T3010 and Transparency in the Charitable Sector

|

|

|

- Juliana Morris

- 6 years ago

- Views:

Transcription

1 T3010 and Transparency in the Charitable Sector A presentation to AFP GTA Congress November 20, 2017 Mark Blumberg (mark@blumbergs.ca) Blumberg Segal LLP

2 Blumberg Segal LLP Blumberg Segal LLP is a law firm based in Toronto, Ontario Mark Blumberg is a partner at Blumbergs who focuses on non-profit and charity law Assists charities from across Canada with Canadian and international operations and foreign charities fundraising in Canada and Free Canadian Charity Law Newsletter. Sign up at: (416) or mark@blumbergs.ca 2

3 Introduction Legal information not legal advice Views expressed are my own Questions during and at end Logistics and timing 3

4 Charity Sector Environment Competition Insufficient resources (money, volunteers) vs. need Uncertain resources Maximize public benefit of charities Reporting requirements Desire for greater transparency and accountability Technology Standards Visibility National and International activities 4

5 Transparency

6 What is transparency? (UK) The Charity Commission interprets transparency and accountability as providing relevant and reliable information to stakeholders in a way that is free from bias, comparable, understandable and focused on stakeholders legitimate needs. 6

7 Why Charities Should Be Transparent? A high level of transparency when accounting for performance allows trustees to: demonstrate that resources are being used wisely and for the stated purpose; show that the charity is being organised and managed properly; demonstrate that the charity is carrying out its activities efficiently and effectively; and attract new resources to enable the charity to continue its activities. 7

8 Are Charities transparent? (UK) Our evidence is that the general standard of performance against the transparency and accountability framework is not satisfactory. Whilst there are some very good examples, too many charities in our study did not meet basic requirements. We hope that charities will take both this message and what the report shows about good practice to heart and respond constructively. 8

9 Does your charity describe impact? (UK) The impact of a charity s activities is of great interest to stakeholders as a measure of its effectiveness in applying its resources for public benefit. 16% of the Annual Reports explained in detail how the year s activities had benefited wider society. 34% gave limited information. 51% gave no details at all. 9

10 Transparency helps with running a better charity helps to prevent misuse of charity resources enhances stakeholder knowledge and confidence expectations are greater and T3010 has not kept up better data on the sector may improve discussion and decision-making 10

11 T3010

12 What is T3010 Canadian Registered Charities must file their T3010 Registered Charity Information Return every year Within six months of the end of the charity s fiscal period Form is mailed with labels to charity also can download form from: See for T3010 information (Blumberg Segal LLP) CRA Advanced Search 12

13 13

14 When to File T

15 Complete T3010 Part 1 Form T3010, Registered Charity Information Return; Form TF725, Registered Charity Basic Information Sheet; a copy of the charity s own financial statements, including notes to the financial statements; Form T1235, Directors/Trustees and Like Officials Worksheet, with all the required information; if applicable Form RC232 WS, Director/Officer Worksheet and Ontario Corporations Information Act Annual Return, or Form RC232, Ontario Corporations Information Act Annual Return; if applicable Form T1236, Qualified donees worksheet / Amounts provided to other organizations; 15

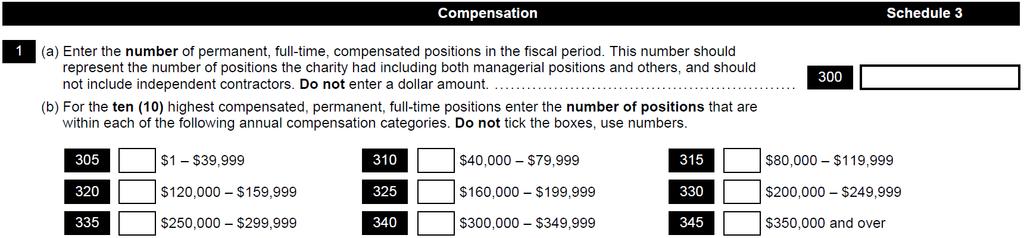

16 Complete T3010 Part 2 if applicable Schedule 1, Foundations; if applicable Schedule 2, Activities outside Canada; if applicable Schedule 3, Compensation; if applicable Schedule 4, Confidential data; if applicable Schedule 5, Gifts in kind; if applicable Schedule 6, Detailed financial information; if applicable Schedule 7, Political activities; and if applicable Form T2081, Excess Corporate Holdings Worksheet for Private Foundations. 16

17 Why File T3010 Legally required Only uniform way to compare Canadian charities Advertisement for charity Important for transparency of charity Only beginning of transparency (website, annual report, newsletters, e- mail lists, etc.) 17

18 Consequences for Failing to File Revocation of charitable status within months Cannot issue receipts Lose benefits of registered status Revocation tax if not re-registered within 1 year May not be able to reregister Embarrassing $500 penalty 18

19 Mistakes with T3010 T3010 must be the correct form, accurate and complete including schedules and financial statements otherwise may be returned or considered incomplete Lots of help on internet with T3010 Budget 2012 if T3010 not complete and accurate charity can be suspended from receipting 19

20 Problems with T3010 Using wrong form Not providing all information Not providing accurate information Not providing all schedules Not providing financial statements Not providing date of birth of directors 20

21 Why Transparency for the Public Accurately reflect your organizations work Bring in more resources (tactical and strategic) Understand the sector or subsector Compare your organization to others Identify risks Safeguard reputation of your charity 21

22 CRA Caution We recognize that completing the information return requires an understanding of some complex provisions. We recommend that, if necessary, registered charities get advice from legal or accounting experts. 22

23 What is Confidential Most of the T3010 is publicly available including financial statements Confidential data is marked Section F (physical, books and records address and who completed form)(not mailing address) Schedule 4 (information on funders and foreign donors) the right-hand side of Form T1235, Directors/Trustees and Like Officials Worksheet; (contact information on directors) and Part II, Section B, of Form T2081, Excess Corporate Holdings Worksheet for Private Foundations. (material transactions by relevant persons) CRA can share even confidential information in certain circumstances such as court order, enforcement of ITA, CPP, EI, CSIS, Finance etc. 23

24 Partial Section by Section

25 Programs 25

26 26

27 Ongoing and New Programs If the charity was not active, tick no. This means that during the entire fiscal period, the charity did not use any of its resources to carry out its charitable activities, or to further the charitable purposes for which it was established. To keep its registered status, the charity must file its information return and explain why it was not active in the Ongoing programs space at C2. C2 Describe any ongoing and new programs the charity carried on. New programs are those that the charity began in this fiscal period. 27

28 Ongoing and New Programs (Cont) The term program covers all the charitable activities the charity carries out on its own through employees or volunteers, and through intermediaries, as well as gifts it makes to qualified donees. Grant making registered charities should describe the types of organizations they support. The charity can use this space to give details about the contributions of its volunteers in carrying out its activities, including the number of volunteers and their hours. Since this section is public information, do not include the names of volunteers. Do not send documents such as annual reports in place of describing the charity s activities in question C2. Do not report information on fundraising activities here. 28

29 Ongoing and New Programs (Cont) If the charity is considering new activities that we have not yet approved, contact us before starting them to make sure that the proposed activities are charitable and fall within the charity s approved purposes. Use active verbs such as do, offer, operate, conduct, perform, educate, feed, give, or house to describe how the charity carried out its charitable activities during the fiscal period. You must give enough detail for a reader to understand what the charity does. Do not repeat the charity s purposes. For example, saying we advance religion, or we relieve poverty, is not enough. 29

30 30

31 Foreign Donors 31

32 32

33 Political Activities 33

34 Fundraising

35 35

36 36

37 Fundraising Costs and Practice Fundraising is important for charities but it is not a charitable activity Lots of media and donor concern about costs and practices CRA Guidance on Fundraising recently released Must read for anyone very involved with fundraising: 37

38 Organization of Guidance Fundraising by Registered Charities A. Introduction B. Summary C. Application and jurisdiction D. What is fundraising? E. Definitions F. When is fundraising not acceptable? G. Evaluating a charity's fundraising H. Factors that may influence the CRA s evaluation of a charity s fundraising Appendix A Examples of fundraising activities Appendix B Allocating fundraising expenditures Appendix C Best practices Appendix D Questions and answers Footnotes 38

39 Fundraising Ratio Ratio of costs to revenue over fiscal period under 35% This ratio is unlikely to generate questions or concerns by the CRA. Ratio of costs to revenue over fiscal period 35% and above The CRA will examine the average ratio over recent years to determine if there is a trend of high fundraising costs. The higher the ratio, the more likely it is the CRA will be concerned the charity is engaged in fundraising that is not acceptable, requiring a more detailed assessment of expenditures. Ratio of costs to revenue over fiscal period above 70% This level will raise concerns with the CRA. The charity must be able to provide an explanation and rationale for this level of expenditure to show that it is not engaged in unacceptable fundraising. 39

40 Questions on Ratio What are your total fundraising expenditures? What are your total fundraising revenues? What is the ratio of expenditures to revenue? Is the ratio high? What are you doing to reduce ratio? Is your board and senior staff aware of ratio? Are you disclosing to public accurately ratio? What other steps are you taking to be more transparent and provide more disclosure? Do you report regularly to your board about compliance with the Guidance? 40

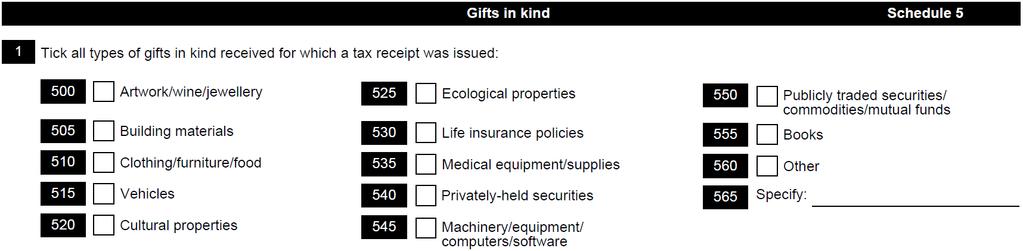

41 Exclusions from fundraising Fundraising does not include: seeking grants, gifts, contributions, or other funding from other charities or government, recruiting volunteers to carry out the general operations of the charity, or related business activities. (See CPS-019, What is a Related Business?) 41

42 Understating Fundraising Revenue Where a charity knowingly or negligently understates its fundraising expenses on line 5020 of Form T3010 or elsewhere, this is taken into account in assessing whether the charity has acted reasonably. Inaccurate reporting is grounds for compliance action under the Income Tax Act. 42

43 Employees and Compensation Compensation includes all forms of salaries, wages, commissions, bonuses, fees, and honoraria, plus the value of taxable and non-taxable benefits paid by a charity to its employees. Compensation generally includes all amounts that form part of an employee s gross income from employment, plus the charity s contributions to the employee s pension, medical or insurance plan, employer Canada Pension Plan/Quebec Pension Plan and employment insurance contributions, and workers compensation premiums. Do not include reimbursements for expenses incurred while working for the charity, such as travel claims. 43

44 44

45 45

46 46

47 Non-Cash Gifts Gifts-in-Kind (GIK) 47

48 Gifts-in-kind 1 Lines If the charity received gifts in kind for which it issued official donation receipts, tick all the types the charity received during the fiscal period. Does not cover gifts-in-kind that were not tax receipted 48

49 49

50 50

51 51

52 Schedule 6 Detailed Financial Information 52

53 53

54 Expenditures Line 5000 Enter the part reported on line 4950 that represents all expenditures on charitable activities, except for gifts to qualified donees. Examples include: running the charity s day-to-day programs; occupancy costs (such as rent, mortgage payments, hydro, repairs, and insurance) for buildings used to carry out charitable activities; most salaries; and education and training for staff and volunteers. Do not include expenditures for management, administration, fundraising, or political activities on this line. 54

55 Expenditures Line 5010 Enter the part reported on line 4950 that represents management and administrative expenditures. These may include expenses for: holding meetings of the board of directors; accounting, auditing, personnel, and other administrative services; buying supplies and equipment, and paying occupancy costs for administrative offices; and applying for grants or other types of government funding, and gifts from other qualified donees (usually foundations). 55

56 Expenditures Some expenditures can be considered partly charitable and partly management and administration, such as salaries and occupancy costs. In these cases, divide the amounts accordingly between lines 5000 and Expenditures must be allocated consistently and on a reasonable basis. 56

57 57

58 Certification 58

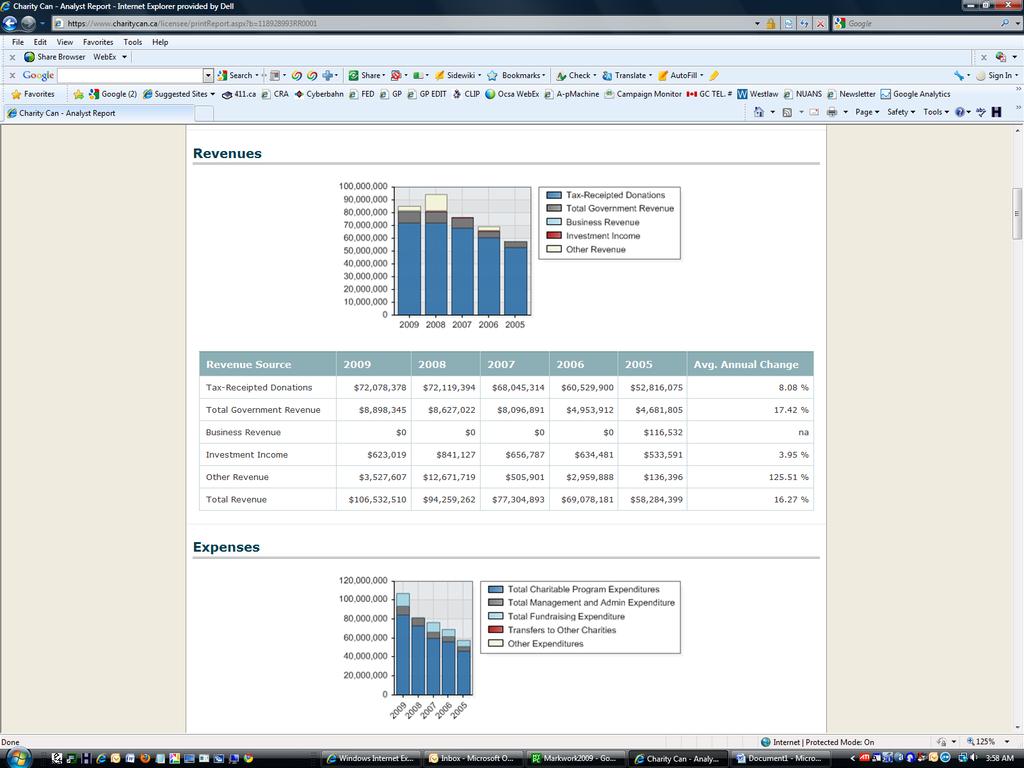

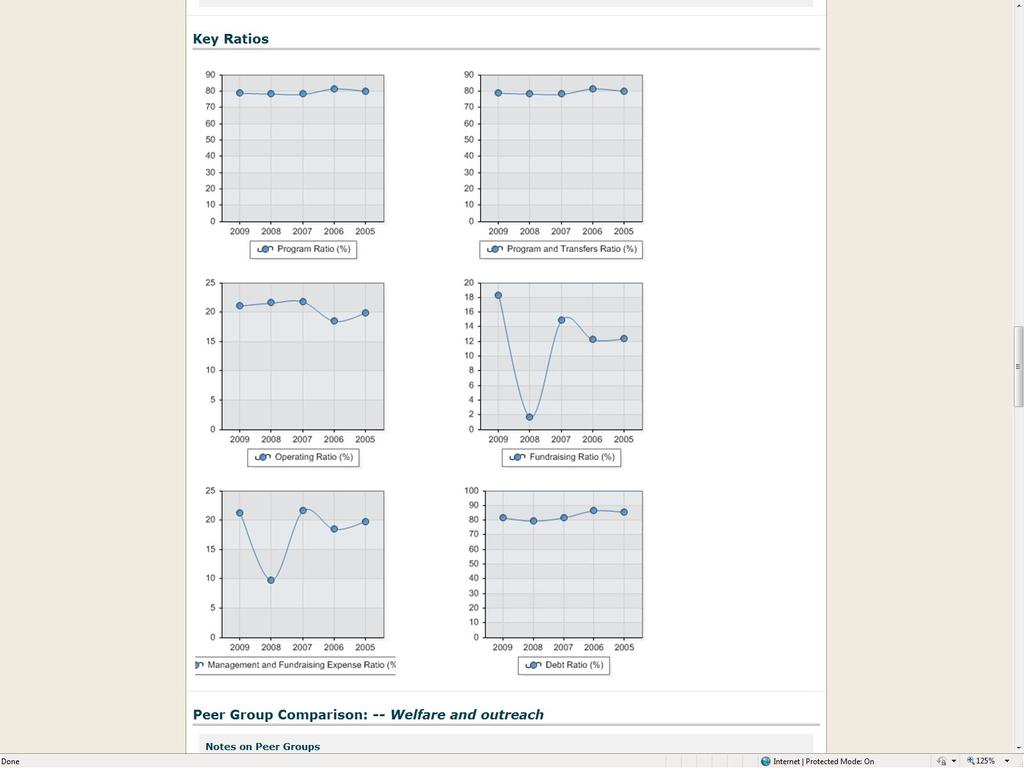

59 Media, Watchdog and Database Use of T3010 Information

60 ?? 60

61 Many Databases Utilizing T3010 Information (subscription) (subscription) 61

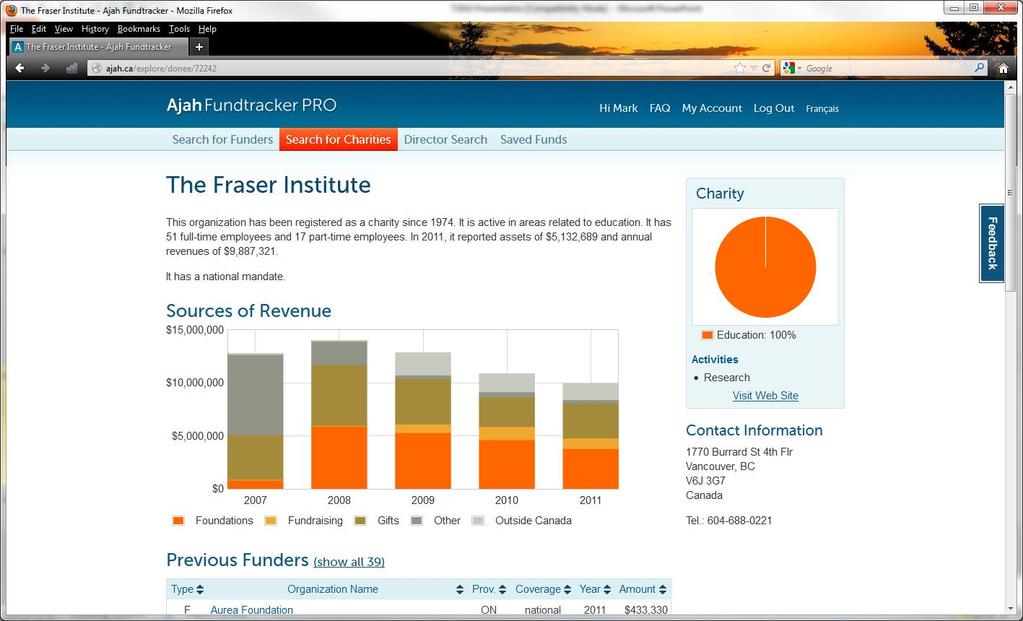

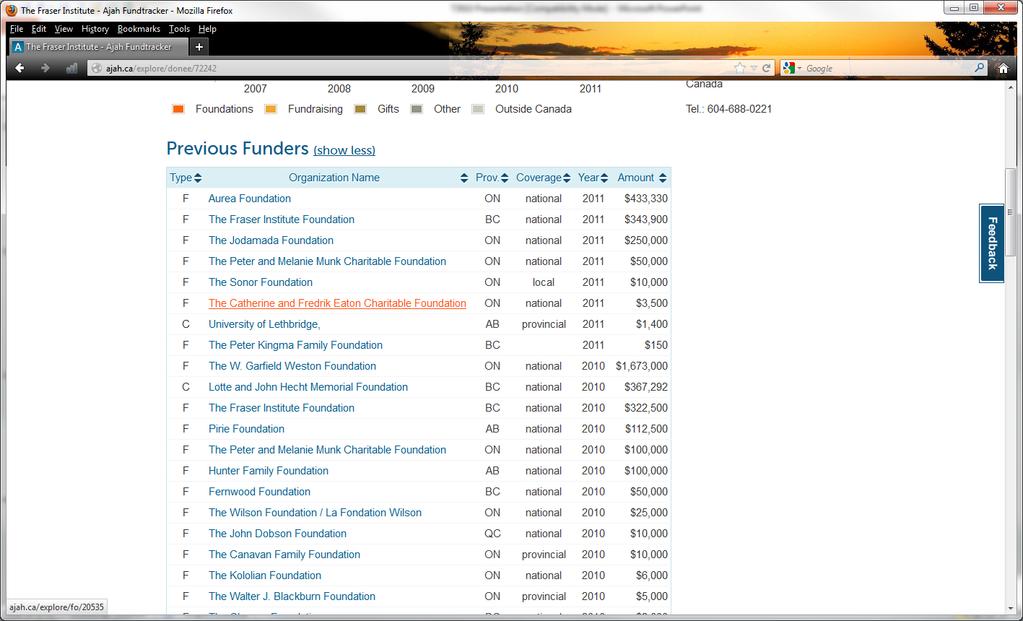

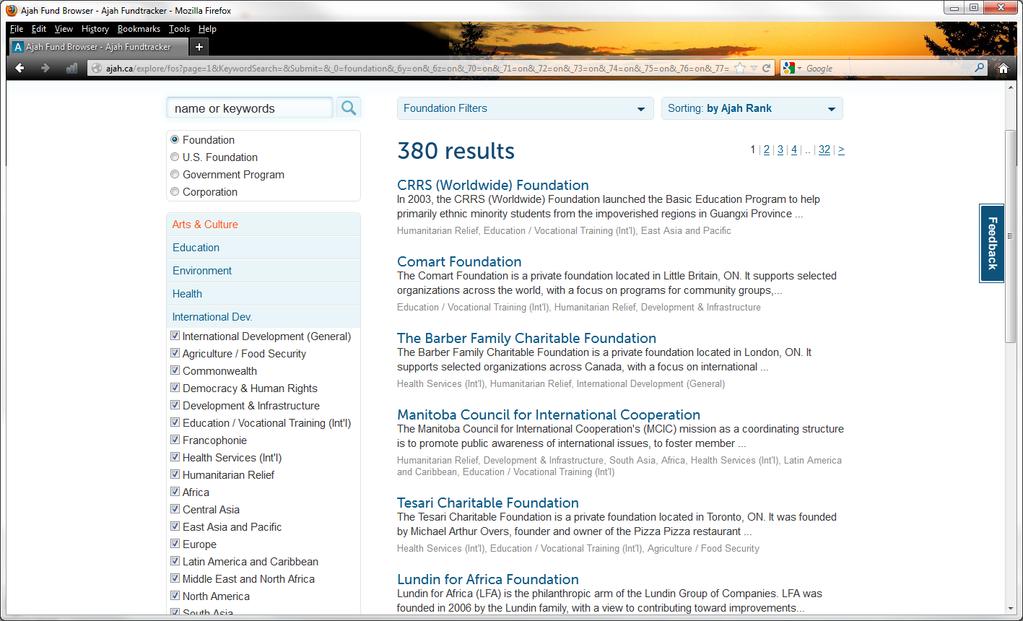

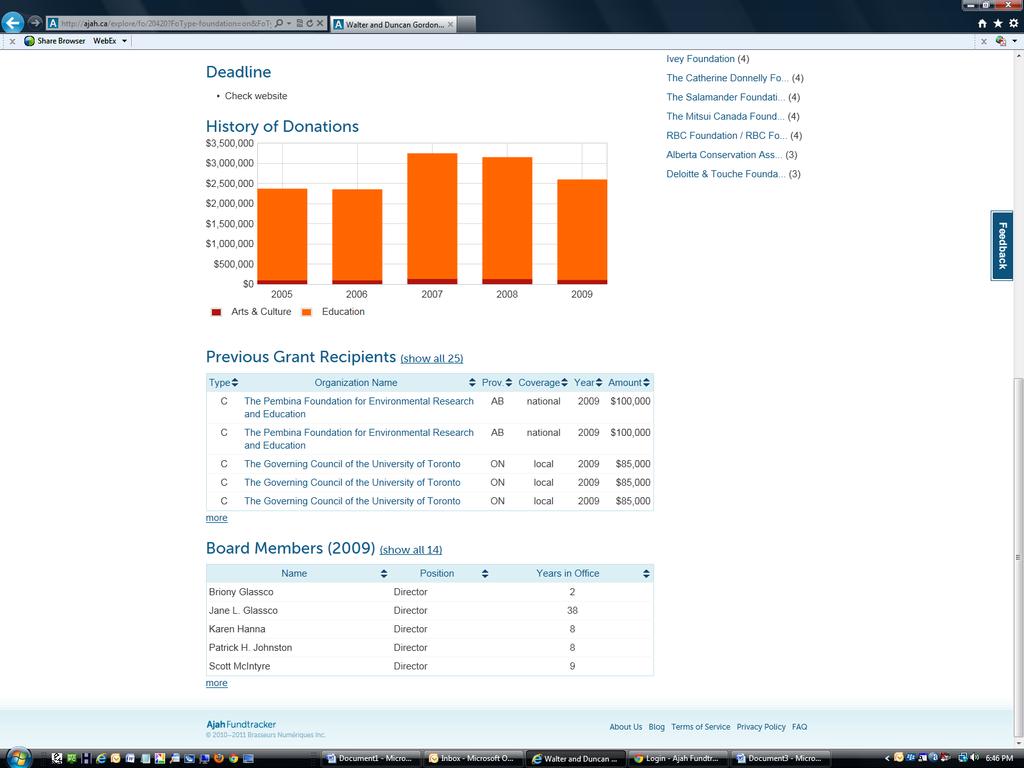

62 ?? 62

63 ? 63

64 ? 64

65 ? 65

66 CharityCan report on registered charity 66

67 67

68 68

69 AJAH report on registered charity 69

70 70

71 71

72

73

74

75

76

77 CAVEATS with T3010 Volunteers often completing Some don t understand Income Tax Act terminology Some don t know every facet of their charity Usually completed in a hurry Rarely is their enough input (finance, legal, accounting, program staff) Most are inputted manually Some charities are deliberately deceptive GAAP vs. tax form Many important questions are not asked (tree vs. forest) Some questions are ambiguous Based on fiscal year and can be huge swings between years 77

78 A Closer Look at the T3010 Using Different Lenses

79 Examples of uses of T3010 information Individual charity, vs subsector vs sector analysis and benchmarking Charity sector spends almost $225 billion per year perhaps your organization offers services or programs that could capture some of those funds. Only limited by your imagination Grants vs. loans. 79

80 Specific Examples Use postal code data to find foundations geographically located near your hospital. Which charities or foundations worked in which country if you want to support your work in a particular country You are interested in a particular person what boards of directors does the person serve on gives you idea about what they care about and who they are connected to. Which charities gave to which other charities that are similar to your charity? Which charities could we work with or collaborate with? Which charities are new? 80

81 Specific Examples (Cont) Which charities have grown in revenue? Which foundations have the biggest asset base? Which ones are not receiving a good return on their investments/may be interested in an PRI. Which charities are conducting political activities? Which charities received funds from abroad? Which charities received a lot of government revenue and from which level of government? Benchmarking how is your charity comparing to others in terms of fundraising, government revenue, expenditures, etc. Awareness of directors of charities that were revoked 81

82 Specific Examples (Cont) Find charities across country to implement programs or partner with Selling organizational memberships, e.g.. APRA, AFP especially in new Territory Gain a better understanding of the charities within a particular charitable sector, e.g.. Arts organizations Find out which charities do work in which countries Find out which organizations have had their charitable status revoked and who has been involved with them Find out which organizations have failed to file Investable assets and marketing investment services 82

83 Specific Examples (Cont) Real estate the property management New Foundations with large assets and their directors How much money is CIDA providing for foreign activities and to whom 83

84 Obtaining a Copy of T3010 Database you can request electronic versions of the lists by calling or toll free , or by sending an to charitylistings- ListeBienfaisance@cra-arc.gc.ca. 84

85 We have created four websites to use technology to inform and provide accessible, understandable information for free to the Canadian public

86 86

87 ? 87

88 88

89 89

90 Other Sources of Information Industry Canada Search for a Federal Corporation ale=en_ca Under CNCA pay for documents but can get them. CRA Can request copies letters patent, by-laws, charity application Financial Statements 90

91 Recent Developments CHAMP CRA Charities Modernization Program November 2018 will be able to file T3010 electronically Using CRA s My Business Account (MyBA) secure online portal, charities will be able to: 1)File T3010 (can also use paper based) 2) Charity applications (only electronically from November on) 3) Change certain account information and upload documents 4) Correspond with CRA electronically through portal 91

92 Effect of CHAMP Registered charities should open a My Business Account (MyBA) if they don t have one Charities listing may look different Eventually but not now more questions or changes to content of T3010 Quicker processing of T3010 information and availability to public Will reduce CRA error in inputting but not charity human error 92

93 Mockup of Champ interface My BA from CRA 93

94 Mockup of T3010 from CRA 94

95 Ideas to Improve Transparency Ask stakeholders what information they want. Update website Provided audited financial statements on website Provide simplified financial information as well. Have directors and non-finance staff review T3010 before filing Start preparing T months before filing date Try to file T3010 on time (sooner filed, sooner posted) Improve knowledge of those people filing form 95

96 Ideas to Improve Transparency Check for mistakes in past T3010 filings Utilize social media to increase access to important information What languages do stakeholders require Is mission within legal objects? Provide links to your information on CRA, etc? Provide details of value of the contribution of volunteers Have a policy on transparency, reserve funds etc. 96

97 Ideas to Improve Transparency Discuss impact Describe affiliated entities, subsidiaries etc. (and be mindful of the disclosure requirements or lack thereof for such entities) Tell CRA you are using the T3010 information Ask Finance to changes s. 241 of the Income Tax Act (Canada) to allow release of information on non-profits who file T1044 and charities that are abusing the system. 97

98 Thank you! Blumberg Segal LLP Barristers & Solicitors 390 Bay Street, Suite 1202 Toronto, Ontario, M5H 2Y2 Tel. (416) ext. 237 Toll Free (866) Fax. (416) Twitter at: and 98

CRA Questions on Charities Assisting Those Affected by the Conflict in Syria

CRA Questions on Charities Assisting Those Affected by the Conflict in Syria By Mark Blumberg (January 22, 2018) Many Canadian citizens and registered charities have assisted Syrian refugees over the last

CRA Questions on Charities Assisting Those Affected by the Conflict in Syria By Mark Blumberg (January 22, 2018) Many Canadian citizens and registered charities have assisted Syrian refugees over the last

Fundraising by registered charities

Home Taxes Charities and giving Charities Policies and guidance Fundraising by registered charities Guidance Reference number CG-013 Issued April 20, 2012 This guidance updates and replaces the previous

Home Taxes Charities and giving Charities Policies and guidance Fundraising by registered charities Guidance Reference number CG-013 Issued April 20, 2012 This guidance updates and replaces the previous

Talking Pointss. ng in 2009.

1 Talking Pointss CBCC Article: Charities paid $762M to private fundraisers. The Scope of Telemarketing ng is an important aspect of fundraising for some charities, but it is not widely used. According

1 Talking Pointss CBCC Article: Charities paid $762M to private fundraisers. The Scope of Telemarketing ng is an important aspect of fundraising for some charities, but it is not widely used. According

Common Errors on the T3010 related to fundraising costs. Know how to avoid them

Common Errors on the T3010 related to fundraising costs Know how to avoid them 1 Focus of presentation Many errors that charities make in the reporting of their fundraising expenses on the T3010 occur

Common Errors on the T3010 related to fundraising costs Know how to avoid them 1 Focus of presentation Many errors that charities make in the reporting of their fundraising expenses on the T3010 occur

1.1 Charitable Fundraising Strategy

KIWANIS CLUB OF OTTAWA 1.1 Charitable Fundraising Strategy 2013-14 Business Year Release 1.0 This strategy provides the policy and processes to conduct KCO fundraising activities from public sources for

KIWANIS CLUB OF OTTAWA 1.1 Charitable Fundraising Strategy 2013-14 Business Year Release 1.0 This strategy provides the policy and processes to conduct KCO fundraising activities from public sources for

FREQUENTLY ASKED QUESTIONS. Table of Contents

FREQUENTLY ASKED QUESTIONS Table of Contents What is United Way? 2 What geographical area does United Way of the Alberta Capital Region serve? 2 How do I get involved with United Way? 2-3 Does organized

FREQUENTLY ASKED QUESTIONS Table of Contents What is United Way? 2 What geographical area does United Way of the Alberta Capital Region serve? 2 How do I get involved with United Way? 2-3 Does organized

Canada Cultural Investment Fund (CCIF)

") Canada Cultural Investment Fund (CCIF) Endowment Incentives Component Guidelines Endowment Incentives 1 This publication is available in PDF format on the Internet at http://www.pch.gc.ca/eng/1268614803109#a5

Canada Cultural Investment Fund (CCIF) Endowment Incentives Component Guidelines Endowment Incentives 1 This publication is available in PDF format on the Internet at http://www.pch.gc.ca/eng/1268614803109#a5

distinction as to race, religion, age or disability, and in compliance with relevant legislation.

People and Places - Standard terms and conditions of grant Definitions We and our refer to the organisation receiving the grant bound by these terms and conditions. You and your means the Big Lottery Fund

People and Places - Standard terms and conditions of grant Definitions We and our refer to the organisation receiving the grant bound by these terms and conditions. You and your means the Big Lottery Fund

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS. National Historical Publications and Records Commission

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

MEMORANDUM OF UNDERSTANDING THE CHARITY COMMISSION FOR NORTHERN IRELAND AND THE FUNDRAISING REGULATOR

MEMORANDUM OF UNDERSTANDING THE CHARITY COMMISSION FOR NORTHERN IRELAND AND THE FUNDRAISING REGULATOR 1 Contents 1. Introduction 2. Objectives of the memorandum 3. Functions of the Commission 4. Functions

MEMORANDUM OF UNDERSTANDING THE CHARITY COMMISSION FOR NORTHERN IRELAND AND THE FUNDRAISING REGULATOR 1 Contents 1. Introduction 2. Objectives of the memorandum 3. Functions of the Commission 4. Functions

SAMPLE. Henry Smith Charity Christian Projects. Your organisation. Organisation Contact Details. 1. Organisation Name. 2. Organisation's Legal Name

Henry Smith Charity Christian Projects Application Form Page 1 of 10 Henry Smith Charity Christian Projects Application Form Your organisation Organisation Contact Details Please note: On the longer questions

Henry Smith Charity Christian Projects Application Form Page 1 of 10 Henry Smith Charity Christian Projects Application Form Your organisation Organisation Contact Details Please note: On the longer questions

What Canadian Donors Want

What Canadian Donors Want Most (71%) Canadians Agree that Charities Play an Important Role in Society Addressing Needs Not Being Met by the Public/Private Sectors Conducting Fundraising Campaigns Tops

What Canadian Donors Want Most (71%) Canadians Agree that Charities Play an Important Role in Society Addressing Needs Not Being Met by the Public/Private Sectors Conducting Fundraising Campaigns Tops

Charities Partnership and Outreach Program. Funding Guide and Application

Funding Guide and Application Please Read This Guide Carefully Before Preparing Your Funding Application RC4411(E) Rev 09 Table of Contents Introduction Funding Eligibility Objectives of the Current funding

Funding Guide and Application Please Read This Guide Carefully Before Preparing Your Funding Application RC4411(E) Rev 09 Table of Contents Introduction Funding Eligibility Objectives of the Current funding

Debunking the Myths of Charity Overhead. By: Caroline Riseboro

Debunking the Myths of Charity Overhead By: Caroline Riseboro caroline.riseboro@camh.ca Twitter: @criseboro Learning Outcomes Identifying the popular myths and counterarguments on charity overhead Understand

Debunking the Myths of Charity Overhead By: Caroline Riseboro caroline.riseboro@camh.ca Twitter: @criseboro Learning Outcomes Identifying the popular myths and counterarguments on charity overhead Understand

LOTTERY LICENCE ELIGIBILITY

PLANNING and BUILDING DEPARTMENT Licensing Office - Building 426 Brant Street, P.O. Box 5013 Burlington, ON L7R 3Z6 Tel: 905-335-7731 Fax: 905-335-7876 LOTTERY LICENCE ELIGIBILITY GENERAL INFORMATION:

PLANNING and BUILDING DEPARTMENT Licensing Office - Building 426 Brant Street, P.O. Box 5013 Burlington, ON L7R 3Z6 Tel: 905-335-7731 Fax: 905-335-7876 LOTTERY LICENCE ELIGIBILITY GENERAL INFORMATION:

NOT-FOR-PROFIT INSIDER

NOT-FOR-PROFIT INSIDER VOLUME 11 :: ISSUE 3 In This Issue: Challenges For Nonprofits In 2017: Fulfilling Mission Goals With Flexible Strategies Presenting The Financial Statements With Appeal To Major

NOT-FOR-PROFIT INSIDER VOLUME 11 :: ISSUE 3 In This Issue: Challenges For Nonprofits In 2017: Fulfilling Mission Goals With Flexible Strategies Presenting The Financial Statements With Appeal To Major

INNOSPEC INC. GIFTS, HOSPITALITY, CHARITABLE CONTRIBUTIONS, AND SPONSORSHIPS POLICY

INNOSPEC INC. GIFTS, HOSPITALITY, CHARITABLE CONTRIBUTIONS, AND SPONSORSHIPS POLICY CONTENTS 1. INTRODUCTION... 1 2. SCOPE... 1 3. GENERAL RULE... 1 4. DEFINITIONS... 2 5. GIFTS... 2 5.1 GIFTS PROCESS

INNOSPEC INC. GIFTS, HOSPITALITY, CHARITABLE CONTRIBUTIONS, AND SPONSORSHIPS POLICY CONTENTS 1. INTRODUCTION... 1 2. SCOPE... 1 3. GENERAL RULE... 1 4. DEFINITIONS... 2 5. GIFTS... 2 5.1 GIFTS PROCESS

FY2016 Grant Application Workshop. Basics of Financial Management for Grant Applicants

FY2016 Grant Application Workshop Basics of Financial Management for Grant Applicants Jerron M. Johnson Chief Field Program Officer Missouri Community Service Commission November 19, 2015 Session Overview

FY2016 Grant Application Workshop Basics of Financial Management for Grant Applicants Jerron M. Johnson Chief Field Program Officer Missouri Community Service Commission November 19, 2015 Session Overview

Cultural Competency Initiative. Program Guidelines

New Jersey STOP Violence Against Women (VAWA) Grants Program Cultural Competency Initiative Cultural Competency Technical Assistance Project Program Guidelines State Office of Victim Witness Advocacy Division

New Jersey STOP Violence Against Women (VAWA) Grants Program Cultural Competency Initiative Cultural Competency Technical Assistance Project Program Guidelines State Office of Victim Witness Advocacy Division

Shared Spaces Learning Series

Shared Spaces Learning Series KNOWLEDGE IN ACTION 1: CORPORATE STRUCTURES AND REGULATORY CONTEXT Roman Katsnelson Erin McFarlane NCN Canada: A Program of Tides Canada NCN Canada and the Shared Spaces Learning

Shared Spaces Learning Series KNOWLEDGE IN ACTION 1: CORPORATE STRUCTURES AND REGULATORY CONTEXT Roman Katsnelson Erin McFarlane NCN Canada: A Program of Tides Canada NCN Canada and the Shared Spaces Learning

Overview of CRA s Guidance on Expenditures for Fundraising Activities

Overview of CRA s Guidance on Expenditures for Fundraising Activities Podcast [Transcript] This is a Charity Central podcast. Charity Central provides information and resource material to registered charities

Overview of CRA s Guidance on Expenditures for Fundraising Activities Podcast [Transcript] This is a Charity Central podcast. Charity Central provides information and resource material to registered charities

CHARITY LAW BULLETIN NO. 318

CHARITY LAW BULLETIN NO. 318 AUGUST 28, 2013 EDITOR: TERRANCE S. CARTER CRA GUIDANCE ON HOW TO DRAFT PURPOSES FOR CHARITABLE REGISTRATION By Jennifer M. Leddy and Terrance S. Carter * A. INTRODUCTION On

CHARITY LAW BULLETIN NO. 318 AUGUST 28, 2013 EDITOR: TERRANCE S. CARTER CRA GUIDANCE ON HOW TO DRAFT PURPOSES FOR CHARITABLE REGISTRATION By Jennifer M. Leddy and Terrance S. Carter * A. INTRODUCTION On

INNOSPEC GROUP GIVING AND RECEIVING GIFTS & HOSPITALITIES PROCEDURES

INNOSPEC GROUP GIVING AND RECEIVING GIFTS & HOSPITALITIES PROCEDURES I : company documents/corporate policies / current / Giving and receiving gifts and hospitalities procedures English Uploaded 27.07.11

INNOSPEC GROUP GIVING AND RECEIVING GIFTS & HOSPITALITIES PROCEDURES I : company documents/corporate policies / current / Giving and receiving gifts and hospitalities procedures English Uploaded 27.07.11

Form 1023 Checklist (Revised June 2006)

") Form 1023 Checklist (Revised June 2006) Application for Recognition of Exemption under Section 501(c)(3) of the Internal Revenue Code Note. Retain a copy of the completed Form 1023 in your permanent records.

Form 1023 Checklist (Revised June 2006) Application for Recognition of Exemption under Section 501(c)(3) of the Internal Revenue Code Note. Retain a copy of the completed Form 1023 in your permanent records.

Guidelines: Comic Relief Local Communities Core Strength Grant

Guidelines: Comic Relief Local Communities Core Strength Grant Who are Quartet Community Foundation? Quartet Community Foundation manages funding on behalf of individuals, companies, charitable trusts

Guidelines: Comic Relief Local Communities Core Strength Grant Who are Quartet Community Foundation? Quartet Community Foundation manages funding on behalf of individuals, companies, charitable trusts

COMIC RELIEF AWARDS THE GRANT TO YOU, SUBJECT TO YOUR COMPLYING WITH THE FOLLOWING CONDITIONS:

Example conditions of grant Below are the standard conditions that we ask grant holders to sign up to when accepting a grant from Comic Relief. These conditions are provided here only as an example; we

Example conditions of grant Below are the standard conditions that we ask grant holders to sign up to when accepting a grant from Comic Relief. These conditions are provided here only as an example; we

STAGE ONE APPLICATION GUIDE

THE CHRISTMAS CHALLENGE 2018 Discover. Donate. Double. STAGE ONE APPLICATION GUIDE Monday 21st May Friday 6th July STAGE ONE APPLICATION GUIDE The application for The Christmas Challenge 2018 is divided

THE CHRISTMAS CHALLENGE 2018 Discover. Donate. Double. STAGE ONE APPLICATION GUIDE Monday 21st May Friday 6th July STAGE ONE APPLICATION GUIDE The application for The Christmas Challenge 2018 is divided

Inclusive Local Economies Program Guidelines

Inclusive Local Economies Program Guidelines Contents 1 Metcalf Foundation 2 Inclusive Local Economies Program 3 Opportunities Fund 8 Upcoming Application Deadlines 9 Opportunities Fund Application Cover

Inclusive Local Economies Program Guidelines Contents 1 Metcalf Foundation 2 Inclusive Local Economies Program 3 Opportunities Fund 8 Upcoming Application Deadlines 9 Opportunities Fund Application Cover

M I L L E R T H O M S O N LLP Barristers & Solicitors, Patent & Trade Mark Agents

M I L L E R T H O M S O N LLP Barristers & Solicitors, Patent & Trade Mark Agents Communiqué for Health Industry Clients on the Legal Retainer Program BOND Policy Business Oriented New Development ( BOND

M I L L E R T H O M S O N LLP Barristers & Solicitors, Patent & Trade Mark Agents Communiqué for Health Industry Clients on the Legal Retainer Program BOND Policy Business Oriented New Development ( BOND

GUIDELINES FOR FINANCIAL ASSISTANCE

GUIDELINES FOR FINANCIAL ASSISTANCE The submission of an application does not guarantee our assistance. JACC aspires to help as many children and families as possible with our limited funds: we guarantee

GUIDELINES FOR FINANCIAL ASSISTANCE The submission of an application does not guarantee our assistance. JACC aspires to help as many children and families as possible with our limited funds: we guarantee

The YAS Charity exists to support the work of the Yorkshire Ambulance Service NHS Trust.

YAS Charity Fundraising Strategy 2018 2021 Introduction The purpose of this Fundraising Strategy is to guide the YAS Charity to carry out tasks in the most coordinated and effective way. It is to inform

YAS Charity Fundraising Strategy 2018 2021 Introduction The purpose of this Fundraising Strategy is to guide the YAS Charity to carry out tasks in the most coordinated and effective way. It is to inform

HIPAA PRIVACY NOTICE

HIPAA PRIVACY NOTICE PLEASE REVIEW THIS NOTICE CAREFULLY. IT DESCRIBES HOW YOUR MEDICAL INFORMATION MAY BE USED AND DISCLOSED AND HOW YOU MAY GAIN ACCESS TO THAT INFORMATION. POLICY STATEMENT This Practice

HIPAA PRIVACY NOTICE PLEASE REVIEW THIS NOTICE CAREFULLY. IT DESCRIBES HOW YOUR MEDICAL INFORMATION MAY BE USED AND DISCLOSED AND HOW YOU MAY GAIN ACCESS TO THAT INFORMATION. POLICY STATEMENT This Practice

AFP Fundraising Day 2018 Tuesday June 12, 2018 Metro Toronto Convention Centre, North Building

AFP Fundraising Day 2018 Tuesday June 12, 2018 Metro Toronto Convention Centre, North Building BURSARY APPLICATION FORM The AFP Foundation for Philanthropy - Canada supports this Bursary Program as part

AFP Fundraising Day 2018 Tuesday June 12, 2018 Metro Toronto Convention Centre, North Building BURSARY APPLICATION FORM The AFP Foundation for Philanthropy - Canada supports this Bursary Program as part

American Friends of Canadian Land Trusts. American Friends of Canadian Land Trusts. Grantee Application 1

American Friends of Canadian Land Trusts Grantee Application Grantee Application 1 APPLICATION CHECKLIST Thank you for your interest in becoming a grantee with the American Friends of Canadian Land Trusts

American Friends of Canadian Land Trusts Grantee Application Grantee Application 1 APPLICATION CHECKLIST Thank you for your interest in becoming a grantee with the American Friends of Canadian Land Trusts

Culture Projects Grant Program

2019 Guidelines Culture Projects Grant Program Grant applications are due Friday, October 12, 2018 by 4:30 PM Due Date: Friday, October 12, 1, 2018 by 4:30pm Table of Contents Program Purpose..........

2019 Guidelines Culture Projects Grant Program Grant applications are due Friday, October 12, 2018 by 4:30 PM Due Date: Friday, October 12, 1, 2018 by 4:30pm Table of Contents Program Purpose..........

State of Kansas Community Service Tax Credit FY2019 Application Guidelines (For projects starting July 1, 2018 And ending December 31, 2019)

") State of Kansas Community Service Tax Credit FY2019 Application Guidelines (For projects starting July 1, 2018 And ending December 31, 2019) 1000 S.W. Jackson Street, Suite 100 Topeka, KS 66612-1354 Phone:

State of Kansas Community Service Tax Credit FY2019 Application Guidelines (For projects starting July 1, 2018 And ending December 31, 2019) 1000 S.W. Jackson Street, Suite 100 Topeka, KS 66612-1354 Phone:

NOTICE OF PRIVACY PRACTICES

535 East 70th Street New York, NY 10021 (212) 606-1000 Specialists in Mobility NOTICE OF PRIVACY PRACTICES Effective Date: April 14, 2003 THIS NOTICE DESCRIBES HOW MEDICAL INFORMATION ABOUT YOU MAY BE

535 East 70th Street New York, NY 10021 (212) 606-1000 Specialists in Mobility NOTICE OF PRIVACY PRACTICES Effective Date: April 14, 2003 THIS NOTICE DESCRIBES HOW MEDICAL INFORMATION ABOUT YOU MAY BE

Uniform Grants Guidance. Colorado Charter School Institute Cassie Walgren, Controller

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

Uniform Grants Guidance Colorado Charter School Institute Cassie Walgren, Controller 1 Agenda 1. Introduction 2. EDGAR and C.F.R. 3. Financial Management Rules 4. Cost Principles 5. Procurement 6. Time

Charitable Giving Grant Application 2014

Charitable Giving Grant Application 2014 Our Vision A world with increased opportunity for all, through better access to education and technology. Our Mission Our mission is to leverage Blackboard s unique

Charitable Giving Grant Application 2014 Our Vision A world with increased opportunity for all, through better access to education and technology. Our Mission Our mission is to leverage Blackboard s unique

CHARITY LAW BULLETIN NO. 349

CHARITY LAW BULLETIN NO. 349 SEPTEMBER 25, 2014 EDITOR: TERRANCE S. CARTER IMAGINE CANADA REPORT ON CANADA S GRANTMAKING FOUNDATIONS By Terrance S. Carter * A. INTRODUCTION On September 4, 2014, Imagine

CHARITY LAW BULLETIN NO. 349 SEPTEMBER 25, 2014 EDITOR: TERRANCE S. CARTER IMAGINE CANADA REPORT ON CANADA S GRANTMAKING FOUNDATIONS By Terrance S. Carter * A. INTRODUCTION On September 4, 2014, Imagine

CALL FOR PROPOSALS FALL 2018

CALL FOR PROPOSALS FALL 2018 Proposal Deadline: August 31, 2018 Funding Available for Grants: $1,000 - $20,000 BACKGROUND The Ceramic and Glass Industry Foundation (CGIF) was created to attract, inspire,

CALL FOR PROPOSALS FALL 2018 Proposal Deadline: August 31, 2018 Funding Available for Grants: $1,000 - $20,000 BACKGROUND The Ceramic and Glass Industry Foundation (CGIF) was created to attract, inspire,

Guide to. Grant Aid Agreement Document. Section 39 Health Act, 2004 Section 10 Child Care Act, 1991 National Lottery

Guide to Grant Aid Agreement Document Section 39 Health Act, 2004 Section 10 Child Care Act, 1991 National Lottery Please note that this document provides an explanatory guide to the document but is not

Guide to Grant Aid Agreement Document Section 39 Health Act, 2004 Section 10 Child Care Act, 1991 National Lottery Please note that this document provides an explanatory guide to the document but is not

General Eligibility And Funding Guidelines

The Ounce of Prevention Fund of Florida General Eligibility And Funding Guidelines Revised March 2018 The Ounce of Prevention Fund of Florida The Ounce of Prevention Fund of Florida 1 INTRODUCTION The

The Ounce of Prevention Fund of Florida General Eligibility And Funding Guidelines Revised March 2018 The Ounce of Prevention Fund of Florida The Ounce of Prevention Fund of Florida 1 INTRODUCTION The

The Ford Foundation EQUIVALENCY AFFIDAVIT PACKET FOR NON-U.S. GRANT APPLICANTS

The Ford Foundation EQUIVALENCY AFFIDAVIT PACKET FOR NON-U.S. GRANT APPLICANTS This packet includes: INTRODUCTION "EQUIVALENCY AFFIDAVIT FOR NON-U.S. ORGANIZATIONS" AND INSTRUCTIONS "PUBLIC SUPPORT SCHEDULE"

The Ford Foundation EQUIVALENCY AFFIDAVIT PACKET FOR NON-U.S. GRANT APPLICANTS This packet includes: INTRODUCTION "EQUIVALENCY AFFIDAVIT FOR NON-U.S. ORGANIZATIONS" AND INSTRUCTIONS "PUBLIC SUPPORT SCHEDULE"

PTA fundraising activities are carried out by a committee whose chairman is an appointed or elected member of the executive board.

Fundraising for PTAs Home Page> Finance > Fundraising for PTAs Fundraising is the method of raising money to finance PTA programs and projects. The fund-raising project must support the goals of PTA and

Fundraising for PTAs Home Page> Finance > Fundraising for PTAs Fundraising is the method of raising money to finance PTA programs and projects. The fund-raising project must support the goals of PTA and

10 CFR 600: KNOW YOUR REQUIREMENTS

WEATHERIZATION ASSISTANCE PROGRAM 10 CFR 600: KNOW YOUR REQUIREMENTS Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and

WEATHERIZATION ASSISTANCE PROGRAM 10 CFR 600: KNOW YOUR REQUIREMENTS Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and

Fundraising. Standards for PTA Fundraising

Fundraising The primary emphasis in PTA should be the promotion of the PTA Mission and Purposes of the PTA. The real working capital of a PTA lies in its members, not in its treasury. PTAs do not exist

Fundraising The primary emphasis in PTA should be the promotion of the PTA Mission and Purposes of the PTA. The real working capital of a PTA lies in its members, not in its treasury. PTAs do not exist

THE DORSEY & WHITNEY FOUNDATION

External Application THE DORSEY & WHITNEY FOUNDATION To determine whether to submit a request to The Dorsey & Whitney Foundation (the Foundation ), please review the guidelines below. To submit a request,

External Application THE DORSEY & WHITNEY FOUNDATION To determine whether to submit a request to The Dorsey & Whitney Foundation (the Foundation ), please review the guidelines below. To submit a request,

Community Initiatives Program Major Cultural and Sport Events

Community Initiatives Program Major Cultural and Sport Events Program Guidelines November 2016 Table of Contents 1. Purpose and Objectives 3 2. CIP Major Cultural and Sport Events stream..3 3. Program

Community Initiatives Program Major Cultural and Sport Events Program Guidelines November 2016 Table of Contents 1. Purpose and Objectives 3 2. CIP Major Cultural and Sport Events stream..3 3. Program

University of Florida Foundation, Inc. Financial and Compliance Report June 30, 2016

University of Florida Foundation, Inc. Financial and Compliance Report Contents Independent auditor s report 1-2 Financial statements Statement of financial position 3 Statement of activities 4 Statement

University of Florida Foundation, Inc. Financial and Compliance Report Contents Independent auditor s report 1-2 Financial statements Statement of financial position 3 Statement of activities 4 Statement

Legal and Ethical Issues for Foundations

Legal and Ethical Issues for Foundations Delaware Valley Grantmakers Fundamentals of Smart Grantmaking Series January 11, 2012 Nina L. Cohen, Managing Director, Philanthropic Advisory Services 215-419-6722

Legal and Ethical Issues for Foundations Delaware Valley Grantmakers Fundamentals of Smart Grantmaking Series January 11, 2012 Nina L. Cohen, Managing Director, Philanthropic Advisory Services 215-419-6722

Wage Subsidy Community Coordinator

Wage Subsidy Community Coordinator Program Guidelines Advanced Education and Skills Government of Newfoundland and Labrador Version 1.1 Effective Date April 1, 2014 Table of Contents 1. Wage Subsidy Community

Wage Subsidy Community Coordinator Program Guidelines Advanced Education and Skills Government of Newfoundland and Labrador Version 1.1 Effective Date April 1, 2014 Table of Contents 1. Wage Subsidy Community

Services that help donors give their support more generously

Working Together The Fidelity Charitable Gift Fund is an independent public charity Like your organization, we are also a nonprofit. Our donor advised fund program, called the Giving Account, helps us

Working Together The Fidelity Charitable Gift Fund is an independent public charity Like your organization, we are also a nonprofit. Our donor advised fund program, called the Giving Account, helps us

Trends in Nonprofit Accountability and Its Impact on Reporting Requirements

Trends in Nonprofit Accountability and Its Impact on Reporting Requirements Increased Stewardship and Accountability Requirements Raises the Importance of Integrated, Accurate, and Easy-to-Use Reporting

Trends in Nonprofit Accountability and Its Impact on Reporting Requirements Increased Stewardship and Accountability Requirements Raises the Importance of Integrated, Accurate, and Easy-to-Use Reporting

Am I eligible to participate in The Home Depot Foundation Matching Gift Program?

FAQ FAQ - Matching Gift Program What is the Matching Gift Program? Am I eligible to participate in The Home Depot Foundation Matching Gift Program? How does the Matching Gift Program work? How do I register

FAQ FAQ - Matching Gift Program What is the Matching Gift Program? Am I eligible to participate in The Home Depot Foundation Matching Gift Program? How does the Matching Gift Program work? How do I register

Scouts Scotland Fundraising Charter

Scouts Scotland Fundraising Charter This acts as a summary statement of our fundraising principles and methods, will sit on the website and is available for any enquiries. Anyone who is kind enough to

Scouts Scotland Fundraising Charter This acts as a summary statement of our fundraising principles and methods, will sit on the website and is available for any enquiries. Anyone who is kind enough to

City of Brantford. Terms of Eligibility Annual Operating Grants

Description of Program City of Brantford Community Cultural Investment Program 2017 Terms of Eligibility Annual Operating Grants Funded by the City of Brantford, the goals for the Community Cultural Investment

Description of Program City of Brantford Community Cultural Investment Program 2017 Terms of Eligibility Annual Operating Grants Funded by the City of Brantford, the goals for the Community Cultural Investment

REQUIREMENTS FOR LOTTERY LICENCE ELIGIBILITY

REQUIREMENTS FOR LOTTERY LICENCE ELIGIBILITY PLANNING and BUILDING DEPARTMENT Licensing Office - Building 426 Brant Street, P.O. Box 5013 Burlington, ON L7R 3Z6 Tel: 905-335-7731 Fax: 905-335-7876 To be

REQUIREMENTS FOR LOTTERY LICENCE ELIGIBILITY PLANNING and BUILDING DEPARTMENT Licensing Office - Building 426 Brant Street, P.O. Box 5013 Burlington, ON L7R 3Z6 Tel: 905-335-7731 Fax: 905-335-7876 To be

Renaissance Charitable Foundation Inc. Grantmaking Due Diligence Policy

Renaissance Charitable Foundation Inc. Grantmaking Due Diligence Policy I. Overview It is the policy of Renaissance Charitable Foundation Inc. (Foundation) to perform due diligence procedures on each grant

Renaissance Charitable Foundation Inc. Grantmaking Due Diligence Policy I. Overview It is the policy of Renaissance Charitable Foundation Inc. (Foundation) to perform due diligence procedures on each grant

BACKGROUND. CPB Community Service Grant

This report presents the conclusions of the OIG. The findings and recommendations presented in this report do not necessarily represent CPB s final position on these matters. CPB officials will make a

This report presents the conclusions of the OIG. The findings and recommendations presented in this report do not necessarily represent CPB s final position on these matters. CPB officials will make a

South Central Ambulance Charity: Policy on eligible expenditure and Procedure for disbursement of funds.

South Central Ambulance Charity: Policy on eligible expenditure and Procedure for disbursement of funds. Updated by the Charitable Funds Sub Committee, April 26 th 2017 1. Legal context The South Central

South Central Ambulance Charity: Policy on eligible expenditure and Procedure for disbursement of funds. Updated by the Charitable Funds Sub Committee, April 26 th 2017 1. Legal context The South Central

Matching Gifts Program

Matching Gifts Program GUIDELINES OVERVIEW The Matching Gifts Program is an important part our community investments strategy and one of the ways Tesoro, in partnership with the Tesoro Foundation, supports

Matching Gifts Program GUIDELINES OVERVIEW The Matching Gifts Program is an important part our community investments strategy and one of the ways Tesoro, in partnership with the Tesoro Foundation, supports

CITY OF ABBOTSFORD PERMISSIVE PROPERTY TAX EXEMPTION. Policy No. C REVISIONS. Revision No. Date Approved Description

CITY OF ABBOTSFORD PERMISSIVE PROPERTY TAX EXEMPTION Policy No. C008-05 REVISIONS Revision No. Date Approved Description 1 10 24 2016 Updates requirements and eligibility criteria. PAGE 1 OF 14 COUNCIL

CITY OF ABBOTSFORD PERMISSIVE PROPERTY TAX EXEMPTION Policy No. C008-05 REVISIONS Revision No. Date Approved Description 1 10 24 2016 Updates requirements and eligibility criteria. PAGE 1 OF 14 COUNCIL

TITLE. Subtitle. Is Your Charity Tax Status at Risk?

TITLE Subtitle Is Your Charity Tax Status at Risk? Is Your Charity Tax Status at Risk? Chair Lyne Bouret Controller (Interim) Concordia University Barry Travers - Partner KPMG LLP Presenters Joanne McKee

TITLE Subtitle Is Your Charity Tax Status at Risk? Is Your Charity Tax Status at Risk? Chair Lyne Bouret Controller (Interim) Concordia University Barry Travers - Partner KPMG LLP Presenters Joanne McKee

NOT-FOR-PROFIT INSIDER

NOT-FOR-PROFIT INSIDER VOLUME 9 :: ISSUE 3 In This Issue: Streamlining OMB Guidance For Federal Funding Of Nonprofit Organizations New 1023-EZ Makes Applying For 501(C)(3) Tax-Exempt Status Easier Identifying

NOT-FOR-PROFIT INSIDER VOLUME 9 :: ISSUE 3 In This Issue: Streamlining OMB Guidance For Federal Funding Of Nonprofit Organizations New 1023-EZ Makes Applying For 501(C)(3) Tax-Exempt Status Easier Identifying

Ontario Black Youth Action Plan

Ontario Black Youth Action Plan Innovative Supports for Black Parents Initiative Application Questions and Answers The following document responds to all questions received by the Ministry of Children

Ontario Black Youth Action Plan Innovative Supports for Black Parents Initiative Application Questions and Answers The following document responds to all questions received by the Ministry of Children

NOTICE OF PRIVACY PRACTICES

THIS NOTICE OF PRIVACY PRACTICES ( NOTICE ) DESCRIBES HOW MEDICAL INFORMATION ABOUT YOU MAY BE USED AND DISCLOSED, AND HOW YOU CAN GET ACCESS TO THIS INFORMATION. PLEASE REVIEW IT CAREFULLY. Respect for

THIS NOTICE OF PRIVACY PRACTICES ( NOTICE ) DESCRIBES HOW MEDICAL INFORMATION ABOUT YOU MAY BE USED AND DISCLOSED, AND HOW YOU CAN GET ACCESS TO THIS INFORMATION. PLEASE REVIEW IT CAREFULLY. Respect for

Cambridge House s Ethical Fundraising Policy & Procedures

Contents Page A. Introduction 2 B. Policy Management and Implementation 2 C. Policy Aims 2 D. Context 3 E. Relationship with Supporters 4 F. Risk Assessment 4 G. Commercial Partners 4 H. Anonymous Donations

Contents Page A. Introduction 2 B. Policy Management and Implementation 2 C. Policy Aims 2 D. Context 3 E. Relationship with Supporters 4 F. Risk Assessment 4 G. Commercial Partners 4 H. Anonymous Donations

Program Rules & Guidelines: Matching Gifts Revised April 10, 2012

Program Rules & Guidelines: Matching Gifts Revised April 10, 2012 The JPMorgan Chase Matching Gifts Program maximizes the impact of employee charitable giving by allowing an eligible employee to suggest

Program Rules & Guidelines: Matching Gifts Revised April 10, 2012 The JPMorgan Chase Matching Gifts Program maximizes the impact of employee charitable giving by allowing an eligible employee to suggest

CHARITABLE SOLICITATION What does it take to be compliant? Presented by: Ify Aduba

CHARITABLE SOLICITATION What does it take to be compliant? Presented by: Ify Aduba Introduction To Harbor Compliance Harbor Compliance provides services and software to help executive teams and boards

CHARITABLE SOLICITATION What does it take to be compliant? Presented by: Ify Aduba Introduction To Harbor Compliance Harbor Compliance provides services and software to help executive teams and boards

CHARITY LAW BULLETIN NO. 329

CHARITY LAW BULLETIN NO. 329 JANUARY 29, 2014 EDITOR: TERRANCE S. CARTER CRA GUIDANCE ON PROMOTION OF HEALTH AND CHARITABLE REGISTRATION By Terrance S. Carter & Karen J. Cooper * A. INTRODUCTION Canada

CHARITY LAW BULLETIN NO. 329 JANUARY 29, 2014 EDITOR: TERRANCE S. CARTER CRA GUIDANCE ON PROMOTION OF HEALTH AND CHARITABLE REGISTRATION By Terrance S. Carter & Karen J. Cooper * A. INTRODUCTION Canada

Bridging Divides How to apply for a grant

Bridging Divides How to apply for a grant City Bridge Trust wants to support high quality work that will help us meet our priorities. These guidelines are intended to help you understand our application

Bridging Divides How to apply for a grant City Bridge Trust wants to support high quality work that will help us meet our priorities. These guidelines are intended to help you understand our application

A Handbook for Local Leagues Including Procedures and Forms. THE LEAGUE OF WOMEN VOTERS of Washington Education Fund. Revised January 2015

YOUR EDUCATION FUND A Handbook for Local Leagues Including Procedures and Forms THE LEAGUE OF WOMEN VOTERS of Washington Education Fund Revised January 2015 (approved 1/21/2015-C3 Board) THE LEAGUE OF

YOUR EDUCATION FUND A Handbook for Local Leagues Including Procedures and Forms THE LEAGUE OF WOMEN VOTERS of Washington Education Fund Revised January 2015 (approved 1/21/2015-C3 Board) THE LEAGUE OF

STAGE ONE APPLICATION GUIDE

CHRISTMAS CHALLENGE 2017 Discover. Donate. Double. STAGE ONE APPLICATION GUIDE Monday 5th JuneFriday 7th July STAGE ONE APPLICATION GUIDE The application for the Christmas Challenge 2017 is divided into

CHRISTMAS CHALLENGE 2017 Discover. Donate. Double. STAGE ONE APPLICATION GUIDE Monday 5th JuneFriday 7th July STAGE ONE APPLICATION GUIDE The application for the Christmas Challenge 2017 is divided into

Terms & Conditions of Award

PART 1 1. INTRODUCTION 1 Terms & Conditions of Award 1.1. Part 1 of this Terms & Conditions of Award document sets out the standard terms and conditions for all British Academy awards. Additional terms

PART 1 1. INTRODUCTION 1 Terms & Conditions of Award 1.1. Part 1 of this Terms & Conditions of Award document sets out the standard terms and conditions for all British Academy awards. Additional terms

Minnesota health care price transparency laws and rules

Minnesota health care price transparency laws and rules Minnesota Statutes 2013 62J.81 DISCLOSURE OF PAYMENTS FOR HEALTH CARE SERVICES. Subdivision 1.Required disclosure of estimated payment. (a) A health

Minnesota health care price transparency laws and rules Minnesota Statutes 2013 62J.81 DISCLOSURE OF PAYMENTS FOR HEALTH CARE SERVICES. Subdivision 1.Required disclosure of estimated payment. (a) A health

EXPRESSION OF INTEREST. Niagara Homelessness Service System Funding July 2017-March Service Priority Supported Transitional Housing

EXPRESSION OF INTEREST Niagara Homelessness Service System Funding July 2017-March 2020 Service Priority Supported Transitional Housing DOCUMENT NUMBER 2017-EOI-04 ISSUE DATE: FEBRUARY 15, 2017 CLOSING

EXPRESSION OF INTEREST Niagara Homelessness Service System Funding July 2017-March 2020 Service Priority Supported Transitional Housing DOCUMENT NUMBER 2017-EOI-04 ISSUE DATE: FEBRUARY 15, 2017 CLOSING

Do-It-Yourself Prospect Research: Discovery Exciting and Innovative Research Methods You Can Take Back to Your Shop Today!

Do-It-Yourself Prospect Research: Discovery Exciting and Innovative Research Methods You Can Take Back to Your Shop Today! Tracey Church, MLIS, Tracey Church & Associates November 22, 2017 Metro Toronto

Do-It-Yourself Prospect Research: Discovery Exciting and Innovative Research Methods You Can Take Back to Your Shop Today! Tracey Church, MLIS, Tracey Church & Associates November 22, 2017 Metro Toronto

2010 Mauldin & Jenkins Single Audits for for Auditees

2010 Mauldin & Jenkins Single Audits for Auditees SINGLE AUDITS FOR AUDITEES Mauldin & Jenkins July 22, 2010 Macon August 3, 2010 - Atlanta PRESENTER Hope Pendergrass Manager Macon Office hpendergrass@mjcpa.com

2010 Mauldin & Jenkins Single Audits for Auditees SINGLE AUDITS FOR AUDITEES Mauldin & Jenkins July 22, 2010 Macon August 3, 2010 - Atlanta PRESENTER Hope Pendergrass Manager Macon Office hpendergrass@mjcpa.com

Updated March 21, 2018

Exhibit 1 INCUBATOR FISCAL SPONSORSHIP PROGRAM MANUAL Updated March 21, 2018 ABOUT THE PROGRAM... 2 ELIGIBILITY... 2 CREATIVE CONTROL AND INTELLECTUAL PROPERTY... 2 APPLICATION PROCESS... 2 PROGRAM FEES...

Exhibit 1 INCUBATOR FISCAL SPONSORSHIP PROGRAM MANUAL Updated March 21, 2018 ABOUT THE PROGRAM... 2 ELIGIBILITY... 2 CREATIVE CONTROL AND INTELLECTUAL PROPERTY... 2 APPLICATION PROCESS... 2 PROGRAM FEES...

Community Grant Program

Status of Women Community Grant Program Innovation Projects Guidelines 1 November Month 20XX 2017 Main Heading Sub-heading TABLE OF CONTENTS Purpose... 1 Eligibility... 2 Eligible Organizations... 2 Eligible

Status of Women Community Grant Program Innovation Projects Guidelines 1 November Month 20XX 2017 Main Heading Sub-heading TABLE OF CONTENTS Purpose... 1 Eligibility... 2 Eligible Organizations... 2 Eligible

CHAPTER 4: Income from Employment

CHAPTER 4: Income from Employment Prepared by Nathalie Johnstone University of Saskatchewan Electronic Presentations in Microsoft PowerPoint Copyright 2015 McGraw-Hill Ryerson, Limited. All rights reserved.

CHAPTER 4: Income from Employment Prepared by Nathalie Johnstone University of Saskatchewan Electronic Presentations in Microsoft PowerPoint Copyright 2015 McGraw-Hill Ryerson, Limited. All rights reserved.

Jeans for Genes Day Genetic Disorders UK. Guidance for Applicants JEANS FOR GENES DAY. Supporting families affected by genetic disorders

Jeans for Genes Day Genetic Disorders UK Guidance for Applicants JEANS FOR GENES DAY Supporting families affected by genetic disorders Contents 3 Jeans for Genes Day / Genetic Disorders UK 4 The 2015 Grant

Jeans for Genes Day Genetic Disorders UK Guidance for Applicants JEANS FOR GENES DAY Supporting families affected by genetic disorders Contents 3 Jeans for Genes Day / Genetic Disorders UK 4 The 2015 Grant

This form shows the information you have entered through the Charity Commission Online Application for Registration.

Charity Commission Apply to register a charity Organisation names Main name Paradise 4 Kids Other name or acronym Application number 5107147 Submission date 07/08/2017 Special circumstances If we decide

Charity Commission Apply to register a charity Organisation names Main name Paradise 4 Kids Other name or acronym Application number 5107147 Submission date 07/08/2017 Special circumstances If we decide

INNOSPEC INC GIFTS, HOSPITALITY, CHARITABLE CONTRIBUTIONS AND SPONSORSHIPS POLICY

INNOSPEC INC GIFTS, HOSPITALITY, CHARITABLE CONTRIBUTIONS AND SPONSORSHIPS POLICY CONTENTS 1. INTRODUCTION... 1 2. SCOPE... 1 3. GENERAL RULE... 1 4. DEFINITIONS... 2 5. GIFTS... 3 5.1 GIFTS PROCESS OVERVIEW...

INNOSPEC INC GIFTS, HOSPITALITY, CHARITABLE CONTRIBUTIONS AND SPONSORSHIPS POLICY CONTENTS 1. INTRODUCTION... 1 2. SCOPE... 1 3. GENERAL RULE... 1 4. DEFINITIONS... 2 5. GIFTS... 3 5.1 GIFTS PROCESS OVERVIEW...

PATIENT BILL OF RIGHTS & NOTICE OF PRIVACY PRACTICES

Helping People Perform Their Best PRIVACY, RIGHTS AND RESPONSIBILITIES NOTICE PATIENT BILL OF RIGHTS & NOTICE OF PRIVACY PRACTICES Request Additional Information or to Report a Problem If you have questions

Helping People Perform Their Best PRIVACY, RIGHTS AND RESPONSIBILITIES NOTICE PATIENT BILL OF RIGHTS & NOTICE OF PRIVACY PRACTICES Request Additional Information or to Report a Problem If you have questions

Accounting for Government Grants and Disclosure of Government Assistance

Indian Accounting Standard (Ind AS) 20 Accounting for Government Grants and Disclosure of Government Assistance (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which

Indian Accounting Standard (Ind AS) 20 Accounting for Government Grants and Disclosure of Government Assistance (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which

CITY FUNDING REQUEST GUIDELINES AND APPLICATION INSTRUCTIONS

CITY FUNDING REQUEST GUIDELINES AND APPLICATION INSTRUCTIONS INTRODUCTION One of the purposes of the Families, Parks and Recreation Advisory Board is to encourage and support events in the City of Orlando

CITY FUNDING REQUEST GUIDELINES AND APPLICATION INSTRUCTIONS INTRODUCTION One of the purposes of the Families, Parks and Recreation Advisory Board is to encourage and support events in the City of Orlando

FAQ. FAQ - Matching Gift Program. FAQ - Volunteer Grant Program. FAQ - Matching Gift Program

FAQ FAQ - Matching Gift Program What is the Charitable Matching Gift Program? Am I eligible to participate in The Home Depot Foundation Charitable Matching Gifts Program? How do I participate in The Home

FAQ FAQ - Matching Gift Program What is the Charitable Matching Gift Program? Am I eligible to participate in The Home Depot Foundation Charitable Matching Gifts Program? How do I participate in The Home

PRINCE ALBERT AND AREA COMMUNITY FOUNDATION GRANT APPLICATION GUIDELINES & FORM 2017

PRINCE ALBERT AND AREA COMMUNITY FOUNDATION GRANT APPLICATION GUIDELINES & FORM 2017 Please read Application Guidelines and complete as directed. It is your responsibility to ensure that this application

PRINCE ALBERT AND AREA COMMUNITY FOUNDATION GRANT APPLICATION GUIDELINES & FORM 2017 Please read Application Guidelines and complete as directed. It is your responsibility to ensure that this application

ROCKY MOUNTAIN TAX SEMINAR FOR PRIVATE FOUNDATIONS GRANT-MAKING PART I: ROUTINE GRANTS TO INDIVIDUALS AND PUBLIC CHARITIES

ROCKY MOUNTAIN TAX SEMINAR FOR PRIVATE FOUNDATIONS GRANT-MAKING PART I: ROUTINE GRANTS TO INDIVIDUALS AND PUBLIC CHARITIES September 11, 2013 Celia Roady, Esq. Morgan, Lewis & Bockius LLP 1111 Pennsylvania

ROCKY MOUNTAIN TAX SEMINAR FOR PRIVATE FOUNDATIONS GRANT-MAKING PART I: ROUTINE GRANTS TO INDIVIDUALS AND PUBLIC CHARITIES September 11, 2013 Celia Roady, Esq. Morgan, Lewis & Bockius LLP 1111 Pennsylvania

GST MANUAL 1. GST AND CHS P&C Why is Chatswood P&C Registered for GST? What things do we need to charge GST on? 2

GST MANUAL Contents 1. GST AND CHS P&C 2 1.1. Why is Chatswood P&C Registered for GST? 2 1.2. What things do we need to charge GST on? 2 1.3. How does charging GST and claiming back GST on purchases (input

GST MANUAL Contents 1. GST AND CHS P&C 2 1.1. Why is Chatswood P&C Registered for GST? 2 1.2. What things do we need to charge GST on? 2 1.3. How does charging GST and claiming back GST on purchases (input

Navigating the New Uniform Grant Guidance. Jack Reagan, Audit Partner Grant Thornton LLP. Grant Thornton. All rights reserved.

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

Navigating the New Uniform Grant Guidance Jack Reagan, Audit Partner Grant Thornton LLP Objectives What s New with OMB: Uniform Administrative Requirements, Cost Principles, and Audit requirements for

UCLA HEALTH SYSTEM CODE OF CONDUCT

UCLA HEALTH SYSTEM CODE OF CONDUCT STANDARD 1 - QUALITY OF CARE The University s health centers and health systems will provide quality health care that is appropriate, medically necessary, and efficient.

UCLA HEALTH SYSTEM CODE OF CONDUCT STANDARD 1 - QUALITY OF CARE The University s health centers and health systems will provide quality health care that is appropriate, medically necessary, and efficient.

PANEL ON THE NON-PROFIT SECTOR GOOD GOVERNANCE RECOMMENDATIONS

Panel on the Non-Profit Sector recommendations: Effectiveness and Relevance to Good Governance of Nonprofit, Tax-Exempt Arts Organizations Erin Puskar Shenandoah University 1 Abstract This article discusses

Panel on the Non-Profit Sector recommendations: Effectiveness and Relevance to Good Governance of Nonprofit, Tax-Exempt Arts Organizations Erin Puskar Shenandoah University 1 Abstract This article discusses

Sheds Grant Fund Grant Guidelines for all Applicants 2018

Sheds Grant Fund Grant Guidelines for all Applicants 2018 What is the Royal Voluntary Service / Asda Foundation Sheds Grant Fund? Royal Voluntary Service provides practical solutions to help older people

Sheds Grant Fund Grant Guidelines for all Applicants 2018 What is the Royal Voluntary Service / Asda Foundation Sheds Grant Fund? Royal Voluntary Service provides practical solutions to help older people

Terms and Conditions of studentship funding

Terms and Conditions of studentship funding Any offer of PhD funding from Brain Research UK ( the Charity ) is subject to the following Terms and Conditions. By accepting the award, the Host Institute

Terms and Conditions of studentship funding Any offer of PhD funding from Brain Research UK ( the Charity ) is subject to the following Terms and Conditions. By accepting the award, the Host Institute

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE AND OTHER SELECTED GRANTS AT KENTUCKY AUTHORITY FOR EDUCATIONAL TELEVISION, INC., KET-TV, LEXINGTON, KENTUCKY

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE AND OTHER SELECTED GRANTS AT KENTUCKY AUTHORITY FOR EDUCATIONAL TELEVISION, INC., KET-TV, LEXINGTON, KENTUCKY

Benefits Handbook Date March 1, Matching Gifts MMC

Date March 1, 2010 MMC Marsh & McLennan Companies values education as one of its most important investments. The to Education Program is designed to encourage the personal giving of employees and allows

Date March 1, 2010 MMC Marsh & McLennan Companies values education as one of its most important investments. The to Education Program is designed to encourage the personal giving of employees and allows

REQUEST FOR QUALIFICATIONS FOR CONSTRUCTION MANAGER-AT-RISK

REQUEST FOR QUALIFICATIONS FOR CONSTRUCTION MANAGER-AT-RISK DANBURY INDEPENDENT SCHOOL DISTRICT Project: Danbury I.S.D. Elementary School Issue Date: March 2, 2018 Submission Due Date: March 20, 2018 Table

REQUEST FOR QUALIFICATIONS FOR CONSTRUCTION MANAGER-AT-RISK DANBURY INDEPENDENT SCHOOL DISTRICT Project: Danbury I.S.D. Elementary School Issue Date: March 2, 2018 Submission Due Date: March 20, 2018 Table