCY ACT OVERVIEW T.H.E. CONFERENCE

GATA GRANT ACCOUNTABILITY AND TRANSPARENCY ACT OVERVIEW T.H.E. CONFERENCE 2.28.17 Topics of Discussion GATA Myths Applicability of GATA GATA Overview What s New Roles and Responsibilities Consequences

GATA GRANT ACCOUNTABILITY AND TRANSPARENCY ACT OVERVIEW T.H.E. CONFERENCE 2.28.17 Topics of Discussion GATA Myths Applicability of GATA GATA Overview What s New Roles and Responsibilities Consequences

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Preparing campus for what is changing and what is not What is Grants Reform and when is it effective? What

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards Preparing campus for what is changing and what is not What is Grants Reform and when is it effective? What

Financial Oversight of Sponsored Projects

Financial Oversight of Sponsored Projects Today s Agenda Introduction Reasons for Principal Investigator Oversight Sponsor and University Policies General Considerations Unallowable Costs Re-Budgeting

Financial Oversight of Sponsored Projects Today s Agenda Introduction Reasons for Principal Investigator Oversight Sponsor and University Policies General Considerations Unallowable Costs Re-Budgeting

WHEREAS, the Transit Operator provides mass transportation services within the Madison Urbanized Area; and

COOPERATIVE AGREEMENT FOR CONTINUING TRANSPORTATION PLANNING FOR THE MADISON, WISCONSIN METROPOLITAN AREA between STATE OF WISCONSIN, DEPARTMENT OF TRANSPORTATION and the MADISON AREA TRANSPORTATION PLANNING

COOPERATIVE AGREEMENT FOR CONTINUING TRANSPORTATION PLANNING FOR THE MADISON, WISCONSIN METROPOLITAN AREA between STATE OF WISCONSIN, DEPARTMENT OF TRANSPORTATION and the MADISON AREA TRANSPORTATION PLANNING

Guidelines for the Acceptance and Use of Externally Funded Grants and Contracts

Guidelines for the Acceptance and Use of Externally Funded Grants and Contracts http://www.una.edu/sponsored-programs/ Tanja F. Blackstone, PhD Director, Sponsored Programs tfblackstone@una.edu University

Guidelines for the Acceptance and Use of Externally Funded Grants and Contracts http://www.una.edu/sponsored-programs/ Tanja F. Blackstone, PhD Director, Sponsored Programs tfblackstone@una.edu University

Building a Budget. Rebecca Hunsaker Gaye Bugenhagen University of Maryland, College Park

Building a Budget Rebecca Hunsaker Gaye Bugenhagen University of Maryland, College Park 1 Disclaimer The information and federal regulations contained within this workshop are accurate and up to date as

Building a Budget Rebecca Hunsaker Gaye Bugenhagen University of Maryland, College Park 1 Disclaimer The information and federal regulations contained within this workshop are accurate and up to date as

Building Your Foundation: Administrative Requirements Boot Camp (Modules 1-8: Administrative Requirements for Non-Federal Entities)

") Course #400 Syllabus Grant Management Boot Camp (Covers 12 Grant Management Modules) This Boot Camp bundle includes 12 Grants Management training courses including 8 modules on the Administrative Requirements

Course #400 Syllabus Grant Management Boot Camp (Covers 12 Grant Management Modules) This Boot Camp bundle includes 12 Grants Management training courses including 8 modules on the Administrative Requirements

EASTERN MICHIGAN UNIVERSITY. Sponsored Research Accounting Cost Share Guidelines

EASTERN MICHIGAN UNIVERSITY Sponsored Research Accounting Cost Share Guidelines PURPOSE: The purpose for the Cost Share Guidelines is to articulate the roles and responsibilities of the various parties

EASTERN MICHIGAN UNIVERSITY Sponsored Research Accounting Cost Share Guidelines PURPOSE: The purpose for the Cost Share Guidelines is to articulate the roles and responsibilities of the various parties

Grants and Contracts Accounting Policies Manual

Grants and Contracts Accounting Policies Manual For assistance with researching funders, writing grants applications or proposals and/or with Northern Oklahoma College s grant process, or questions on

Grants and Contracts Accounting Policies Manual For assistance with researching funders, writing grants applications or proposals and/or with Northern Oklahoma College s grant process, or questions on

Subrecipient Profile Questionnaire

Subrecipient Profile Questionnaire How to use: The questionnaire is used to help determine a subrecipient organization s financial and management strength, which helps assess risk and dictates the monitoring

Subrecipient Profile Questionnaire How to use: The questionnaire is used to help determine a subrecipient organization s financial and management strength, which helps assess risk and dictates the monitoring

MAXIMUS Higher Education Practice

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director, MAXIMUS Jason Guilbeault, Senior Consultant, MAXIMUS 1 MAXIMUS Higher Education Practice Headquartered in Northbrook,

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director, MAXIMUS Jason Guilbeault, Senior Consultant, MAXIMUS 1 MAXIMUS Higher Education Practice Headquartered in Northbrook,

The Uniform Guidance (2 CFR, Part 200)

") WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

WCMC Implementation of The Uniform Guidance (2 CFR, Part 200) Tuesday, September 22, 2015 & Wednesday, September 23, 2015 UG Workshop Michelle A. Lewis, M.S. Director of Research Administration Interim

Federal Government Grants:

Federal Government Grants: Is My Organization Ready? Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor. 2017 CliftonLarsonAllen

Federal Government Grants: Is My Organization Ready? Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor. 2017 CliftonLarsonAllen

APPENDIX VII OTHER AUDIT ADVISORIES

APPENDIX VII OTHER AUDIT ADVISORIES I. Effect of Changes to Generally Applicable Compliance Requirements in the 2015 Supplement In the 2015 Supplement, OMB has removed several of the compliance requirements

APPENDIX VII OTHER AUDIT ADVISORIES I. Effect of Changes to Generally Applicable Compliance Requirements in the 2015 Supplement In the 2015 Supplement, OMB has removed several of the compliance requirements

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards Thursday, March 20, 2014, 12:30 p.m. 2:00 p.m. ET Venable LLP, Washington, DC Moderator: Jeffrey S. Tenenbaum,

The OMB Super Circular: What the New Rules Mean for Nonprofit Recipients of Federal Awards Thursday, March 20, 2014, 12:30 p.m. 2:00 p.m. ET Venable LLP, Washington, DC Moderator: Jeffrey S. Tenenbaum,