Corporation for Public Broadcasting. Introduction to Financial Reporting

|

|

|

- Rodney Terry

- 6 years ago

- Views:

Transcription

1 Corporation for Public Broadcasting Introduction to Financial Reporting Live Webinar Training October 4, 2017

2 Introductions Webinar Presenters Kate Arno, Director, TV CSG Policy & Review Biniam Debebe, Senior Financial Review Specialist Ken Goulet, Senior Financial Review Specialist 2

3 Objectives By participating in this training, you will: Understand purpose and importance of accurate reporting Be ready to prepare your first Annual Financial Report (AFR) or Financial Summary Report (FSR) Improve ability to file a flawless report Know where to find help Meet annual training requirement 3

4 Agenda Overview of Financial Reporting to CPB Non-Federal Financial Support (NFFS) Preparing the Annual Financial Reports AFR Demonstration 4

5 Financial Reporting to CPB Webinar Series Intro to Financial Reporting What is NFFS? TV Grantees & Radio CSG Level C & D In-kind Contributions Radio CSG Level A & B AFR Schedules A, E & F FSR Indirect Administrative Support Institutional Licensees 5

6 CPB Office of Grants Administration cpb.org Greg Schnirring, VP, CSG and Station Initiatives Kate Arno, Director, TV CSG Policy and Review Andrew Charnik, Director, Radio CSG Policy and Administration Nadine M. Feaster, Director, Grants Administration Sharon Simmons, Manager, Grants Administration Biniam Debebe, Senior Financial Review Specialist Ken Goulet, Senior Financial Review Specialist Station information page: cpb.org/stations/ Online webinars: cpb.org/station-resource/csg-and-isis-training-opportunities Help Desk Phone: (866) Fax: (202) CSG Resources 6

7 Where to Find Resources Website cpb.org 7

8 Where to Find Resources Website cpb.org 8

9 Submitting Questions Press Q&A button in the top right of screen At bottom right, choose Q&A Under Ask, select Host Type question in field at bottom of screen Hit send 9

10 Agenda Overview of Financial Reporting to CPB Grantee compliance Important documents Annual filing requirements Non-Federal Financial Support (NFFS) Preparing the Annual Financial Reports AFR Demonstration 10

11 Grantee Compliance The Communications Act 1. Open and closed meeting 2. Open financial records 3. Community advisory boards 4. Equal employment opportunity (EEO) 5. Donor lists and political activities 11

12 Grantee Compliance General Provisions and Eligibility Criteria 1. Eligibility criteria 2. Recordkeeping 3. Operational requirements 4. Diversity and transparency requirements 5. Use of CSG funds and spending restrictions 6. Reporting requirements (AFR/FSR, SABS and SAS) 12

13 Important Documents CSG Agreement and Certification of Eligibility Signed by Head of Grantee and Licensee Official Explains requirements of the Communications Act 13

14 Important Documents Financial Reporting Guidelines Explains reporting requirements, defines NFFS, provides line item instructions Updated annually Principles of Accounting (May 2005) Provides guidance on CPB s requirement to submit audited financial statements, both under Financial Accounting Standards Board (FASB) and Governmental Accounting Standards Board (GASB) 14

15 Important Documents Discrete Accounting The Communications Act and CSG General Provisions require grantees practice discrete accounting of all CSG revenues and expenditures. Discrete Accounting Defined Discrete accounting requires unique accounting codes that identify CSG funds both revenues and expenses, restricted and unrestricted so that both the grantor and auditor can track CSG funds within the grant recipient s accounting system. 15

16 Important Documents CSG Non-compliance Policy: To increase grantees compliance and to address consequences for grantees non-compliance. 16

17 Legal Form Annual Filing Requirements CSG Agreement and Certification of Eligibility Form Surveys/Reports Station Activities Survey (SAS) (TV & Radio) Station Activities Benchmarking Survey (SABS) (TV) Local Content and Services Report (LCSR) (TV) Financial Forms AFR or FSR 17

18 FY 2018 CSG Cycle 2 nd payment made (30% of CSG) Submit FY 2016 AFR/FSR (5 mo. after FY end) FY 2018 grant offers made (Nov. 2017) FY 2017 AFR/FSR submitted Certify & accept CSG (by June 30, 2018) SABS/SAS/LCSR (by Feb. 15, 2018) 1 st payment made (70% of CSG) 18

19 AFR or FSR & AFS? All TV grantees are required to file AFR and submit AFS Radio grantees: CSG Level Total Revenue Financial Form Financial Statements Required A & B < $300,000 FSR Audited or Unaudited A & B $300,000 FSR Audited C & D N/A AFR Audited 19

20 Submitting Questions Press Q&A button in the top right of screen At bottom right, choose Q&A Under Ask, select Host Type question in field at bottom of screen Hit send 20

21 Agenda Overview of Financial Reporting to CPB Non-Federal Financial Support (NFFS) Definition of NFFS Purpose NFFS Criteria Preparing the Annual Financial Reports AFR Demonstration 21

22 What is NFFS? NFFS is the total of direct revenue and the fair value of property and services received as either a contribution or a payment, which meets specific criteria as to: recipient, form, source, and purpose. 22

23 Purpose of NFFS Determine Grantee s CSG program eligibility Factor in calculating incentive portion of CSG Part of the legal justification for CPB s federal appropriation 23

24 NFFS Criteria Summary NFFS Criteria Contribution Payment (including Exchange Transactions) Recipient Public broadcasting entity or an organization that receives the revenue on its behalf Form Gifts, grants, bequests, donations and appropriations An appropriation or contract payment Source Any source except the federal government or a public broadcasting entity State or local government or agency thereof; or an educational institution Purpose Construction or operation of a noncommercial, educational public broadcast station; or the production, acquisition, distribution, or dissemination of educational television or radio programs and related activities The cash, goods and/or services received by the CSG recipient must be in exchange for a service directly related to producing, developing, or delivering educational or instructional television or radio programming. 24

25 NFFS: The Source Criterion Contributions Ineligible Federal Government Public Broadcasting Entities Eligible State & Local Government Agencies Not for profits & Foundations For Profit Entities Individuals Public & Private Colleges & Universities 25

26 NFFS: The Source Criterion Payments Eligible Ineligible Federal Government Not for profits & foundations that are not educational institutions State & Local Government Agencies Educational Institutions For Profit Entities Individuals Public Broadcasting Entities 26

27 NFFS Criteria Summary NFFS Criteria Contribution Payment (including Exchange Transactions) Recipient Public broadcasting entity or an organization that receives the revenue on its behalf Form Gifts, grants, bequests, donations and appropriations An appropriation or contract payment Source Any source except the federal government or a public broadcasting entity State or local government or agency thereof; or an educational institution Purpose Construction or operation of a noncommercial, educational public broadcast station; or the production, acquisition, distribution, or dissemination of educational television or radio programs and related activities The cash, goods and/or services received by the CSG recipient must be in exchange for a service directly related to producing, developing, or delivering educational or instructional television or radio programming. 27

28 Questions & Answers Q & A Test Your Knowledge 28

29 Question 1 For FY2017, a radio station with CSG level A has total revenue of $500K and NFFS of $275K. What financial forms must the station submit to CPB? A. AFR and AFS since the station is CSG level A. B. FSR and AFS since total revenue is $300K. C. FSR and no AFS since NFFS is < $300K. D. FSR and unaudited financial statements since NFFS is <$300K. 29

30 AFR or FSR & AFS? All TV grantees are required to file AFR and submit AFS Radio grantees: CSG Level Total Revenue Financial Form Financial Statements Required A & B < $300,000 FSR Audited or Unaudited A & B $300,000 FSR Audited C & D N/A AFR Audited 30

31 Question 1 - Answer For FY2017, a radio station with CSG level A has total revenue of $500K and NFFS of $275K. What financial forms must the station submit to CPB? A. AFR and AFS since the station is CSG level A. B. FSR and AFS since total revenue is $300K. C. FSR and no AFS since NFFS is < $300K. D. FSR and unaudited financial statements since NFFS is <$300K. 31

32 Question 2 Which of the following statements are true? A. All revenues in a station s AFS qualify as NFFS. B. The four NFFS criteria are Recipient, Form, Source and Purpose. C. Revenue needs to meet only one NFFS criteria to be eligible as NFFS. D. CPB can add additional restrictions to NFFS. 32

33 Question 2 - Answer Which of the following statements are true? A. All revenues in a station s AFS qualify as NFFS. B. The four NFFS criteria are Recipient, Form, Source and Purpose. C. Revenue needs to meet only one NFFS criteria to be eligible as NFFS. D. CPB can add additional restrictions to NFFS. 33

34 Question 3 A TV station received grants from USDOE, a for-profit entity, a foundation, and a PBE for the production and distribution of educational television. Which statement is correct? A. All contributions for the purpose of production and distribution of educational television are NFFS eligible. B. Contributions from the USDOE and other public broadcasting entity are NFFS eligible. C. Contributions from the foundation and for-profit entity are NFFS eligible. 34

35 Question 3 - Answer A TV station received grants from USDOE, a for-profit entity, a foundation, and a PBE for the production and distribution of educational television. Which statement is correct? A. All contributions for the purpose of production and distribution of educational television are NFFS eligible. B. Contributions from the USDOE and other public broadcasting entity are NFFS eligible. C. Contributions from the foundation and for-profit entity are NFFS eligible. 35

36 Question 4 A Radio station received payments for rental of excess tower capacity to the local government and to a private business. Which statement is correct? A. Payment from the local government is NFFS eligible and private business is NFFS ineligible. B. Payments from both sources are NFFS eligible. C. Payments from both sources are NFFS ineligible. 36

37 Question 4 - Answer A Radio station received payments for rental of excess tower capacity to the local government and to a private business. Which statement is correct? A. Payment from the local government is NFFS eligible and private business is NFFS ineligible. B. Payments from both sources are NFFS eligible. C. Payments from both sources are NFFS ineligible. 37

38 Submitting Questions Press Q&A button in the top right of screen At bottom right, choose Q&A Under Ask, select Host Type question in field at bottom of screen Hit send 38

39 Agenda Overview of Financial Reporting to CPB Non-Federal Financial Support (NFFS) Preparing the Annual Financial Reports AFR/FSR Filing Process AFR Form/Schedules Audited Financial Statement Requirements AFR Demonstration 39

40 AFR/FSR Filing Process General ledger and accounting records maintained throughout the fiscal year... 40

41 AFR/FSR Financial Schedules AFR FSR Direct Revenue Schedule A Part 1 Indirect Administrative Support (if applicable) In-kind Contributions (if applicable) Schedule B Part 1 Schedules C and D Part 1 Expenses Schedule E Part 2 NFFS Exclusions Schedules A, B, C and D Part 3 Reconciliation with Audited Financial Statements (if applicable) Schedule F Part 4 41

42 Required forms for all grantees Schedule A: Direct Revenue Schedule E: Expenses Schedule F: Reconciliation Grantee Profile Signature Page Audited Financial Statements Required forms, if they apply to your station Schedule B: Indirect Administrative Support Schedule C: In-kind Contributions of Services & Other Assets Schedule D: In-kind Contributions of Property & Equipment Large Gift Spread (TV) or Capital Spread (Radio) Accountant s Qualification Statement (AQS) (State/Internal Audit) Extension Request Form AFR Form 42

43 Audited Financial Statements/AFS Must be station specific Must be comparative statements (include prior year) Must be on letterhead, signed & uploaded by the Independent Auditor. Joint Licensees file separate AFRs/FSRs for each distinct CSG grantee but can use a combined AFS. 43

44 Audited Financial Statements Financial Accounting Standards Board (FASB) model financial statements include: Independent Auditor s Report Statement of Financial Position Statement of Activities Statement of Cash Flows Notes to Financial Statements Statement of Functional Expenses (optional but strongly encouraged) 44

45 Audited Financial Statements Governmental Accounting Standards Board (GASB) model financial statements generally include: Independent Auditor s Report Management s Discussion and Analysis (MD&A) Statement of Net Assets (and/or Balance Sheet) Statement of Revenues, Expenses and Changes in (Fund) Net Assets Statement of Cash Flows Notes to Financial Statements Statement of Functional Expenses (optional but strongly encouraged) 45

46 Unaudited Financial Statements Unaudited Financial Statements for FASB model: Required: Statement of Financial Position Statement of Activities Statement of Cash Flows Optional for CPB: Notes to Financial Statements Statement of Functional Expenses Note: Financial statements must be comparative. 46

47 Unaudited Financial Statements Unaudited Financial Statements for GASB model: Required Statement of Net Assets (and/or Balance Sheet) Statement of Revenues, Expenses and Changes in (Fund) Net Assets Statement of Cash Flows Optional for CPB Notes to Financial Statements Statement of Functional Expenses Management s Discussion and Analysis (MD&A) Note: Financial statements must be comparative. 47

48 AFR/FSR Filing Deadlines The AFR or FSR is due 5 months after the end of your fiscal year and penalties apply for late filing. CSG Grantee s Fiscal year-end AFR/FSR due by 6/30/17 11/30/17 9/30/17 2/28/18 12/31/17 5/31/18 Two extensions are available: 1 st extension is for 45 days 2 nd extension is for 30 days 48

49 Requesting Changes to AFRs/FSRs Submit requests by May 15 of voluntary changes to your AFR/FSR or AFS. Changes affecting NFFS must be recertified and re-attested before resubmitting to CPB. 49

50 AFR/FSR Desk Review Process After you submit your AFR/FSR: CPB performs desk reviews Stations will be contacted during desk reviews AFRs/FSRs are subject to audit by the Inspector General (even after desk review approvals) 50

51 AFR Submission Summary Complete all required & applicable schedules Verify revenues, expenses, and NFFS Complete signature page (by Head of Grantee & Independent Accountant) Submit the AFR/FSR to CPB CPB performs desk reviews & requests information/documentation Once approved, NFFS is used in CSG calculations 51

52 Questions & Answers Q & A Test Your Knowledge 52

53 Question 5 Which of the following is correct regarding AFR/FSR filing? A. The AFR/FSR is due by May 31 st B. Penalties do not apply C. A maximum of 3 filing extensions are available D. 1 st extension requires justification & approval by CPB E. 2 nd extension requires justification & approval by CPB 53

54 Question 5 - Answer Answer (E): The 2nd extension requires a justification and approval by CPB - The AFR is due 5 months after the grantee s FY end. - Penalties do apply for late filing - Only 2 AFR/FSR extensions are available, - 1 st extension requires only requesting it 54

55 Question 6 Which of the following is not correct? A. An AFR/FSR is subject to an audit by CPB s OIG, even after desk review approvals. B. Both the Head of Grantee & Independent Accountant must sign the AFR. C. AFR Schedules A, E, & F are always required to be completed. D. None of the above 55

56 Question 6 - Answer Answer (D): None of the above. - Choices A to C are all correct. A. An AFR/FSR is subject to an audit by CPB s OIG, even after desk review approvals. B. Both the Head of Grantee & Independent Accountant must sign the AFR. C. AFR Schedules A, E, & F are always required to be completed. 56

57 Submitting Questions Press Q&A button in the top right of screen At bottom right, choose Q&A Under Ask, select Host Type question in field at bottom of screen Hit send 57

58 Agenda Overview of Financial Reporting to CPB Non-Federal Financial Support (NFFS) Preparing the Annual Financial Reports AFR Demonstration 58

59 Integrated Station Information System Access at isis.cpb.org 59

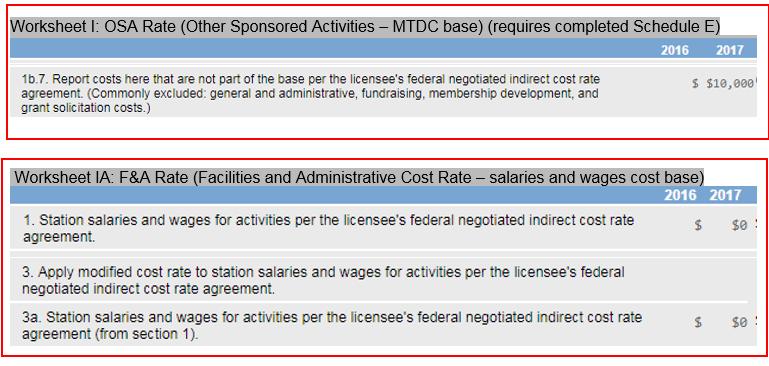

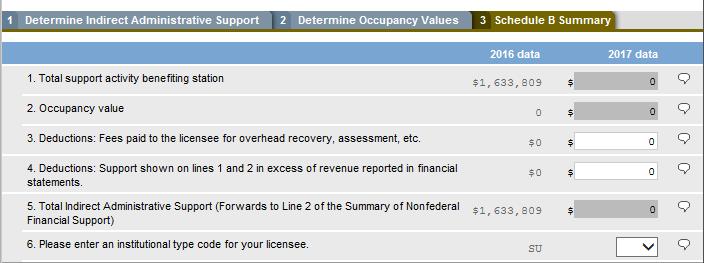

60 Financial Reporting Main View status of schedules and forms Submit to CPB Menu NFFS Summary 60

61 Report direct revenue Schedule A Identify NFFS on each line Add comments for large differences 61

62 Report direct revenue Schedule A Line 13 & 14 Revenue (Net of Direct Expenses) Indicate NFFS eligibility on Line 20 New (Line 21) Spectrum Auction 62

63 Schedule A Adjustments to Revenue (Automatically populated in ISIS) Revised description New Line Item 63

64 Schedule E Report program and support services expenses Report investment in capital assets Indicate direct and indirect expenses 64

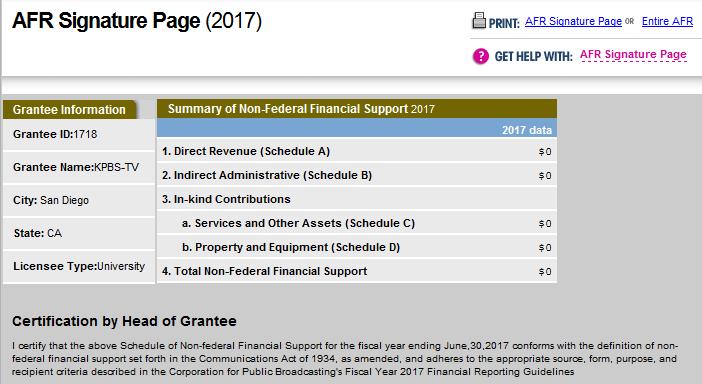

Radio TV")

65 Schedule E Report expenses by function & source in Lines 1 to 7 (A-D) Radio TV 65

66 Schedule F Input all revenue reported in your audited financial statements in line 2 and add reconciling items in Line 4 66

67 Schedule B Indirect administrative support-ias Revised description 67

68 Indirect administrative support Schedule B 68

69 Schedule C In-kind contributions of services and other assets 69

70 Schedule D In-kind contributions of property and equipment 70

71 AFS Upload Page The independent accountant must complete this page and upload the audited financial statements 71

72 Signature Page Head of Grantee certifies NFFS Independent Accountant attests to NFFS 72

73 Submitting Questions Press Q&A button in the top right of screen At bottom right, choose Q&A Under Ask, select Host Type question in field at bottom of screen Hit send 73

74 Completed Agenda Overview of Financial Reporting to CPB Non-Federal Financial Support (NFFS) Preparing the Annual Financial Reports AFR Demonstration 74

75 Completed Objectives By participating in this training, you will: Understand purpose and importance of accurate reporting Be ready to prepare your first Annual Financial Report (AFR) or Financial Summary Report (FSR) Improve ability to file flawless report Know where to find help Meet annual training requirement 75

76 CPB Office of Grants Administration cpb.org Greg Schnirring, VP, CSG and Station Initiatives Kate Arno, Director, TV CSG Policy and Review Andrew Charnik, Director, Radio CSG Policy and Administration Nadine M. Feaster, Director, Grants Administration Sharon Simmons, Manager, Grants Administration Biniam Debebe, Senior Financial Review Specialist Ken Goulet, Senior Financial Review Specialist Station information page: cpb.org/stations/ Online webinars: cpb.org/station-resource/csg-and-isis-training-opportunities Help Desk Phone: (866) Fax: (202) CSG Resources 76

77 Where to Find Resources Website cpb.org 77

78 Where to Find Resources Website cpb.org 78

79 Corporation for Public Broadcasting Introduction to Financial Reporting Live Webinar Training October 4, 2017

Corporation for Public Broadcasting

Corporation for Public Broadcasting What is NFFS? Live Webinar Training October 11, 2017 Introductions Webinar Presenters Kate Arno, Director, TV CSG Policy & Review Biniam Debebe, Senior Financial Reviews

Corporation for Public Broadcasting What is NFFS? Live Webinar Training October 11, 2017 Introductions Webinar Presenters Kate Arno, Director, TV CSG Policy & Review Biniam Debebe, Senior Financial Reviews

Financial Reporting Main

CPB ISIS Grantee's Main Finance Screen https://isis.cpb.org/headerclick.aspx?rdct=financialmain 1 of 1 4/12/2017 3:16 PM BRUCE HAINES Financial Reporting Legal Forms Grant Payments Grantee Profile Current

CPB ISIS Grantee's Main Finance Screen https://isis.cpb.org/headerclick.aspx?rdct=financialmain 1 of 1 4/12/2017 3:16 PM BRUCE HAINES Financial Reporting Legal Forms Grant Payments Grantee Profile Current

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE AND OTHER SELECTED GRANTS AT KENTUCKY AUTHORITY FOR EDUCATIONAL TELEVISION, INC., KET-TV, LEXINGTON, KENTUCKY

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE AND OTHER SELECTED GRANTS AT KENTUCKY AUTHORITY FOR EDUCATIONAL TELEVISION, INC., KET-TV, LEXINGTON, KENTUCKY

Source of Income 2015 data 2016 data

Page 1 of 11 Schedule A NFFS Excluded? If you have an NFFS Exclusion, please click the "NFFS X" button, and enter your NFFS data. Source of Income 2015 data 1. Amounts provided directly by federal government

Page 1 of 11 Schedule A NFFS Excluded? If you have an NFFS Exclusion, please click the "NFFS X" button, and enter your NFFS data. Source of Income 2015 data 1. Amounts provided directly by federal government

https://isis.cpb.org/printpage.aspx?printpage=schall

Page 1 of 11 Schedule A NFFS Excluded? If you have an NFFS Exclusion, please click the "NFFS X" button, and enter your NFFS data. Source of Income 2015 data 1. s provided directly by federal government

Page 1 of 11 Schedule A NFFS Excluded? If you have an NFFS Exclusion, please click the "NFFS X" button, and enter your NFFS data. Source of Income 2015 data 1. s provided directly by federal government

BACKGROUND. CPB Community Service Grant

This report presents the conclusions of the OIG. The findings and recommendations presented in this report do not necessarily represent CPB s final position on these matters. CPB officials will make a

This report presents the conclusions of the OIG. The findings and recommendations presented in this report do not necessarily represent CPB s final position on these matters. CPB officials will make a

Source of Income 2015 data 2016 data Revision

Page 1 of 15 Schedule A NFFS Excluded? If you have an NFFS Exclusion, please click the "NFFS X" button, and enter your NFFS data. Source of Income 2015 data 2016 data Revision 1. Amounts provided directly

Page 1 of 15 Schedule A NFFS Excluded? If you have an NFFS Exclusion, please click the "NFFS X" button, and enter your NFFS data. Source of Income 2015 data 2016 data Revision 1. Amounts provided directly

Community Service Grant 101. Kate Arno, Director, TV CSG Policy and Review Deborah Carr, Director, CSG Radio Administration

Community Service Grant 101 Kate Arno, Director, TV CSG Policy and Review Deborah Carr, Director, CSG Radio Administration 1 Almost 600 CSG radio and TV grantees More than 1300 stations Photos courtesy

Community Service Grant 101 Kate Arno, Director, TV CSG Policy and Review Deborah Carr, Director, CSG Radio Administration 1 Almost 600 CSG radio and TV grantees More than 1300 stations Photos courtesy

FY 2017 Radio Station Collaboration Program

FY 2017 Radio Station Collaboration Program The Radio Station Collaboration Program (SCP) is designed to support Community Service Grant (CSG) recipients that have entered into collaborative or consolidation

FY 2017 Radio Station Collaboration Program The Radio Station Collaboration Program (SCP) is designed to support Community Service Grant (CSG) recipients that have entered into collaborative or consolidation

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE AND OTHER SELECTED GRANTS AT ROCKY MOUNTAIN PUBLIC BROADCASTING NETWORK, INC., KRMA-TV/KUVO-FM, DENVER, COLORADO

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE AND OTHER SELECTED GRANTS AT ROCKY MOUNTAIN PUBLIC BROADCASTING NETWORK, INC., KRMA-TV/KUVO-FM, DENVER, COLORADO

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE GRANTS AWARDED TO UNC-TV, PUBLIC MEDIA NORTH CAROLINA, RESEARCH TRIANGLE PARK, NORTH CAROLINA FOR THE PERIOD JULY

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE GRANTS AWARDED TO UNC-TV, PUBLIC MEDIA NORTH CAROLINA, RESEARCH TRIANGLE PARK, NORTH CAROLINA FOR THE PERIOD JULY

CORPORATION FOR PUBLIC BROADCASTING

CORPORATION FOR PUBLIC BROADCASTING SEMIANNUAL REPORT OFFICE OF INSPECTOR GENERAL OPERATIONS CPB AUDIT RESOLUTION ACTIVITIES October 1, 2012 to March 31, 2013 FOREWORD Congress created the (CPB) in 1967

CORPORATION FOR PUBLIC BROADCASTING SEMIANNUAL REPORT OFFICE OF INSPECTOR GENERAL OPERATIONS CPB AUDIT RESOLUTION ACTIVITIES October 1, 2012 to March 31, 2013 FOREWORD Congress created the (CPB) in 1967

Spectrum Auction Planning Grant GUIDELINES

Spectrum Auction Planning Grant GUIDELINES APPLICATION DEADLINE: January 31, 2015 OVERVIEW The Corporation for Public Broadcasting ( CPB ) will make matching grants of up to $50,000 to eligible public

Spectrum Auction Planning Grant GUIDELINES APPLICATION DEADLINE: January 31, 2015 OVERVIEW The Corporation for Public Broadcasting ( CPB ) will make matching grants of up to $50,000 to eligible public

2018 Television Community Service Grants General Provisions and Eligibility Criteria October 2017

2018 Television Community Service Grants General Provisions and Eligibility Criteria October 2017 Questions should be submitted to csg@cpb.org (Include station s call letters and four-digit Grantee ID)

2018 Television Community Service Grants General Provisions and Eligibility Criteria October 2017 Questions should be submitted to csg@cpb.org (Include station s call letters and four-digit Grantee ID)

SEMIANNUAL REPORT. OFFICE OF INSPECTOR GENERAL OPERATIONS and CPB AUDIT RESOLUTION ACTIVITIES

SEMIANNUAL REPORT OFFICE OF INSPECTOR GENERAL OPERATIONS and CPB AUDIT RESOLUTION ACTIVITIES April 1, 2013 September 30, 2013 Index of IG Act Reporting Requirements IG Act Reference OIG Reporting Requirements

SEMIANNUAL REPORT OFFICE OF INSPECTOR GENERAL OPERATIONS and CPB AUDIT RESOLUTION ACTIVITIES April 1, 2013 September 30, 2013 Index of IG Act Reporting Requirements IG Act Reference OIG Reporting Requirements

CATEGORICAL PROGRAMS

CATEGORICAL PROGRAMS Categorical programs include grants, entitlements and other financial assistance received by a school district from governmental or other entities. These programs are designed to fund

CATEGORICAL PROGRAMS Categorical programs include grants, entitlements and other financial assistance received by a school district from governmental or other entities. These programs are designed to fund

CHARLES STEWART MOTT FOUNDATION AFFIDAVIT UPDATE PACKET FOR NON-U.S. GRANTEES

CHARLES STEWART MOTT FOUNDATION AFFIDAVIT UPDATE PACKET FOR NON-U.S. GRANTEES This packet includes: INTRODUCTION and INSTRUCTIONS "AFFIDAVIT UPDATE" "PUBLIC SUPPORT SCHEDULE" "MAJOR DONOR SUPPORT" FORM

CHARLES STEWART MOTT FOUNDATION AFFIDAVIT UPDATE PACKET FOR NON-U.S. GRANTEES This packet includes: INTRODUCTION and INSTRUCTIONS "AFFIDAVIT UPDATE" "PUBLIC SUPPORT SCHEDULE" "MAJOR DONOR SUPPORT" FORM

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS. National Historical Publications and Records Commission

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission March 5, 2012 Contents USE OF THE GUIDE... 2 ACCOUNTABILITY REQUIREMENTS... 2 Financial

CATEGORICAL PROGRAMS

CATEGORICAL PROGRAMS Categorical programs include grants, entitlements and other financial assistance received by a school district from governmental or other entities. These programs are designed to fund

CATEGORICAL PROGRAMS Categorical programs include grants, entitlements and other financial assistance received by a school district from governmental or other entities. These programs are designed to fund

Frequently Asked Questions

Frequently Asked Questions August 2016 CATEGORY Allowable Expenses 1. Is Texas sales tax a reimbursable expense? No, sales tax is not a reimbursable expense. Budget 2. Is there a preferred order to submit

Frequently Asked Questions August 2016 CATEGORY Allowable Expenses 1. Is Texas sales tax a reimbursable expense? No, sales tax is not a reimbursable expense. Budget 2. Is there a preferred order to submit

Quincy Riley Assessment Manager, HUD-REAC. Brian Edwards Auditor/Financial Analyst, HUD-REAC

19th Annual Public Housing Authority (PHA) Conference June 21 - June 22 Quincy Riley Assessment Manager, HUD-REAC Brian Edwards Auditor/Financial Analyst, HUD-REAC 1 Today s Topics 1. Submission Due Dates

19th Annual Public Housing Authority (PHA) Conference June 21 - June 22 Quincy Riley Assessment Manager, HUD-REAC Brian Edwards Auditor/Financial Analyst, HUD-REAC 1 Today s Topics 1. Submission Due Dates

American Friends of Canadian Land Trusts. American Friends of Canadian Land Trusts. Grantee Application 1

American Friends of Canadian Land Trusts Grantee Application Grantee Application 1 APPLICATION CHECKLIST Thank you for your interest in becoming a grantee with the American Friends of Canadian Land Trusts

American Friends of Canadian Land Trusts Grantee Application Grantee Application 1 APPLICATION CHECKLIST Thank you for your interest in becoming a grantee with the American Friends of Canadian Land Trusts

Understanding Audits and Common Audit Findings. Draft Manageme nt Decision

Understanding Audits and Common Audit Findings CNCS and OIG Oversight Activities The OIG conducts four to six audits of commissions and or subgrantees each year CNCS program and/or grants staff conduct

Understanding Audits and Common Audit Findings CNCS and OIG Oversight Activities The OIG conducts four to six audits of commissions and or subgrantees each year CNCS program and/or grants staff conduct

Solicitation for the 2016 Principal Campaign Fund Organization (PCFO)

") Solicitation for PCFO Norcal CFC Solicitation for the Principal Campaign Fund Organization (PCFO) Thank you for your interest in the PCFO selection process. The Office of Personnel Management (OPM) has

Solicitation for PCFO Norcal CFC Solicitation for the Principal Campaign Fund Organization (PCFO) Thank you for your interest in the PCFO selection process. The Office of Personnel Management (OPM) has

AGRICULTURAL MARKETING AND DEVELOPMENT DIVISION MDA Grants Line: AGRI MINNESOTA FARM TO EARLY CARE AND EDUCATION GRANT PROGRAM

MDA Grants Line: 651-201-6500 2019 REQUESTS FOR PROPOSALS Contents Background......................... 2 Program Goals....................... 2 Eligible Applicants and Required Letters of Support... 2

MDA Grants Line: 651-201-6500 2019 REQUESTS FOR PROPOSALS Contents Background......................... 2 Program Goals....................... 2 Eligible Applicants and Required Letters of Support... 2

HUMBOLDT STATE UNIVERSITY SPONSORED PROGRAMS FOUNDATION

HUMBOLDT STATE UNIVERSITY SPONSORED PROGRAMS FOUNDATION BASIC FINANCIAL STATEMENTS, SUPPLEMENTARY INFORMATION, AND SINGLE AUDIT REPORTS Including Schedules Prepared for Inclusion in the Financial Statements

HUMBOLDT STATE UNIVERSITY SPONSORED PROGRAMS FOUNDATION BASIC FINANCIAL STATEMENTS, SUPPLEMENTARY INFORMATION, AND SINGLE AUDIT REPORTS Including Schedules Prepared for Inclusion in the Financial Statements

Operational Support Program Final Report Instructions

Operational Support Program Final Report Instructions The Operational Support Grant Agreement with MCACA requires the final reporting of grant activities. Review these instructions carefully regarding

Operational Support Program Final Report Instructions The Operational Support Grant Agreement with MCACA requires the final reporting of grant activities. Review these instructions carefully regarding

United Way Funding Application Guidelines

United Way Funding Application Guidelines 2016-2017 Submission Deadline: Friday, April 1,2016 Our Mission To build a better community by organizing the capacity of people to care for one another. Guiding

United Way Funding Application Guidelines 2016-2017 Submission Deadline: Friday, April 1,2016 Our Mission To build a better community by organizing the capacity of people to care for one another. Guiding

MISSISSIPPI SMALL MUNICIPALITIES AND LIMITED POPULATION COUNTIES GRANT PROGRAM

MISSISSIPPI SMALL MUNICIPALITIES AND LIMITED POPULATION COUNTIES GRANT PROGRAM 2018 APPLICATION GUIDELINES & IMPLEMENTATION MANUAL Table of Contents SMALL MUNICIPALITIES AND LIMITED POPULATION COUNTIES

MISSISSIPPI SMALL MUNICIPALITIES AND LIMITED POPULATION COUNTIES GRANT PROGRAM 2018 APPLICATION GUIDELINES & IMPLEMENTATION MANUAL Table of Contents SMALL MUNICIPALITIES AND LIMITED POPULATION COUNTIES

AGRICULTURAL MARKETING AND DEVELOPMENT DIVISION MDA Grants Line:

Contents Background........................ 2 Program Goals...................... 2 Eligible Applicants and Required Letters of Support. 2 Eligible Projects..................... 2 Cash Match and Ineligible

Contents Background........................ 2 Program Goals...................... 2 Eligible Applicants and Required Letters of Support. 2 Eligible Projects..................... 2 Cash Match and Ineligible

Welcome and Introductions

Fiscal Matters: An Overview of Annual Head Start and Early Head Start Grant Requirements U.S. Department of Health and Human Services, Welcome and Introductions Staff Grantee Representatives 1 Goals for

Fiscal Matters: An Overview of Annual Head Start and Early Head Start Grant Requirements U.S. Department of Health and Human Services, Welcome and Introductions Staff Grantee Representatives 1 Goals for

RACE TO THE TOP EARLY LEARNING CHALLENGE

APRIL 2015 84.412 RACE TO THE TOP EARLY LEARNING CHALLENGE State Project/Program: Federal Authorization: State Authorization: RACE TO THE TOP EARLY LEARNING CHALLENGE U. S. DEPARTMENT OF EDUCATION PL 111-5

APRIL 2015 84.412 RACE TO THE TOP EARLY LEARNING CHALLENGE State Project/Program: Federal Authorization: State Authorization: RACE TO THE TOP EARLY LEARNING CHALLENGE U. S. DEPARTMENT OF EDUCATION PL 111-5

City of St. Petersburg Arts and Culture Grant Program Guidelines General Support Grant

City of St. Petersburg Arts and Culture Grant Program Guidelines 2017-2018 General Support Grant St. Petersburg Arts Advisory Committee Staff Wayne David Atherholt, Director, Mayor s Office of Cultural

City of St. Petersburg Arts and Culture Grant Program Guidelines 2017-2018 General Support Grant St. Petersburg Arts Advisory Committee Staff Wayne David Atherholt, Director, Mayor s Office of Cultural

Cancer Prevention & Research Institute of Texas

Cancer Prevention & Research Institute of Texas IA # 01-18 Internal Audit Report over Post-Award C O N T E N T S Page Internal Audit Report Transmittal Letter to the Oversight Committee... 1 Background...

Cancer Prevention & Research Institute of Texas IA # 01-18 Internal Audit Report over Post-Award C O N T E N T S Page Internal Audit Report Transmittal Letter to the Oversight Committee... 1 Background...

Commonwealth Health Research Board ("CHRB") Grant Guidelines for FY 2014/2015

Grant Guidelines for FY 2014/2015") ("CHRB") Grant Guidelines for FY 2014/2015 Effective July 1, 2013 for grants to be awarded July 1, 2014 KEY DATES DUE DATES Concept Paper Submissions October 1, 2013 Full Proposal Submissions February

("CHRB") Grant Guidelines for FY 2014/2015 Effective July 1, 2013 for grants to be awarded July 1, 2014 KEY DATES DUE DATES Concept Paper Submissions October 1, 2013 Full Proposal Submissions February

Henry County Community Foundation How to Access the Online Grant Application

Henry County Community Foundation How to Access the Online Grant Application 1. Follow the link from the Foundation s website to https://henrycountycfgrants.communityforce.com/ You will be taken to HCCF

Henry County Community Foundation How to Access the Online Grant Application 1. Follow the link from the Foundation s website to https://henrycountycfgrants.communityforce.com/ You will be taken to HCCF

Being a CPRIT Grantee: What You Need To Know

Being a CPRIT Grantee: What You Need To Know FY2016 Welcome & Introductions Cameron Eckel Staff Attorney 512-305-8495 ceckel@cprit.texas.gov Lisa Nelson Operations Manager 512-305-8418 lnelson@cprit.texas.gov

Being a CPRIT Grantee: What You Need To Know FY2016 Welcome & Introductions Cameron Eckel Staff Attorney 512-305-8495 ceckel@cprit.texas.gov Lisa Nelson Operations Manager 512-305-8418 lnelson@cprit.texas.gov

REQUEST FOR PROPOSALS FOR FEE ACCOUNTING SERVICES ALL PROPOSALS MUST BE ADDRESSED AND SUBMITTED TO:

REQUEST FOR PROPOSALS FOR FEE ACCOUNTING SERVICES ALL PROPOSALS MUST BE ADDRESSED AND SUBMITTED TO: ROBERT DICKE, EXECUTIVE DIRECTOR 2001 W. BROADWAY, SUITE 1 MONONA, WI 53713-3707 PROPOSALS MUST BE RECEIVED

REQUEST FOR PROPOSALS FOR FEE ACCOUNTING SERVICES ALL PROPOSALS MUST BE ADDRESSED AND SUBMITTED TO: ROBERT DICKE, EXECUTIVE DIRECTOR 2001 W. BROADWAY, SUITE 1 MONONA, WI 53713-3707 PROPOSALS MUST BE RECEIVED

NEW LEADERS FINAL REPORT INSTRUCTIONS

NEW LEADERS FINAL REPORT INSTRUCTIONS The New Leaders Grant Agreement with MCACA requires the final reporting of grant activities. Review the instructions below carefully regarding the specific grant reporting

NEW LEADERS FINAL REPORT INSTRUCTIONS The New Leaders Grant Agreement with MCACA requires the final reporting of grant activities. Review the instructions below carefully regarding the specific grant reporting

Canada Cultural Investment Fund (CCIF)

") Canada Cultural Investment Fund (CCIF) Endowment Incentives Component Guidelines Endowment Incentives 1 This publication is available in PDF format on the Internet at http://www.pch.gc.ca/eng/1268614803109#a5

Canada Cultural Investment Fund (CCIF) Endowment Incentives Component Guidelines Endowment Incentives 1 This publication is available in PDF format on the Internet at http://www.pch.gc.ca/eng/1268614803109#a5

FY2017 SNAP PROCESS AND TECHNOLOGY IMPROVEMENT GRANTS (PTIG)

") FY2017 SNAP PROCESS AND TECHNOLOGY IMPROVEMENT GRANTS (PTIG) MAY 9, 2017, 3:00PM EST CALL-IN: 888.844.9904 ACCESS CODE: 5094077 THIS WEBINAR IS BEING RECORDED Presented by Christina Palazzolo, SNAP Program

FY2017 SNAP PROCESS AND TECHNOLOGY IMPROVEMENT GRANTS (PTIG) MAY 9, 2017, 3:00PM EST CALL-IN: 888.844.9904 ACCESS CODE: 5094077 THIS WEBINAR IS BEING RECORDED Presented by Christina Palazzolo, SNAP Program

UNC Account Request System

ACCOUNTING SERVICES UNC Account Request System Purpose: The UNC Account Request System is designed to request new accounts for the University and it s Associated Entities (Foundations). Please refer to

ACCOUNTING SERVICES UNC Account Request System Purpose: The UNC Account Request System is designed to request new accounts for the University and it s Associated Entities (Foundations). Please refer to

Culture Projects Grant Program

2019 Guidelines Culture Projects Grant Program Grant applications are due Friday, October 12, 2018 by 4:30 PM Due Date: Friday, October 12, 1, 2018 by 4:30pm Table of Contents Program Purpose..........

2019 Guidelines Culture Projects Grant Program Grant applications are due Friday, October 12, 2018 by 4:30 PM Due Date: Friday, October 12, 1, 2018 by 4:30pm Table of Contents Program Purpose..........

FINAL AUDIT REPORT DEPARTMENT OF COMMUNITY AFFAIRS WEATHERIZATION ASSISTANCE PROGRAM ARRA IMPLEMENTATION FEBRUARY 14, 2009 THROUGH JANUARY 31, 2010

FINAL AUDIT REPORT DEPARTMENT OF COMMUNITY AFFAIRS WEATHERIZATION ASSISTANCE PROGRAM ARRA IMPLEMENTATION FEBRUARY 14, 2009 THROUGH JANUARY 31, 2010 ACN 10-A403 Cassi Beebe, CGAP Audit Evaluation and Review

FINAL AUDIT REPORT DEPARTMENT OF COMMUNITY AFFAIRS WEATHERIZATION ASSISTANCE PROGRAM ARRA IMPLEMENTATION FEBRUARY 14, 2009 THROUGH JANUARY 31, 2010 ACN 10-A403 Cassi Beebe, CGAP Audit Evaluation and Review

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT)

") GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

GRANTS AND CONTRACTS (FINANCIAL GRANTS MANAGEMENT) Policies & Procedures UPDATED: February 25, 2015 (04/21/16) 2 TABLE OF CONTENTS Definitions... 3-7 DRFR 8.00 Policy Statement... 8 DRFR 8.02 Employee

The Vision: Norfolk is the cultural capital of Virginia and offers the highest quality and the widest array of artistic experiences.

Commission on the Arts and Humanities Department of Cultural Facilities, Arts and Entertainment City of Norfolk, Virginia Slover Library Room LL40, 235 East Plume Street, Norfolk, VA 23510 (Directions

Commission on the Arts and Humanities Department of Cultural Facilities, Arts and Entertainment City of Norfolk, Virginia Slover Library Room LL40, 235 East Plume Street, Norfolk, VA 23510 (Directions

N O N-PR O FI T O R G A NI Z A T I O NS

FIN A N C I A L M A N A G E M E N T G UID E F O R N O N-PR O FI T O R G A NI Z A T I O NS N A T I O N A L E ND O W M E N T F O R T H E A R TS O F F I C E O F INSP E C T O R G E N E R A L SEP T E M B E

FIN A N C I A L M A N A G E M E N T G UID E F O R N O N-PR O FI T O R G A NI Z A T I O NS N A T I O N A L E ND O W M E N T F O R T H E A R TS O F F I C E O F INSP E C T O R G E N E R A L SEP T E M B E

Sponsored Programs Roles & Responsibilities

The University of Florida is committed to acting with integrity in the management of sponsored programs. The goals of this document are to provide descriptions of key individuals or units and their responsibilities

The University of Florida is committed to acting with integrity in the management of sponsored programs. The goals of this document are to provide descriptions of key individuals or units and their responsibilities

Grant Guidelines. for Cultural Facilities. Table of Contents. Florida Department of State

Florida Department of State DiVisiOn Of Cultural Affairs Grant Guidelines for 2018-2019 Cultural Facilities Florida Department of State, Division of Cultural Affairs Florida Council on Arts and Culture

Florida Department of State DiVisiOn Of Cultural Affairs Grant Guidelines for 2018-2019 Cultural Facilities Florida Department of State, Division of Cultural Affairs Florida Council on Arts and Culture

Trinity Valley Community College. Grants Accounting Policy and Procedures 2012

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

Trinity Valley Community College Grants Accounting Policy and Procedures 2012 TABLE OF CONTENTS I. Overview.....3 II. Project Startup.... 3 III. Contractual Services.......3 IV. Program Income.....4 V.

REQUEST FOR QUOTES FOR CERTIFIED PUBLIC ACCOUNTANT SERVICES

REQUEST FOR QUOTES FOR CERTIFIED PUBLIC ACCOUNTANT SERVICES for the DUTCHESS COUNTY RESOURCE RECOVERY AGENCY POUGHKEEPSIE, NEW YORK DECEMBER 2017 Deadline for the Submission of Proposals JANUARY 17 at

REQUEST FOR QUOTES FOR CERTIFIED PUBLIC ACCOUNTANT SERVICES for the DUTCHESS COUNTY RESOURCE RECOVERY AGENCY POUGHKEEPSIE, NEW YORK DECEMBER 2017 Deadline for the Submission of Proposals JANUARY 17 at

Sponsored Programs Roles & Responsibilities

The University of Florida is committed to acting with integrity in the management of sponsored programs. The goals of this document are to provide descriptions of key individuals or units and their responsibilities

The University of Florida is committed to acting with integrity in the management of sponsored programs. The goals of this document are to provide descriptions of key individuals or units and their responsibilities

HENDERSHOT, BURKHARDT & ASSOCIATES CERTIFIED PUBLIC ACCOUNTANTS

Young Marines of the Marine Corps League Financial Statements for the Year Ended September 30, 2016 and Independent Auditors Report Dated March 8, 2017 HENDERSHOT, BURKHARDT & ASSOCIATES CERTIFIED PUBLIC

Young Marines of the Marine Corps League Financial Statements for the Year Ended September 30, 2016 and Independent Auditors Report Dated March 8, 2017 HENDERSHOT, BURKHARDT & ASSOCIATES CERTIFIED PUBLIC

Chapter 4. Disbursements

Chapter 4 Disbursements This Page Left Blank Intentionally CTAS User Manual 4-1 Disbursements: Introduction The Claims Module in CTAS allows you to post approved claims into disbursements. If you use a

Chapter 4 Disbursements This Page Left Blank Intentionally CTAS User Manual 4-1 Disbursements: Introduction The Claims Module in CTAS allows you to post approved claims into disbursements. If you use a

2017 Operating Assistance Grants Guide

New Mexico Coalition for Literacy 2017 Operating Assistance Grants Guide BACKGROUND AND GRANT OVERVIEW The New Mexico Coalition for Literacy (NMCL) is a private, nonprofit New Mexico corporation missioned

New Mexico Coalition for Literacy 2017 Operating Assistance Grants Guide BACKGROUND AND GRANT OVERVIEW The New Mexico Coalition for Literacy (NMCL) is a private, nonprofit New Mexico corporation missioned

Accounting for Cost Share Commitments

IV. Accounting for Cost Share Commitments A. Overview Cost share commitments are contributions made by RIT or a third party to support the overall costs of a sponsored project. The cost share commitments

IV. Accounting for Cost Share Commitments A. Overview Cost share commitments are contributions made by RIT or a third party to support the overall costs of a sponsored project. The cost share commitments

Comprehensive Continuous Improvement Plan Allocation Process

Comprehensive Continuous Improvement Plan Allocation Process Issue Date: Revision Date: Sources: Key Words: Summary: March 3, 2009 December 16, 2009 Federal Programs, Grants Management Comprehensive Continuous

Comprehensive Continuous Improvement Plan Allocation Process Issue Date: Revision Date: Sources: Key Words: Summary: March 3, 2009 December 16, 2009 Federal Programs, Grants Management Comprehensive Continuous

2017 Guidelines Arts & Culture Grant Program. Grant applications are due Friday, October 14, 2016 by 4:30pm

2017 Guidelines Arts & Culture Grant Program Grant applications are due Friday, October 14, 2016 by 4:30pm Due Date: Friday, October 14, 2016 by 4:30pm Table of Contents Program Purpose.... 4 Qualifying

2017 Guidelines Arts & Culture Grant Program Grant applications are due Friday, October 14, 2016 by 4:30pm Due Date: Friday, October 14, 2016 by 4:30pm Table of Contents Program Purpose.... 4 Qualifying

Contract & Users Group

Contract & Users Group September 12, 2016 10:00 a.m.- 11:30 a.m. CHASS INT North 1020. Business & Financial Services A Division of Business & Administration Services (BAS) BAS Agenda Payroll Certification

Contract & Users Group September 12, 2016 10:00 a.m.- 11:30 a.m. CHASS INT North 1020. Business & Financial Services A Division of Business & Administration Services (BAS) BAS Agenda Payroll Certification

Match, Leveraged Resources and Program Income

Match, Leveraged Resources and Program Income Speakers Deborah Galloway OGM, DPRR Supervisor Fiscal Policy Unit galloway.deborah@dol.gov Chanel Castaneda OGM, DPRR Grants Management Specialist castaneda.chanel@dol.gov

Match, Leveraged Resources and Program Income Speakers Deborah Galloway OGM, DPRR Supervisor Fiscal Policy Unit galloway.deborah@dol.gov Chanel Castaneda OGM, DPRR Grants Management Specialist castaneda.chanel@dol.gov

OUTDOOR RECREATION ACQUISITION, DEVELOPMENT AND PLANNING U.S. DEPARTMENT OF INTERIOR

APRIL 2009 15.916 OUTDOOR RECREATION ACQUISITION, DEVELOPMENT AND PLANNING State Project/Program: LAND AND WATER CONSERVATION FUND U.S. DEPARTMENT OF INTERIOR Federal Authorization: Land and Water Conservation

APRIL 2009 15.916 OUTDOOR RECREATION ACQUISITION, DEVELOPMENT AND PLANNING State Project/Program: LAND AND WATER CONSERVATION FUND U.S. DEPARTMENT OF INTERIOR Federal Authorization: Land and Water Conservation

A-133 Single Audits: Common Audit Findings & Ways to Mitigate and Prevent Them

A-133 Single Audits: Common Audit Findings & Ways to Mitigate and Prevent Them Wayne Finley, MBA, CGMS Mayor s Office Education & Government Services City of St. Petersburg, Florida Session Objectives

A-133 Single Audits: Common Audit Findings & Ways to Mitigate and Prevent Them Wayne Finley, MBA, CGMS Mayor s Office Education & Government Services City of St. Petersburg, Florida Session Objectives

30. GRANTS AND FUNDING ASSISTANCE POLICY

30. GRANTS AND FUNDING ASSISTANCE POLICY POLICY It is the policy of Scott County to account for, and file all appropriate documentation in relation to, any grants or other funding that the county applies

30. GRANTS AND FUNDING ASSISTANCE POLICY POLICY It is the policy of Scott County to account for, and file all appropriate documentation in relation to, any grants or other funding that the county applies

Discretionary Grants Overview. Why This Session Is Needed. Lesson Overview & Module Objectives. Modifications: when, why, and how

Oversight and Monitoring 1 Why This Session Is Needed Prior approval requirements Ability to incur costs Modifications: when, why, and how Application to subrecipients Formula authority 2 Lesson Overview

Oversight and Monitoring 1 Why This Session Is Needed Prior approval requirements Ability to incur costs Modifications: when, why, and how Application to subrecipients Formula authority 2 Lesson Overview

Carryover Process Diabetes in Indian Country Conference

2017 Diabetes in Indian Country Conference Carryover Process John Hoffman, Senior Grants Management Specialist IHS Division of Grant Management September 19, 2017 Objectives 1. Carryover Policy and Procedure

2017 Diabetes in Indian Country Conference Carryover Process John Hoffman, Senior Grants Management Specialist IHS Division of Grant Management September 19, 2017 Objectives 1. Carryover Policy and Procedure

U.S. Department of Justice 42 U.S.C (a) N.C. Department of Public Safety

N.C. Department of Public Safety") APRIL 2016 16.575 CRIME VICTIM ASSISTANCE State Project/Program: VICTIMS OF CRIME ACT (VOCA) Federal Authorization: U.S. Department of Justice 42 U.S.C. 10603(a) Governor s Crime Commission Agency Contact

APRIL 2016 16.575 CRIME VICTIM ASSISTANCE State Project/Program: VICTIMS OF CRIME ACT (VOCA) Federal Authorization: U.S. Department of Justice 42 U.S.C. 10603(a) Governor s Crime Commission Agency Contact

Program Management Plan

Program Management Plan Section 5310 ENHANCED MOBILITY OF SENIORS AND INDIVIDUALS WITH DISABILITIES PROGRAM Table of Contents GOALS AND OBJECTIVES... 3 ROLES AND RESPONSIBILITIES OF VIA... 3 ALAMO AREA

Program Management Plan Section 5310 ENHANCED MOBILITY OF SENIORS AND INDIVIDUALS WITH DISABILITIES PROGRAM Table of Contents GOALS AND OBJECTIVES... 3 ROLES AND RESPONSIBILITIES OF VIA... 3 ALAMO AREA

Table 1. Cost Share Criteria

Under U.S. Government (USG) funding, cost share refers to the resources an organization contributes to the total cost of a USG grant that is not included as part of the grant. Cost share becomes a condition

Under U.S. Government (USG) funding, cost share refers to the resources an organization contributes to the total cost of a USG grant that is not included as part of the grant. Cost share becomes a condition

Noxious Weed And Invasive Plant Grant Program

Plant Protection Division Phone: 651-201-6020 625 Robert Street North, Saint Paul, MN 55155-2538 WWW.MDA.STATE.MN.US Noxious Weed And Invasive Plant Grant Program Request for Proposal Grant Overview The

Plant Protection Division Phone: 651-201-6020 625 Robert Street North, Saint Paul, MN 55155-2538 WWW.MDA.STATE.MN.US Noxious Weed And Invasive Plant Grant Program Request for Proposal Grant Overview The

Rural and Community Art Grants

Rural and Community Art Grants Guidelines and Application Forms for July 1, 2015 through June 30, 2017 Grant Deadlines: FY2016: October 30, 2015 and April 29, 2016 FY2017: October 28, 2016 and April 28,

Rural and Community Art Grants Guidelines and Application Forms for July 1, 2015 through June 30, 2017 Grant Deadlines: FY2016: October 30, 2015 and April 29, 2016 FY2017: October 28, 2016 and April 28,

Art Project Grants. Guidelines and Application Forms for July 1, 2014 through June 30, 2015

Art Project Grants Guidelines and Application Forms for July 1, 2014 through June 30, 2015 Grant Deadlines: FY2015: July 31, 2014 and January 30, 2015 Arrowhead Regional Arts Council Marshall Professional

Art Project Grants Guidelines and Application Forms for July 1, 2014 through June 30, 2015 Grant Deadlines: FY2015: July 31, 2014 and January 30, 2015 Arrowhead Regional Arts Council Marshall Professional

FUNDRAISING EVENT ADMINISTRATION

PURPOSE/POLICY To provide procedures and guidance for conducting fundraising events in accordance with ICSUAM Policy 15701.00. The University shall accept fundraising proceeds for support of accepted programs

PURPOSE/POLICY To provide procedures and guidance for conducting fundraising events in accordance with ICSUAM Policy 15701.00. The University shall accept fundraising proceeds for support of accepted programs

Finance for non-degree granting private, not-for-profit institutions and public institutions using FASB Reporting Standards

2013-14 Survey Materials > Form date: 10/9/2013 Finance for non-degree granting private, not-for-profit institutions and public institutions using FASB Reporting Standards Overview Finance Overview Purpose

2013-14 Survey Materials > Form date: 10/9/2013 Finance for non-degree granting private, not-for-profit institutions and public institutions using FASB Reporting Standards Overview Finance Overview Purpose

MUNICIPALITY OF ANCHORAGE ARTS ADVISORY COMMISSION ART GRANT FUNDING APPLICATION GUIDELINES

MUNICIPALITY OF ANCHORAGE ARTS ADVISORY COMMISSION ART GRANT FUNDING APPLICATION GUIDELINES GENERAL INFORMATION 1. The Anchorage Arts Advisory Commission is established by the Municipal Code, Chapter 4.60.150

MUNICIPALITY OF ANCHORAGE ARTS ADVISORY COMMISSION ART GRANT FUNDING APPLICATION GUIDELINES GENERAL INFORMATION 1. The Anchorage Arts Advisory Commission is established by the Municipal Code, Chapter 4.60.150

Art Project Grants. Guidelines and Application Forms for July 1, 2015 through June 30, 2017

Art Project Grants Guidelines and Application Forms for July 1, 2015 through June 30, 2017 Grant Deadlines: FY2016: July 31, 2015 and January 29, 2016 FY2017: July 29, 2016 and January 27, 2017 Arrowhead

Art Project Grants Guidelines and Application Forms for July 1, 2015 through June 30, 2017 Grant Deadlines: FY2016: July 31, 2015 and January 29, 2016 FY2017: July 29, 2016 and January 27, 2017 Arrowhead

GEORGIA STATE UNIVERSITY RESEARCH FOUNDATION, INC. AND AFFILIATE (A COMPONENT UNIT OF THE STATE OF GEORGIA)

") GEORGIA STATE UNIVERSITY RESEARCH FOUNDATION, INC. AND AFFILIATE (A COMPONENT UNIT OF THE STATE OF GEORGIA) FINANCIAL STATEMENTS AND COMPLIANCE REPORTS For the Year Ended June 30, 2013 GEORGIA STATE UNIVERSITY

GEORGIA STATE UNIVERSITY RESEARCH FOUNDATION, INC. AND AFFILIATE (A COMPONENT UNIT OF THE STATE OF GEORGIA) FINANCIAL STATEMENTS AND COMPLIANCE REPORTS For the Year Ended June 30, 2013 GEORGIA STATE UNIVERSITY

TOWN AUDITING SERVICES

REQUEST FOR PROPOSAL TOWN AUDITING SERVICES TOWN OF LONGMEADOW MASSACHUSETTS Saved as: RPF Acct Auditing Services FY 12-14 03/1/11 TOWN OF LONGMEADOW REQUEST FOR PROPOSALS FOR AUDITING SERVICES The Town

REQUEST FOR PROPOSAL TOWN AUDITING SERVICES TOWN OF LONGMEADOW MASSACHUSETTS Saved as: RPF Acct Auditing Services FY 12-14 03/1/11 TOWN OF LONGMEADOW REQUEST FOR PROPOSALS FOR AUDITING SERVICES The Town

COST SHARING POLICY COST SHARING POLICY PAGE 1 OF 8

COST SHARING POLICY Effective Date: December 4, 2013 Replaces: Cost Sharing dated January 1, 2010 Approved by: Steve McNally, Senior Associate Vice Chancellor for Budget, Finance and Enrollment Services

COST SHARING POLICY Effective Date: December 4, 2013 Replaces: Cost Sharing dated January 1, 2010 Approved by: Steve McNally, Senior Associate Vice Chancellor for Budget, Finance and Enrollment Services

FY19 MDA Visit Mississippi TOURISM DEVELOPMENT GRANT GUIDELINES FESTIVALS and EVENTS

FY19 MDA Visit Mississippi TOURISM DEVELOPMENT GRANT GUIDELINES FESTIVALS and EVENTS SCOPE AND PURPOSE: The goal of the Tourism Development Grant would be to assist in festivals and events that Visit Mississippi

FY19 MDA Visit Mississippi TOURISM DEVELOPMENT GRANT GUIDELINES FESTIVALS and EVENTS SCOPE AND PURPOSE: The goal of the Tourism Development Grant would be to assist in festivals and events that Visit Mississippi

A Handbook for Local Leagues Including Procedures and Forms. THE LEAGUE OF WOMEN VOTERS of Washington Education Fund. Revised January 2015

YOUR EDUCATION FUND A Handbook for Local Leagues Including Procedures and Forms THE LEAGUE OF WOMEN VOTERS of Washington Education Fund Revised January 2015 (approved 1/21/2015-C3 Board) THE LEAGUE OF

YOUR EDUCATION FUND A Handbook for Local Leagues Including Procedures and Forms THE LEAGUE OF WOMEN VOTERS of Washington Education Fund Revised January 2015 (approved 1/21/2015-C3 Board) THE LEAGUE OF

JUVENILE JUSTICE AND DELINQUENCY PREVENTION ALLOCATION TO STATES. U.S. Department of Justice

APRIL 2013 16.540 JUVENILE JUSTICE AND DELINQUENCY PREVENTION- ALLOCATION TO STATES State Project/Program: JUVENILE JUSTICE AND DELINQUENCY PREVENTION (JJDP) U.S. Department of Justice Federal Authorization:

APRIL 2013 16.540 JUVENILE JUSTICE AND DELINQUENCY PREVENTION- ALLOCATION TO STATES State Project/Program: JUVENILE JUSTICE AND DELINQUENCY PREVENTION (JJDP) U.S. Department of Justice Federal Authorization:

SINGLE AUDIT REPORTS

S A F E T Y, S E R V I C E A N D F I N A N C I A L R E SPO N S I B I LIT Y SINGLE AUDIT REPORTS FOR THE FISCAL YEAR ENDED JUNE 30, 2017 Single Audit Reports issued in Accordance with Title 2 U.S. Code

S A F E T Y, S E R V I C E A N D F I N A N C I A L R E SPO N S I B I LIT Y SINGLE AUDIT REPORTS FOR THE FISCAL YEAR ENDED JUNE 30, 2017 Single Audit Reports issued in Accordance with Title 2 U.S. Code

Department of Human Services Division of Medical Assistance and Health Services Transportation Broker Services Contract Capitation Rates

New Jersey State Legislature Office of Legislative Services Office of the State Auditor Department of Human Services Division of Medical Assistance and Health Services Transportation Broker Services Contract

New Jersey State Legislature Office of Legislative Services Office of the State Auditor Department of Human Services Division of Medical Assistance and Health Services Transportation Broker Services Contract

The Office of Innovation and Improvement s Oversight and Monitoring of the Charter Schools Program s Planning and Implementation Grants

The Office of Innovation and Improvement s Oversight and Monitoring of the Charter Schools Program s Planning and Implementation Grants FINAL AUDIT REPORT ED-OIG/A02L0002 September 2012 Our mission is

The Office of Innovation and Improvement s Oversight and Monitoring of the Charter Schools Program s Planning and Implementation Grants FINAL AUDIT REPORT ED-OIG/A02L0002 September 2012 Our mission is

Creative Investment Program

Creative Investment Program for Not-for-Profit Organizations Fiscal Year 2016 October 1, 2015 - September 30, 2016 Purpose: To fund small but complete cultural projects taking place in Broward County for

Creative Investment Program for Not-for-Profit Organizations Fiscal Year 2016 October 1, 2015 - September 30, 2016 Purpose: To fund small but complete cultural projects taking place in Broward County for

Aboriginal Community Capital Grants Program Guide

APPLICATION GUIDE FOR THE ABORIGINAL COMMUNITY CAPITAL GRANTS PROGRAM WHAT YOU NEED TO KNOW BEFORE YOU APPLY Before completing your Aboriginal Community Capital Grants Program application, please read

APPLICATION GUIDE FOR THE ABORIGINAL COMMUNITY CAPITAL GRANTS PROGRAM WHAT YOU NEED TO KNOW BEFORE YOU APPLY Before completing your Aboriginal Community Capital Grants Program application, please read

North Carolina GlaxoSmithKline Foundation The Ribbon of Hope

North Carolina GlaxoSmithKline Foundation The Ribbon of Hope Emphasizing the Importance of Science, Health, and Education to North Carolina Request for Proposals The North Carolina GlaxoSmithKline Foundation

North Carolina GlaxoSmithKline Foundation The Ribbon of Hope Emphasizing the Importance of Science, Health, and Education to North Carolina Request for Proposals The North Carolina GlaxoSmithKline Foundation

RDA Community Grant Fall 2018

RDA Community Grant Fall 2018 Introduction Thank you for the great work you do for our community! The scoring guideline chart used by RDA Board members to rate proposals is available to you with the above

RDA Community Grant Fall 2018 Introduction Thank you for the great work you do for our community! The scoring guideline chart used by RDA Board members to rate proposals is available to you with the above

The Ford Foundation EQUIVALENCY AFFIDAVIT PACKET FOR NON-U.S. GRANT APPLICANTS

The Ford Foundation EQUIVALENCY AFFIDAVIT PACKET FOR NON-U.S. GRANT APPLICANTS This packet includes: INTRODUCTION "EQUIVALENCY AFFIDAVIT FOR NON-U.S. ORGANIZATIONS" AND INSTRUCTIONS "PUBLIC SUPPORT SCHEDULE"

The Ford Foundation EQUIVALENCY AFFIDAVIT PACKET FOR NON-U.S. GRANT APPLICANTS This packet includes: INTRODUCTION "EQUIVALENCY AFFIDAVIT FOR NON-U.S. ORGANIZATIONS" AND INSTRUCTIONS "PUBLIC SUPPORT SCHEDULE"

SECTION 5310 APPLICATION GUIDELINES FOR 2018 PROJECTS:

#237894-2 KJM/CTH/JBS/JMD 6-26-17 SECTION 5310 APPLICATION GUIDELINES FOR 2018 PROJECTS: VEHICLE CAPITAL PURCHASES MOBILITY MANAGEMENT OPERATING NON-VEHICLE CAPITAL Administered by the Southeastern Wisconsin

#237894-2 KJM/CTH/JBS/JMD 6-26-17 SECTION 5310 APPLICATION GUIDELINES FOR 2018 PROJECTS: VEHICLE CAPITAL PURCHASES MOBILITY MANAGEMENT OPERATING NON-VEHICLE CAPITAL Administered by the Southeastern Wisconsin

Habitat Restoration Grants

Habitat Restoration Grants Great Outdoors Colorado (GOCO) is pleased to announce the 2017 habitat restoration grant cycle for proposals that seek to improve and restore Colorado's rivers, streams, wetlands,

Habitat Restoration Grants Great Outdoors Colorado (GOCO) is pleased to announce the 2017 habitat restoration grant cycle for proposals that seek to improve and restore Colorado's rivers, streams, wetlands,

2018 GUIDELINES COMPETITIVE GRANTS REQUIRING THE LONG FORM APPLICATION

2018 GUIDELINES COMPETITIVE GRANTS REQUIRING THE LONG FORM APPLICATION Guidelines for: UNRESTRICTED ~ KESSLER ~ ORGANIZATIONAL STRENGTHENING ~ ~ PUBLIC SAFETY ~ BRADLEY BREAKTHROUGH COMMUNITY BENEFITS

2018 GUIDELINES COMPETITIVE GRANTS REQUIRING THE LONG FORM APPLICATION Guidelines for: UNRESTRICTED ~ KESSLER ~ ORGANIZATIONAL STRENGTHENING ~ ~ PUBLIC SAFETY ~ BRADLEY BREAKTHROUGH COMMUNITY BENEFITS

SCHOOL TECHNOLOGY FUND STATE PUBLIC SCHOOL FUND (SPSF) PRC 015 (LOCAL EDUCATION AGENCIES - LEAS)

PRC 015 (LOCAL EDUCATION AGENCIES - LEAS)") APRIL 2016 SCHOOL TECHNOLOGY FUND STATE PUBLIC SCHOOL FUND (SPSF) PRC 015 (LOCAL EDUCATION AGENCIES - LEAS) State Authorization: North Carolina General Statutes 115C-102.6A to 115C-102.6D N. C. Department

APRIL 2016 SCHOOL TECHNOLOGY FUND STATE PUBLIC SCHOOL FUND (SPSF) PRC 015 (LOCAL EDUCATION AGENCIES - LEAS) State Authorization: North Carolina General Statutes 115C-102.6A to 115C-102.6D N. C. Department

Financial Management

August 17, 2005 Financial Management Defense Departmental Reporting System Audited Financial Statements Report Map (D-2005-102) Department of Defense Office of the Inspector General Constitution of the

August 17, 2005 Financial Management Defense Departmental Reporting System Audited Financial Statements Report Map (D-2005-102) Department of Defense Office of the Inspector General Constitution of the

Deloitte & Touche LLP 2200 Ross Ave. Suite 1600 Dallas, TX 75201 USA INDEPENDENT AUDITORS' REPORT Tel: +1 214 840 7000 Fax: +1 214 840 7050 www.deloitte.com Members of the Board of Trustees Dallas Independent

Deloitte & Touche LLP 2200 Ross Ave. Suite 1600 Dallas, TX 75201 USA INDEPENDENT AUDITORS' REPORT Tel: +1 214 840 7000 Fax: +1 214 840 7050 www.deloitte.com Members of the Board of Trustees Dallas Independent

REQUEST FOR PROPOSALS FOR FINANCIAL AND ACCOUNTING SERVICES

REQUEST FOR PROPOSALS FOR FINANCIAL AND ACCOUNTING SERVICES Issued: March 30, 2015 Proposals Due: April 24, 2015, 3:00 pm Marshall Moran RethinkWaste Finance Manager 610 Elm Street, Suite 202 San Carlos,

REQUEST FOR PROPOSALS FOR FINANCIAL AND ACCOUNTING SERVICES Issued: March 30, 2015 Proposals Due: April 24, 2015, 3:00 pm Marshall Moran RethinkWaste Finance Manager 610 Elm Street, Suite 202 San Carlos,

INVITATION FOR APPOINTMENT OF INTERNAL AUDITORS FOR THREE YEARS FROM FY Indian Council for Research on International Economic Relations

INVITATION FOR APPOINTMENT OF INTERNAL AUDITORS FOR THREE YEARS FROM FY 2016-17 Indian Council for Research on International Economic Relations Notice inviting offers for Professional Services in the field

INVITATION FOR APPOINTMENT OF INTERNAL AUDITORS FOR THREE YEARS FROM FY 2016-17 Indian Council for Research on International Economic Relations Notice inviting offers for Professional Services in the field

MSU s Financial Administrator Development Program Post-Award Contract and Grant Administration

MSU s Financial Administrator Development Program Post-Award Contract and Grant Administration Presenters: Dan Evon, Executive Director, Contract and Grant Administration Evonne Pedawi, Assistant Director,

MSU s Financial Administrator Development Program Post-Award Contract and Grant Administration Presenters: Dan Evon, Executive Director, Contract and Grant Administration Evonne Pedawi, Assistant Director,

2018 Guidelines Community Grant Program

2018 Guidelines Community Grant Program Grant applications are due Friday, October 13, 2017 by 4:30 PM 2 P a g e TABLE OF CONTENTS PURPOSE...... 4 FUNDING CATEGORIES...... 5 ELIGIBILITY...... 6 INELIGIBILITY......

2018 Guidelines Community Grant Program Grant applications are due Friday, October 13, 2017 by 4:30 PM 2 P a g e TABLE OF CONTENTS PURPOSE...... 4 FUNDING CATEGORIES...... 5 ELIGIBILITY...... 6 INELIGIBILITY......

Arts and Cultural Heritage Community Arts Learning Grants (for Organizations)

") Arts and Cultural Heritage Community Arts Learning Grants (for Organizations) Guidelines and Application Forms July 1, 2015 through June 30, 2017 Grant Deadlines: FY2016: July 31, 2015 and January 29,

Arts and Cultural Heritage Community Arts Learning Grants (for Organizations) Guidelines and Application Forms July 1, 2015 through June 30, 2017 Grant Deadlines: FY2016: July 31, 2015 and January 29,